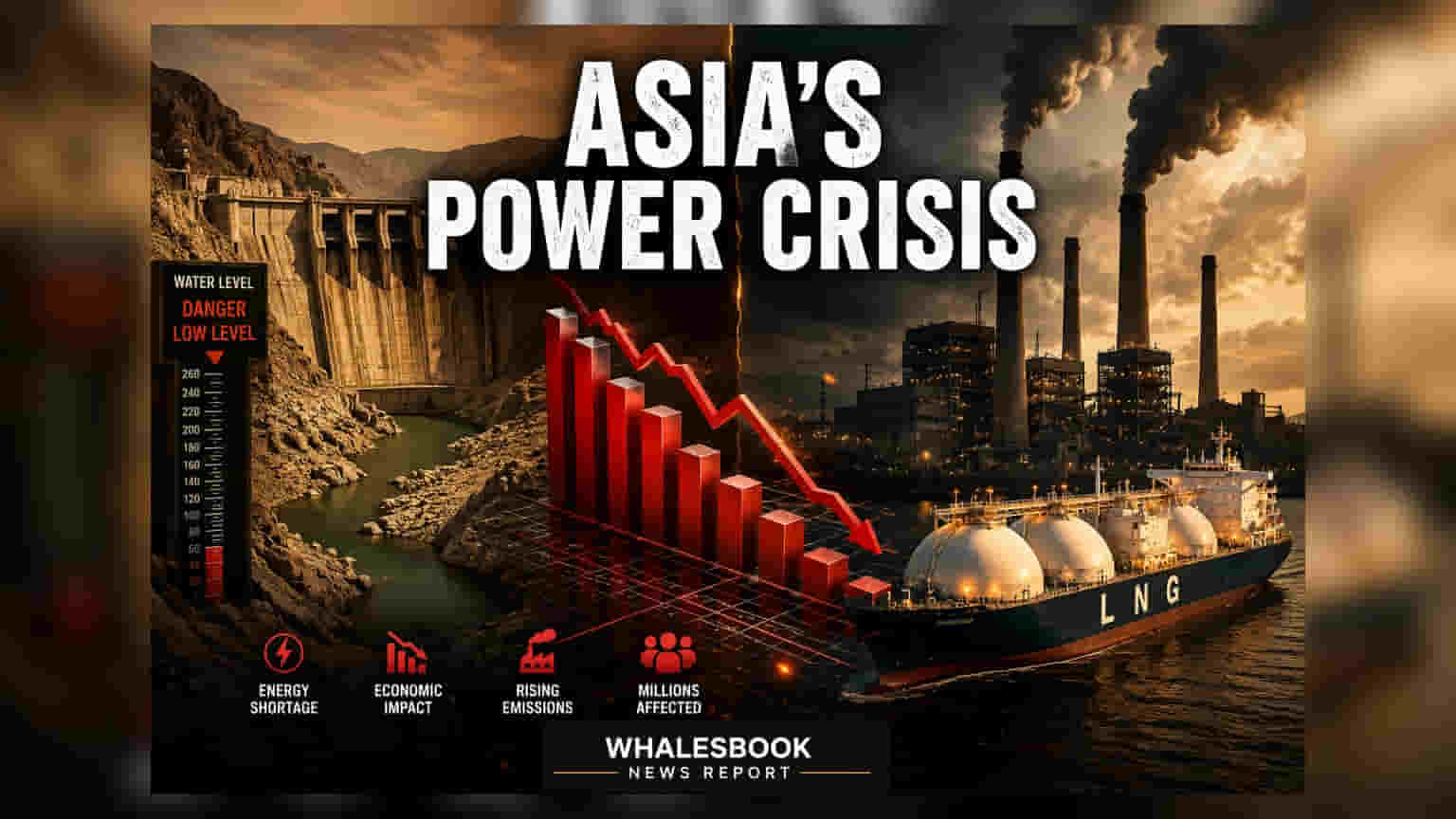

India’s hydropower generation fell by 6.3 average gigawatts in June 2026 as El Niño weather patterns reduced reservoir levels. To bridge the gap, coal-fired power plants ramped up production by 20.7 gigawatts. This shift highlights a challenging period for energy producers as the region relies more heavily on thermal power to meet rising electricity demand.

Hydropower generation across India experienced a significant decline of 6.3 average gigawatts in June 2026 compared to the previous year. This drop occurred while the country simultaneously faced a substantial rise in total electricity demand, which increased by 24.3 average gigawatts during the same period. The shortfall in water-based power highlights the ongoing influence of the El Niño climate phenomenon, which has been associated with suppressed monsoon rainfall and lower water inflows into key reservoirs.

Thermal Power Reliance Increases

With hydropower capacity constrained, the Indian power sector turned to coal and other thermal sources to maintain grid stability. Coal-fired power plants increased output by 20.7 average gigawatts to compensate for the missing hydro energy and to meet the overall surge in consumption. Additionally, renewable energy sources such as solar and wind contributed 9.4 average gigawatts to the grid, helping to offset some of the pressure on the system. This trend of relying on fossil fuels during periods of low hydroelectric generation underscores the practical challenges currently facing the country’s energy transition goals.

Regional Impact and Future Outlook

India and Vietnam were identified as the primary drivers of this regional trend, together accounting for over 80% of the decline in Asian hydropower generation. The World Meteorological Organization has cautioned that El Niño conditions are expected to persist through the third quarter of 2026. This period, covering July to September, may see continued heatwaves and reduced rainfall in several Asian markets, including India, Bangladesh, the Philippines, and Vietnam. If these dry conditions continue, utilities may be required to maintain higher levels of coal and liquefied natural gas (LNG) inventories to ensure reliable electricity supply.

Investors in the power sector may track how this increased reliance on coal and LNG affects the profit margins of power generation companies. While higher demand supports revenue, utilities with a greater share of thermal power may face different cost dynamics due to fluctuations in fuel prices and potential supply chain pressures. Conversely, companies heavily dependent on hydroelectric projects may see continued pressure on their generation volumes and, by extension, their operating performance through the next quarter. The key monitorable will be the actual rainfall levels throughout the monsoon season and whether grid demand remains elevated as thermal reliance persists.