### The Legacy Infrastructure Burden

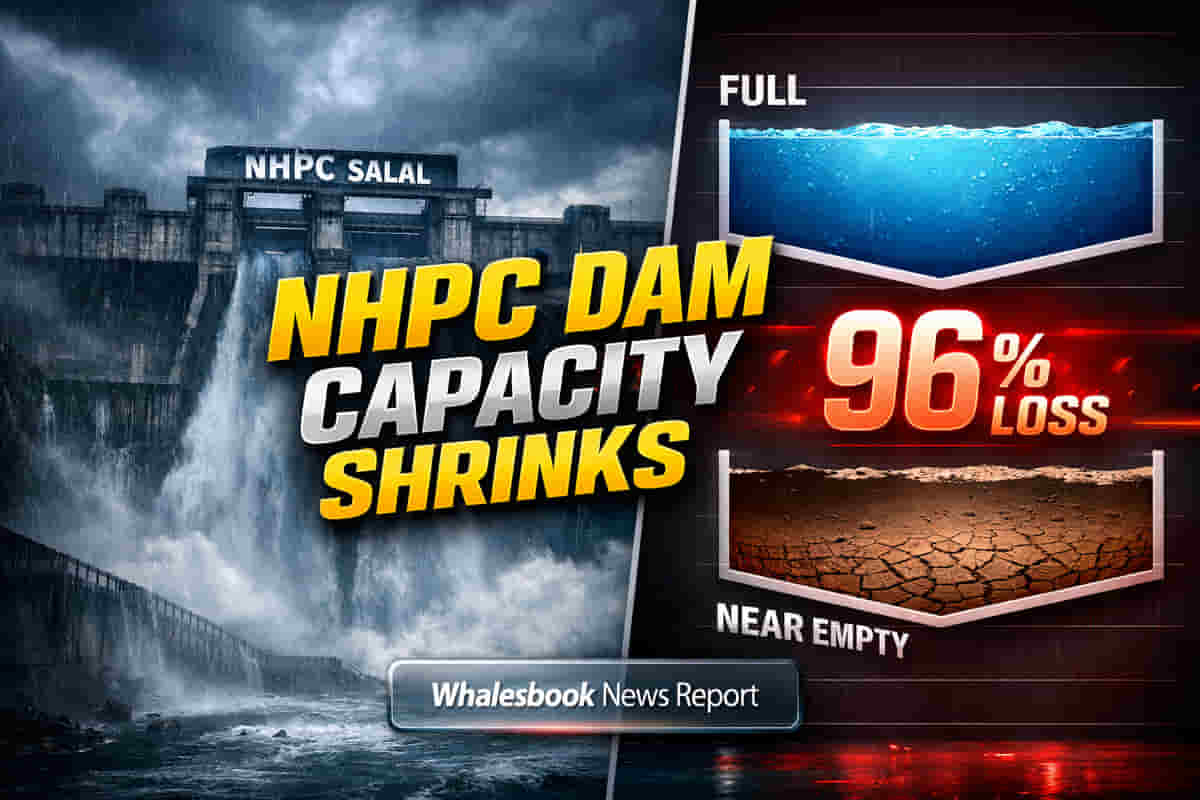

NHPC Ltd's Salal Hydroelectric Project faces a dire operational challenge, with its reservoir storage capacity plummeting by up to 96% from its original 284 million cubic metres (MCM) to a mere 9.91 MCM by May 2025. This dramatic reduction is a direct consequence of decades of sediment accumulation, stemming from the permanent plugging of six under-sluices and prohibition of silt-excluder gate operations, mandated by agreements tied to the 1960 Indus Waters Treaty and a subsequent 1978 accord [cite:news1]. The original dam design, featuring these crucial sediment-management facilities, was thus rendered inoperable, allowing silt to build unchecked over time [cite:news1].

