Q3 FY26 Financial Performance Overview

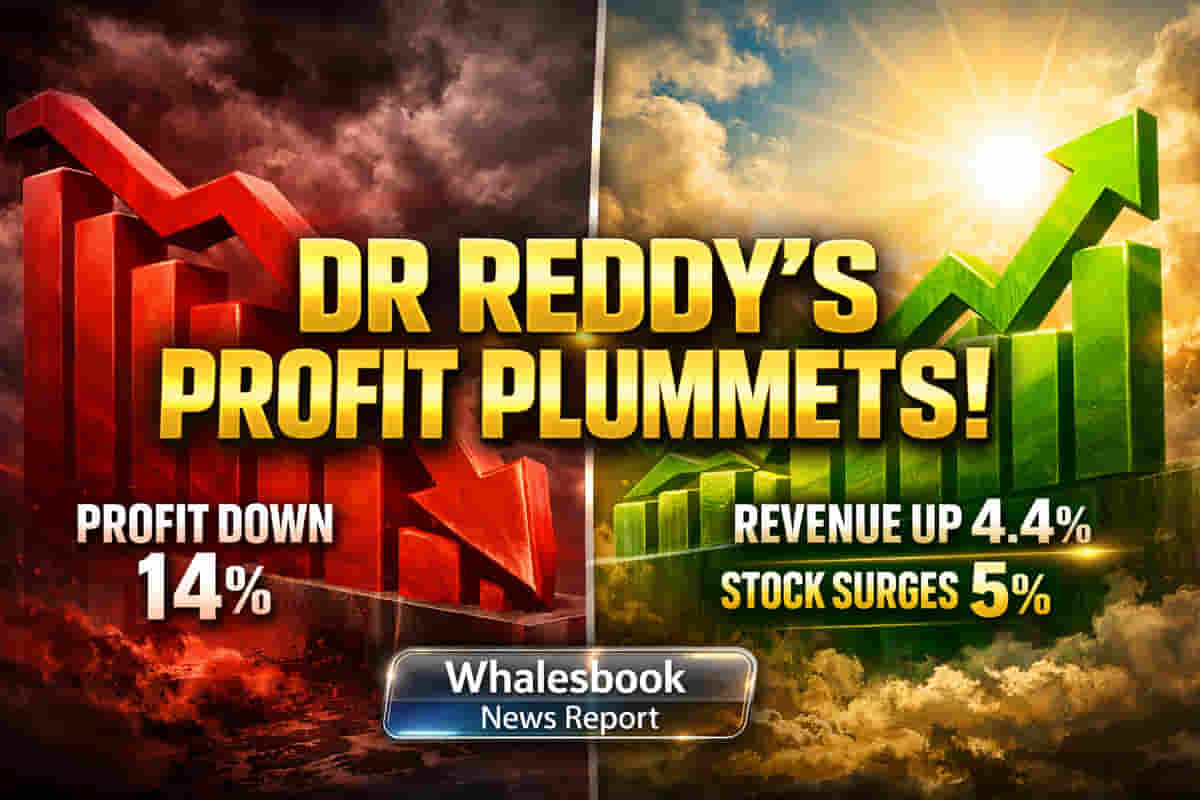

Dr Reddy's Laboratories has reported its financial outcomes for the third quarter of fiscal year 2026. The company achieved revenue from operations of ₹8,727 crore, reflecting a 4.4% year-on-year expansion from the ₹8,357 crore recorded in the corresponding period of FY25. Despite this revenue growth, consolidated net profit for the quarter saw a 14% year-on-year decrease, falling to ₹1,210 crore from ₹1,413 crore in Q3 FY25. Earnings before interest, tax, depreciation, and amortisation (EBITDA) for the period amounted to ₹2,049 crore, a reduction from ₹2,298 crore reported in the prior year's quarter.

Influencing Factors and Sector Dynamics

The decrease in net profit was attributed to several operational factors, including a decline in contributions from key products such as gRevlimid and persistent pricing pressures within the United States market. Elevated selling, general, and administrative expenses also exerted pressure on the company's profitability. On a positive note, Dr Reddy's revenue growth was significantly bolstered by robust performance in its domestic business, which registered a 19% year-on-year increase, with expectations for sustained growth exceeding 15%. Favourable currency exchange rates also provided a tailwind to the company's top line. The broader Indian pharmaceutical industry is navigating a complex environment, characterized by pricing challenges in developed markets and opportunities stemming from strong domestic demand and emerging markets. Key sector themes include managing competition for established generics and investing in the development and commercialization of specialty products.

Market Activity and Analyst Views

Following the release of its Q3 FY26 results on Tuesday, January 20, 2026, after market close, Dr Reddy's Laboratories' stock experienced an upward trend on Wednesday, January 21, 2026, reaching an intra-day level of ₹1,211.50. As of Thursday, January 22, 2026, the stock is trading at ₹1,205.00 on moderate volume. Analyst perspectives on Dr Reddy's medium-term outlook present a divided landscape. Emkay Global Financial Services has maintained a 'Reduce' rating, adjusting its target price to ₹1,200. They noted that while Q3 margin performance aligned with expectations, increased administrative spending offset gross margin improvements, and forecast FY28 earnings per share to potentially trail FY25 levels. Motilal Oswal Financial Services assigned a 'Neutral' rating and revised their target price to ₹1,220, acknowledging strong execution across India, Europe, and Russia that compensated for reduced gRevlimid sales, resulting in an earnings beat. Although FY26 estimates were reduced, FY27 estimates were raised due to improved growth prospects in key regions. Conversely, Elara Capital reiterated a 'Buy' recommendation with a target price of ₹1,588, attributing the profit dip partially to one-off Revlimid sales and highlighting the continued strength of the Indian market. JM Financial Institutional Securities also upheld a 'Buy' rating and raised its target to ₹1,545, suggesting that current valuations may incorporate US market challenges, with significant ex-US growth and upcoming product launches poised to offer medium-term earnings visibility.