The Economic Feedback Loop of Grid Defection

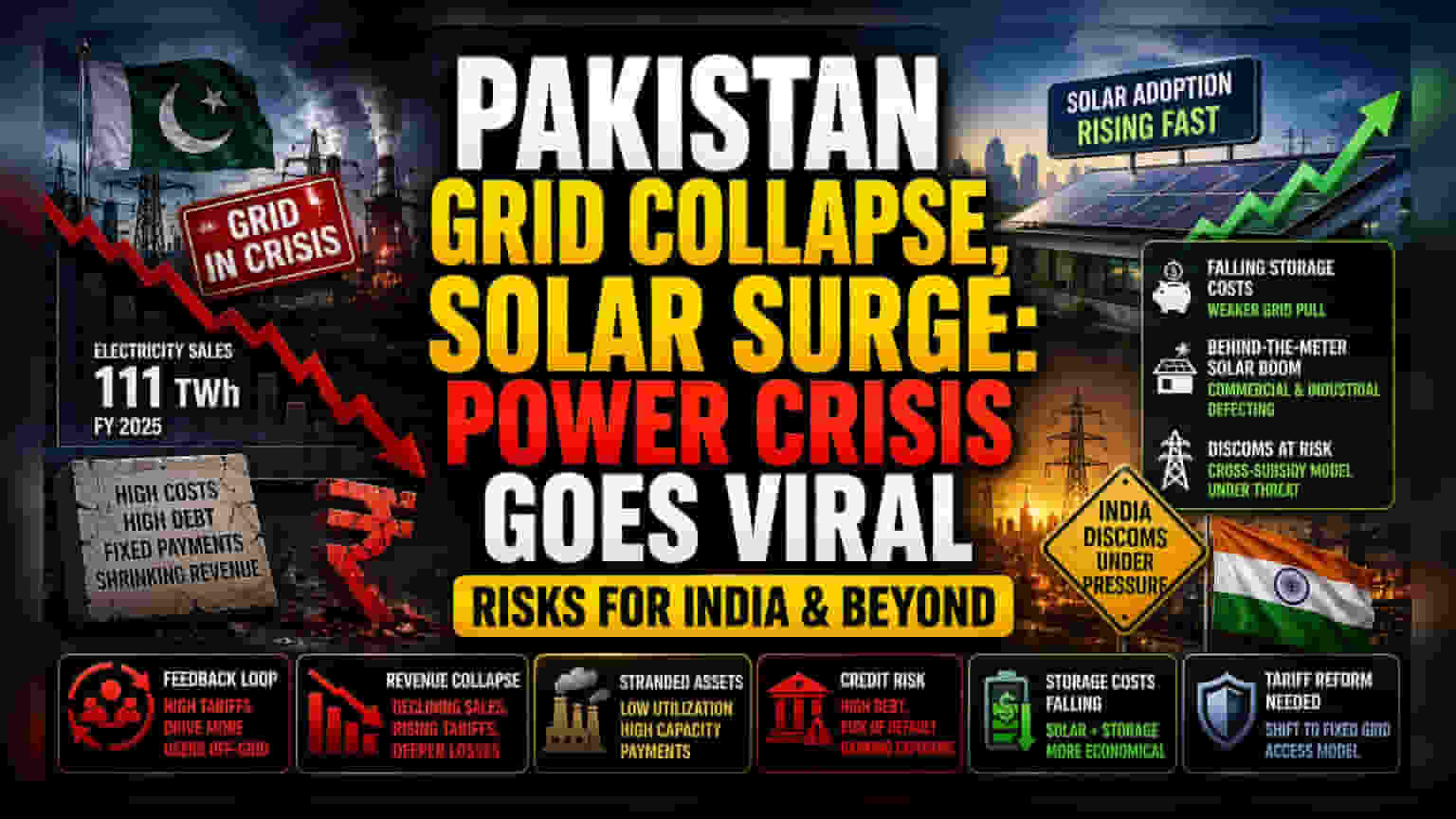

The exodus from Pakistan’s national grid is not merely an environmental success story but an unfolding financial catastrophe for state-backed utilities. As electricity sales plummeted to 111 terawatt-hours in fiscal 2025, the underlying cost structure of the power sector remained rigid. Utilities are now burdened with high-interest debt servicing and inflexible long-term capacity payments to thermal power producers. Because these fixed costs are socialized across a shrinking pool of remaining grid-dependent users, electricity tariffs have surged to compensate for the lost revenue. This creates a reflexive feedback loop: higher prices drive more consumers toward off-grid solar, further eroding the utility's base and accelerating its trajectory toward insolvency.

Cross-Border Implications and Market Risks

Regional power distributors, particularly those in India, are monitoring this transition with increasing apprehension. Unlike Pakistan’s acute grid instability, Indian distribution companies—or DISCOMs—maintain a different risk profile defined by cross-subsidization, where industrial and commercial tariffs are artificially inflated to subsidize agricultural and residential use. This pricing model leaves the most profitable tier of customers vulnerable to capture by the private solar sector. If commercial users continue to adopt behind-the-meter solar systems to bypass high grid tariffs, the financial viability of Indian state utilities could face similar, albeit slower, deterioration. The critical variable is the cost of storage; as lithium-iron-phosphate battery prices continue to decline, the economic rationale for remaining on the grid weakens for a broader range of commercial enterprises.

The Structural Weakness of Legacy Infrastructure

The fundamental issue is that current utility regulatory frameworks were built for a centralized, top-down distribution model. They lack the flexibility to manage bidirectional energy flows or the loss of large-scale baseload demand. Power producers tied to long-term purchase agreements are now sitting on assets that are rapidly becoming stranded. As utilization rates fall, the risk of technical defaults on power project debt increases, potentially triggering a broader credit crunch within the infrastructure banking sector. Institutional investors are beginning to discount utilities exposed to high-debt, high-capacity-payment models, signaling a shift in how the market values legacy energy providers in the age of decentralized generation. Without a radical restructuring of tariff models—moving from volume-based charges to fixed grid-access fees—the shift toward solar independence will continue to undermine the creditworthiness of traditional energy utilities.