### NHPC's Remediation Strategy & Costs

In response to this crisis, NHPC has initiated a comprehensive, three-pronged silt management plan, marking the first such effort since the treaty was put in abeyance. The strategy involves extensive dredging, periodic flushing operations, and reactivating the under-sluicing mechanisms. Reach Dredging Limited commenced desilting on November 25, 2025, having already dredged over 177,000 metric tonnes (MT) and disposed of substantial amounts. Dharti Dredging and Infrastructure Limited has also been engaged, with statutory clearances pending. Concurrently, a tender has been floated to functionalize the permanently plugged under-sluices, with bids due by March 23. These measures are critical for restoring at least partial storage capacity and ensuring the long-term operational viability of the 690 MW project [cite:news1]. However, recent financial performance indicates headwinds; the company reported a consolidated net profit decline of 2.89% to ₹320.60 crore and a 4.74% drop in total income to ₹2,492.83 crore in Q3 FY26 compared to the previous year.

### The Geopolitical Undertow

The operational constraints at Salal are amplified by broader geopolitical shifts. India placed the Indus Waters Treaty "in abeyance" on April 23, 2025, following the Pahalgam attack, citing national security and Pakistan's alleged support for terrorism. This suspension has effectively accelerated India's long-pending infrastructure projects, particularly those involving its allocated eastern rivers, as the nation asserts greater control over water resources. The imminent completion of the Shahpur Kandi dam by March 31, 2026, signifies India's intention to cease surplus Ravi river water flow into Pakistan, a move that will significantly impact downstream agricultural reliance in Pakistan. This strategic recalibration of water policy underscores the complex interplay between geopolitical tensions and vital national infrastructure like hydropower projects.

### The Analytical Deep Dive

NHPC, with a market capitalization hovering around ₹74.8 trillion and a TTM P/E ratio between 23-25, operates within a dynamic yet challenging Indian power sector. Compared to larger peers like NTPC (Market Cap ~₹352 trillion), NHPC shows slower annual revenue growth (2.12% over 5 years versus industry average of 14.85%) and a declining market share. JSW Energy, a comparable player, outperforms NHPC on key financial parameters, including sales, profit growth, ROE, and ROCE. The Indian hydropower sector itself faces significant hurdles, including high capital costs, environmental opposition, and regulatory delays. While NHPC's stock achieved multibagger status in prior years, reaching an all-time high in July 2024, recent technical indicators suggest a mildly bearish trend, with a 10.72% decline over the past month. Analyst sentiment varies, with some projecting significant upside, such as CLSA's target price of ₹117 and an average target of ₹128, while others have issued downgrades, and Q3 earnings missed expectations.

### THE FORENSIC BEAR CASE

The operational challenges at the Salal dam underscore the substantial financial and logistical burdens associated with retrofitting infrastructure constrained by historical geopolitical agreements. The cost of remediation, including extensive dredging and reactivating dormant facilities, is significant and may only offer partial restoration of capacity. NHPC's financial structure is also under scrutiny, with a rising debt-to-equity ratio reaching 1.09 times in the half-year and a P/E ratio of approximately 26.7, trading at a premium compared to its 5-year median of 9.3. This contrasts with its slower revenue and profit growth compared to industry averages. Furthermore, the company has experienced a decline in plant availability factor due to monsoon disruptions, and while its P/E ratio is competitive against some peers, its overall financial health metrics and operational efficiency (ROCE of 6.50%) lag behind some competitors. The ongoing geopolitical tensions surrounding water resources, particularly with the Indus Waters Treaty in abeyance, introduce an additional layer of operational and strategic risk, potentially impacting energy security and long-term project execution.

### Future Outlook

Despite current challenges, NHPC is pursuing strategic growth initiatives. The company's board recently approved investment proposals for two new hydropower projects in Jammu & Kashmir: Uri-I Stage-II (240 MW) and Dulhasti Stage-II (260 MW), with a combined outlay of ₹5,703 crore, slated to commence construction by March 1, 2026. NHPC also has a substantial project pipeline, including 2,744 MW in FY'27 and is diversifying into solar and wind energy. Analysts remain cautiously optimistic, with projections pointing towards significant capacity expansion and EPS growth in 2026, supporting target prices in the ₹117-₹128 range.