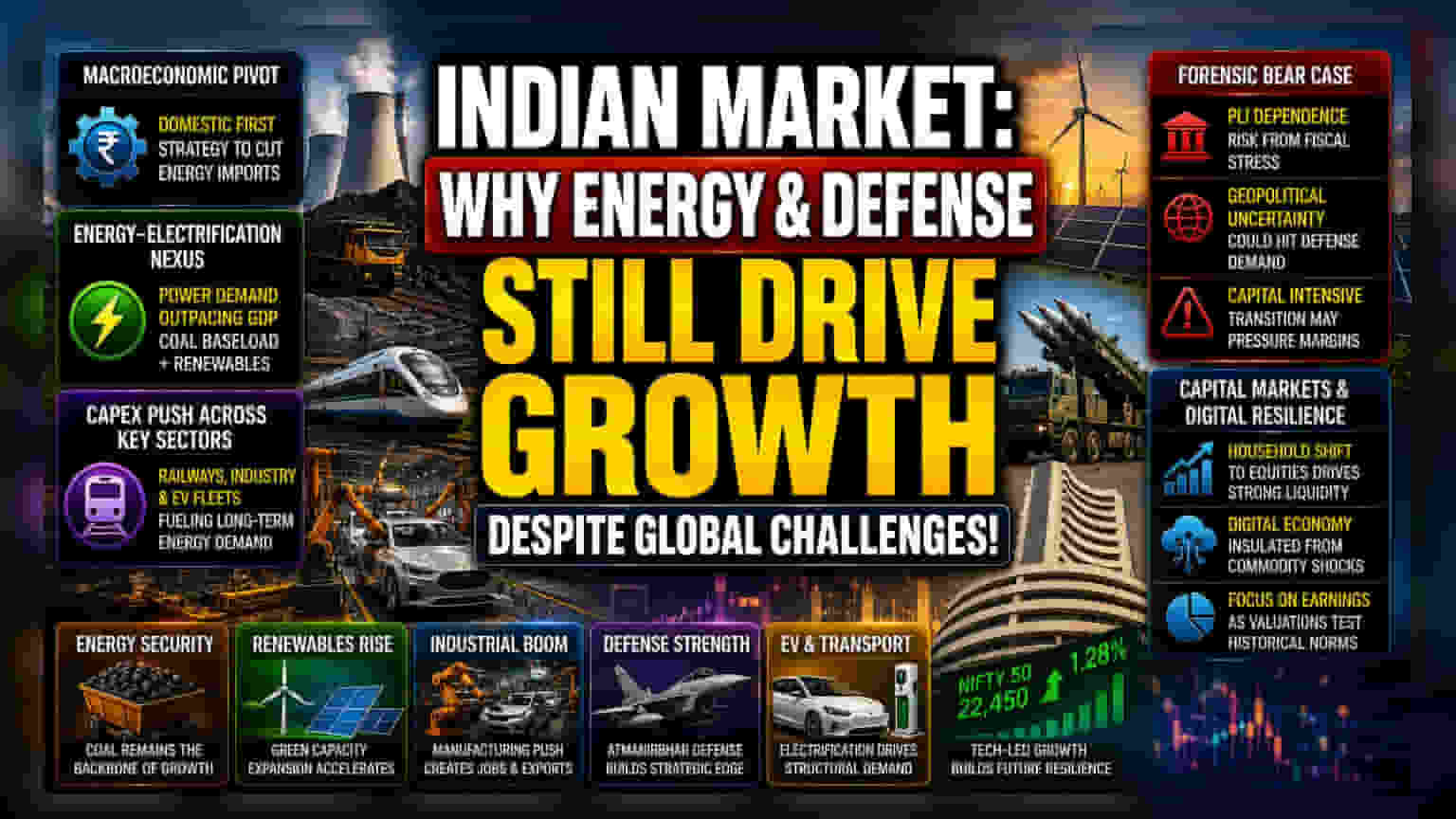

The Macroeconomic Pivot

The Indian market is undergoing a structural transition as institutional managers realign portfolios against a backdrop of persistent energy price volatility. While traditional energy imports typically drain fiscal resources, the current policy framework prioritizes domestic resource maximization. By pivoting toward coal and localized manufacturing, the economy aims to decouple domestic power demand from international crude benchmarks. This strategy is less about short-term cyclicality and more about securing a predictable supply chain for the country’s 1.45 billion consumers.

The Energy-Electrification Nexus

Electricity demand is currently outpacing general economic output, fueled by a multi-sector electrification push. Railway modernization serves as the operational blueprint for this trend, with aggressive capital expenditure now shifting toward industrial manufacturing and vehicle fleets. This creates a dual-benefit scenario for coal producers and renewable infrastructure providers. While renewables gain long-term utility, coal remains the economic bedrock required to support the baseload power necessary for the country’s burgeoning factory output. This ensures that even as the transition to electric vehicles gains traction, traditional energy extraction remains a high-growth, high-utility sector.

The Forensic Bear Case: Structural Risks

Despite the optimistic earnings projections, several structural hurdles remain. The reliance on Production Linked Incentive schemes creates a dependence on government fiscal health; should tax revenues falter, these subsidies may face delays. Furthermore, the defense sector’s long-term growth is heavily predicated on sustained geopolitical friction. If global tensions de-escalate, the urgency behind domestic military procurement could wane, leaving companies with bloated valuations and excessive order backlogs. Additionally, the shift toward coal gasification and non-fossil alternatives involves significant capital intensity, which risks margin compression if execution timelines for new infrastructure are missed.

Capital Markets and Digital Resilience

The migration of household savings into equity markets provides a liquidity buffer that distinguishes the current cycle from previous periods of macroeconomic tension. Digitalization remains a critical thematic insulator, as service-based growth is naturally less vulnerable to commodity price spikes than manufacturing. As capital continues to flow into these sectors, valuation premiums in defense and renewable energy may test historical norms, necessitating a disciplined focus on earnings delivery rather than mere thematic momentum.