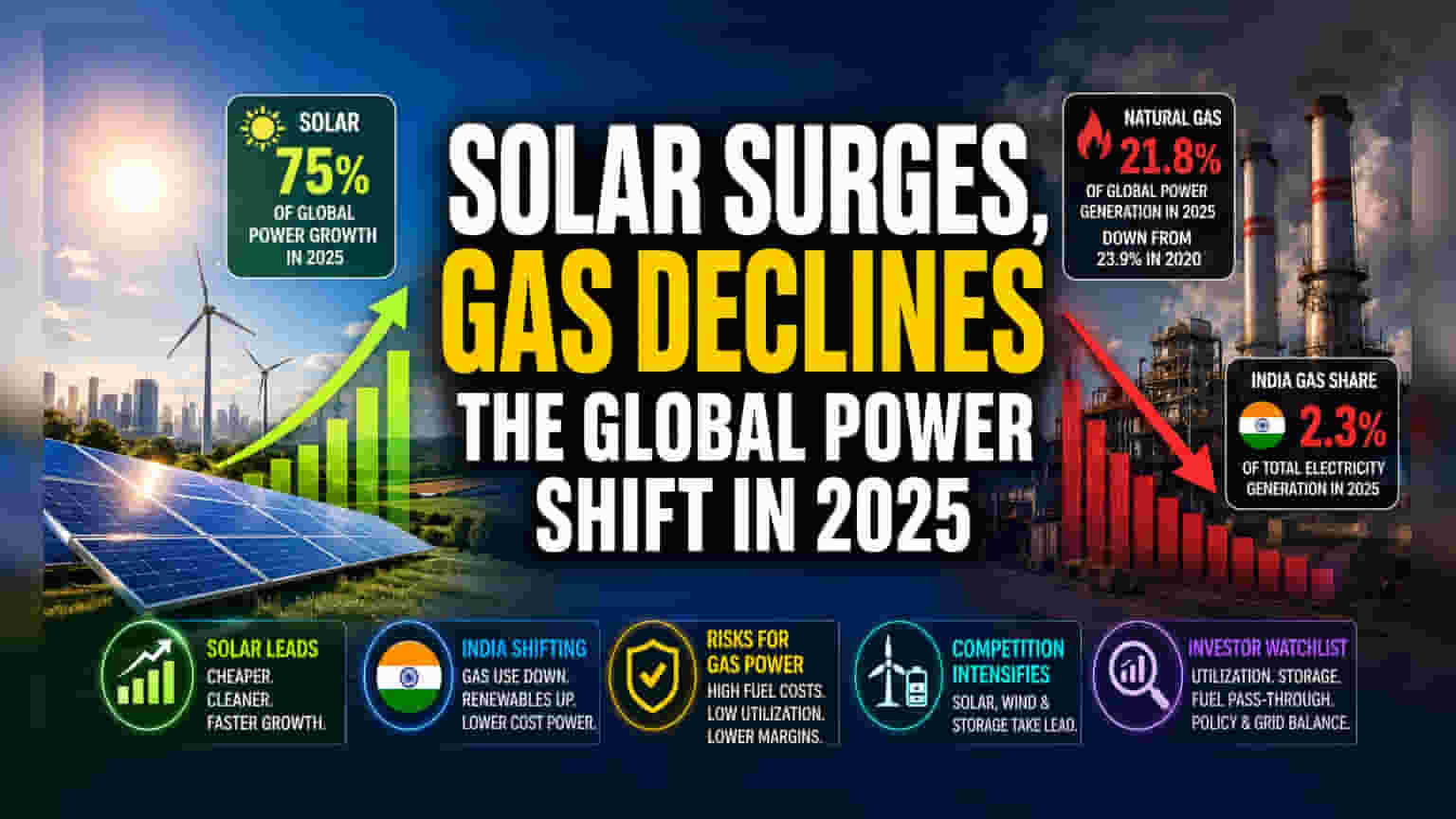

What Happened

Solar power has become the leading driver of the global electricity market, accounting for approximately 75% of the growth in new power demand in 2025. While natural gas-fired generation has continued to grow in total volume, its overall share of the power mix has declined for five years in a row. Globally, gas accounted for 21.8% of power generation in 2025, down from 23.9% in 2020. This shift is also visible in India, where gas-based power generation has fallen significantly, contributing only about 2.3% of the country’s total electricity generation in 2025, compared to much higher levels in the past.

Why This Matters For Investors

The rapid rise of solar energy is fundamentally changing how electricity is generated and managed. For investors in the power sector, this transition highlights a move away from fossil fuel-heavy generation toward renewable sources that are becoming cheaper and easier to deploy. The reliance on natural gas is decreasing not just because of environmental policy, but because of economic factors. Imported natural gas is often expensive and subject to price volatility, making it a less attractive option for base-load power generation compared to solar and wind energy.

The India Power Mix Shift

India has seen a notable decline in its dependence on gas for electricity. In previous years, gas-fired power was a more significant part of the energy basket. However, due to the high cost of imported Liquefied Natural Gas (LNG) and the competitive pricing of renewable energy, many gas-based plants in India have seen their operations reduced. These plants are often used only during peak demand hours or when renewable output is low. The shift toward solar indicates that the market is favoring the lowest-cost generation, which directly impacts the profitability and asset utilization of older, gas-reliant power companies.

Business And Operational Risks

While solar is growing, gas-based power assets still serve a specific function in the grid as a source of peaking power. However, companies operating these plants face significant operational risks. Profit margins for gas-based power producers are highly sensitive to global gas prices. If the cost of imported fuel remains high, these plants may continue to struggle with low capacity utilization. Furthermore, the push for energy security is encouraging nations to prioritize domestically produced renewable energy over imported fuels, which puts additional pressure on the gas-power business model.

Sector Pressure And Competition

Power companies that rely heavily on gas are facing competition from solar and wind farms, which benefit from government incentives and declining capital costs. This sector pressure is not limited to India; major economies like Japan and the United Kingdom have also reported sharp declines in gas-fired power generation. For investors, this creates a clear divide in the power sector. Companies that are successfully transitioning their portfolios toward renewable energy, such as solar, wind, and storage, may see different long-term growth trajectories compared to those heavily dependent on traditional, high-cost fossil fuel generation.

What Investors Should Track

The key monitorable for investors is how power companies manage their asset portfolios amidst this energy transition. It is important to watch for changes in capacity utilization levels for gas-based power plants, especially during periods of high gas prices. Additionally, investors may monitor the adoption of battery storage technologies, which can make solar and wind more reliable, potentially reducing the future need for gas-based peaking power. Future updates on fuel cost pass-through mechanisms and government policy regarding grid balancing will also be important for assessing the long-term outlook for power producers.