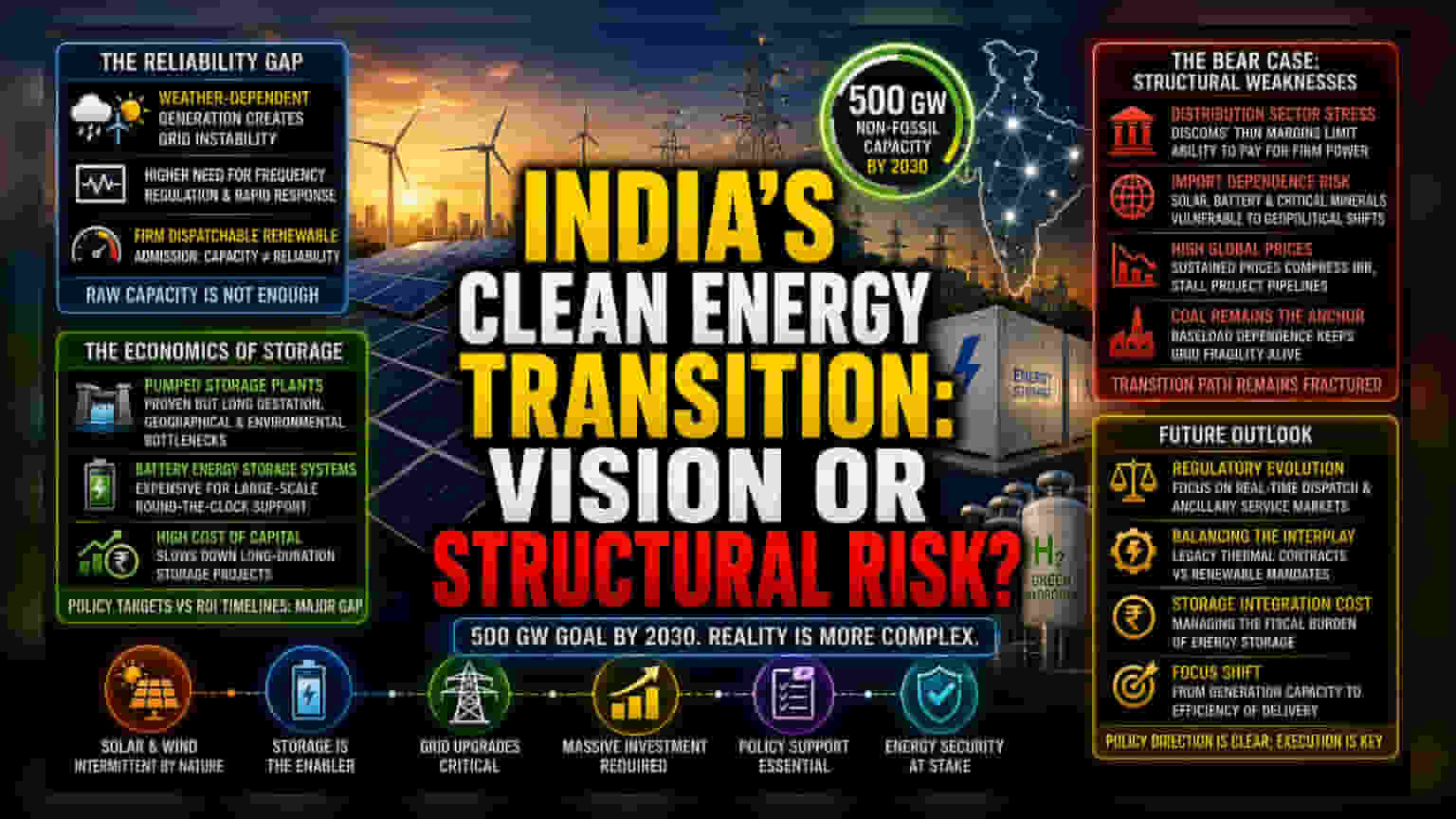

The Reliability Gap

India’s commitment to achieving 500 GW of non-fossil fuel capacity by 2030 is often framed through the lens of pure capacity additions. However, the operational reality is significantly more complex. Relying heavily on solar and wind creates a precarious reliance on weather-dependent generation that current grid infrastructure struggles to balance. The shift toward Firm Dispatchable Renewable Energy reflects an admission that raw capacity is insufficient without massive investment in storage. As the penetration of intermittent sources grows, the requirement for frequency regulation and rapid-response balancing becomes the true, yet under-reported, cost of the energy transition.

The Economics of Storage and Scale

While the National Green Hydrogen Mission and various Production Linked Incentive schemes are designed to catalyze domestic manufacturing, they face stiff headwinds from global supply chain volatility and the high cost of capital for long-duration storage projects. Pumped Storage Plants, though proven for duration, have long gestation periods and face geographical and environmental bottlenecks. Conversely, Battery Energy Storage Systems remain prohibitively expensive for large-scale, round-the-clock grid support without significant government subsidies. The disconnect between policy-set targets and private-sector return-on-investment timelines remains the most persistent friction point in the nation's energy transformation.

The Bear Case: Structural Weaknesses

The transition is not without significant downside risks. Contractual stress within the distribution segment remains a systemic hurdle, as many state-owned utilities operate with thin margins, limiting their ability to absorb the premiums associated with firm power. Furthermore, the reliance on imported components for the solar and battery supply chains leaves the sector vulnerable to geopolitical shifts and price spikes. Should global prices for lithium-ion or critical minerals remain elevated, the internal rate of return for developers will compress, potentially stalling project pipelines. Additionally, the aggressive push for decarbonization ignores the ongoing reality that coal-based thermal power remains the primary, cost-effective anchor for baseload demand, suggesting that grid fragility will persist for the remainder of the decade.

Future Outlook: Policy vs. Reality

Moving forward, market participants should focus on the regulatory evolution of the power market, particularly regarding real-time dispatch and ancillary service markets. Investors are closely watching how the government manages the interplay between legacy thermal contracts and new renewable mandates. While the policy direction is clear, the path to 2030 remains contingent upon resolving the grid's technical limitations and managing the fiscal burden of storage integration. The focus has shifted from mere generation capacity to the efficiency of the delivery mechanism itself.