A recent study by IEEFA identifies Andhra Pradesh, Uttar Pradesh, and Rajasthan as India’s top states for renewable energy investment, citing strong policy and infrastructure readiness. Investors should note that these rankings reflect where renewable energy projects face fewer execution hurdles.

What Happened

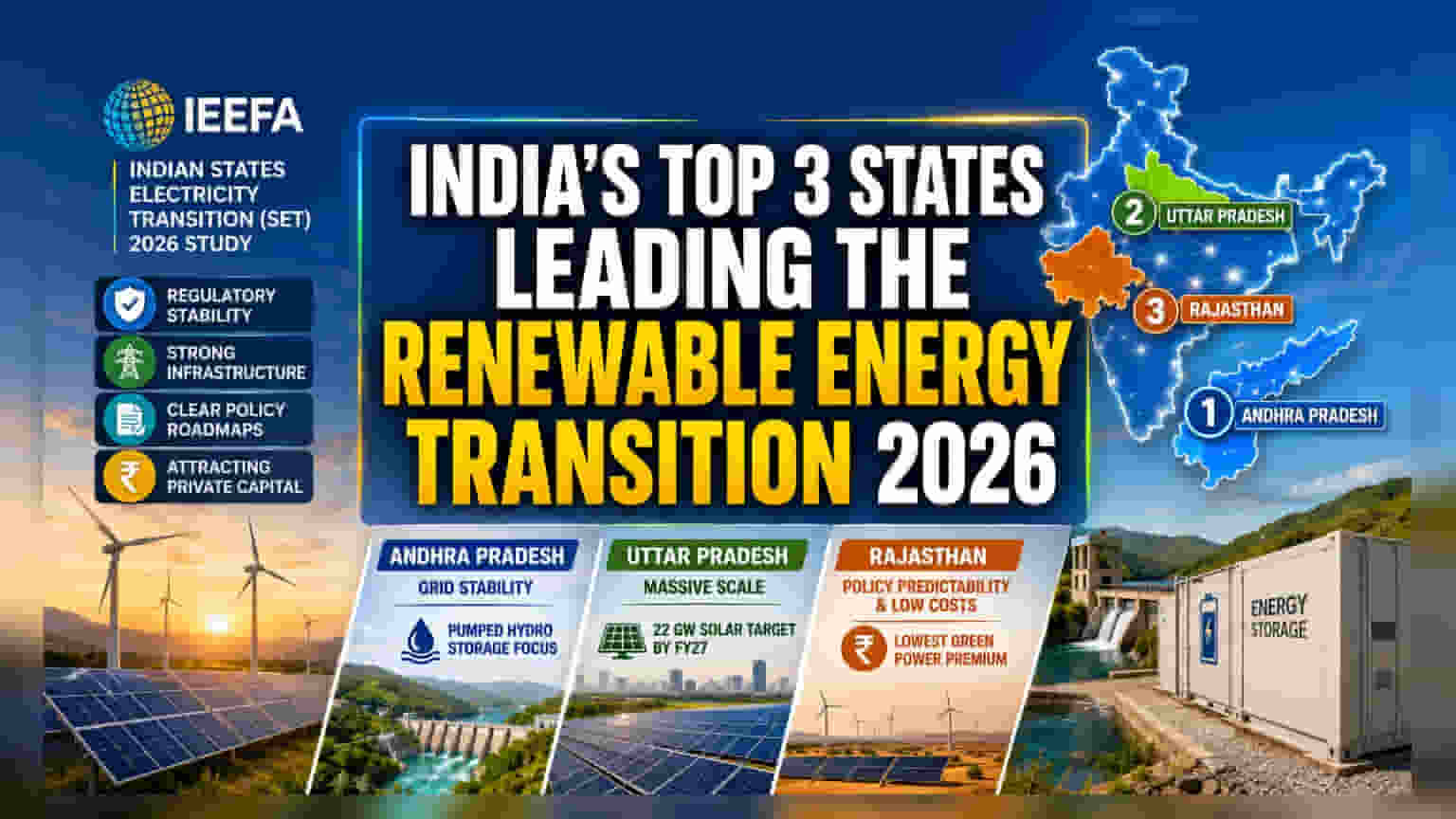

The Institute for Energy Economics and Financial Analysis (IEEFA) released its annual Indian States Electricity Transition (SET) 2026 study, evaluating 21 Indian states on their readiness for the renewable energy shift. The report identifies Andhra Pradesh, Uttar Pradesh, and Rajasthan as the frontrunners for private capital. These states have been recognized for their regulatory stability, infrastructure development, and clear policy roadmaps, which are key factors that attract long-term investments in clean energy projects.

Why This Matters For Investors

For investors in the power sector, state-level performance is as important as company-level financial health. Renewable energy projects require land, grid connectivity, and stable off-take agreements (contracts to buy the power). When a state shows high readiness, it reduces the risk of project delays, land acquisition issues, or policy reversals. Investors often look at these rankings to assess which markets offer a safer and more predictable environment for capital spending, potentially leading to better return on investment over the long term.

State-Specific Strengths

Each of the top three states has secured its position by tackling different challenges in the energy transition. Rajasthan has gained an edge through policy predictability and low costs, offering one of the lowest green power premiums in the country. This makes it an attractive hub for large-scale solar and wind projects.

Uttar Pradesh is focusing on massive scale, aiming for a 22-gigawatt solar capacity target by FY27. It is also building an ecosystem for the future, with a significant push toward electric vehicle adoption and early development in green hydrogen.

Andhra Pradesh has prioritized grid stability. The state is investing heavily in energy storage, specifically pumped hydro storage, which uses water to store energy and release it when solar or wind power generation drops. This solves the intermittency problem—the issue that renewable power isn't available 24/7—making the state’s grid more reliable for large consumers.

The Real-World Risk Assessment

While state rankings provide a useful guide, investors must keep a balanced view of the sector’s structural risks. Even in high-ranking states, the primary challenge for renewable energy companies often remains the financial health of electricity distribution companies, commonly known as DISCOMs. If a DISCOM is struggling financially, it may delay payments to renewable energy producers, creating cash flow pressure for these companies regardless of how good the state's policies are on paper.

Investors should also note that the rapid transition requires massive investment in grid infrastructure. While states are making progress, grid integration—the ability of the electrical network to handle intermittent power from solar and wind—remains a bottleneck that could cause project delays or curtailment, where power producers are forced to stop generating even when they are ready.

What Investors Should Track

Going forward, the success of these states will depend on execution. Investors should monitor a few key indicators. First, watch for payment cycles from state-owned distribution companies; consistent payments are a sign of a healthy energy market. Second, keep an eye on grid connectivity timelines for new projects, as grid congestion can hurt project returns. Finally, monitor whether states can successfully implement their storage and green energy rules, as this will determine the long-term feasibility of the renewable targets they have set.