THE SEAMLESS LINK

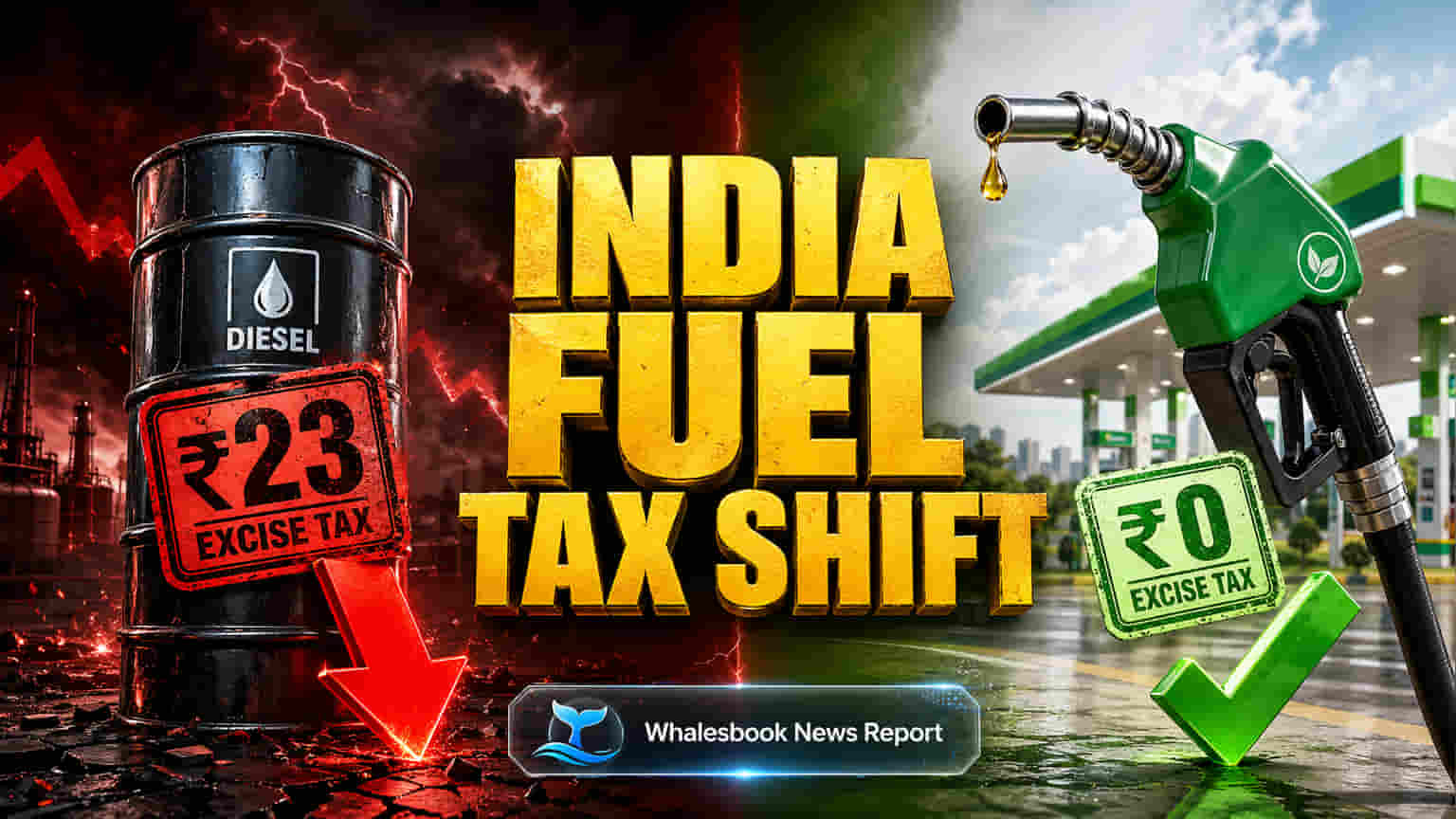

The Indian government's latest adjustment to petroleum product export levies, effective May 1, 2026, signals a strategic recalibration prioritizing national energy security over maximizing export revenues for refiners. This move, which increases duties on diesel and aviation turbine fuel (ATF) while leaving petrol exports untaxed, directly impacts the profitability calculus for India's significant refining sector. The policy underscores a deliberate effort to retain fuel supplies domestically amidst fluctuating global energy markets, a strategy that warrants a closer look at its implications for refiner margins and competitive positioning.

Margin Squeeze and Competitive Disadvantage

The revised export duties of ₹23 per litre on diesel and ₹33 per litre on ATF are designed to curb outbound shipments, thereby ensuring greater domestic availability. However, this policy directly targets the profitability of Indian refiners, particularly those with a substantial export focus. Companies like Reliance Industries, which operates a large Special Economic Zone (SEZ) refinery primarily for exports, face particular scrutiny. While historically SEZ units have seen exemptions from such levies, clarity on their status remains a key factor influencing margins. Should these exports become subject to the new duties, Reliance's refining margins could be compressed by approximately USD 2 per barrel. This contrasts with refiners in regions like Singapore or the Middle East, who may not face similar domestic-oriented taxation, potentially placing Indian exporters at a competitive disadvantage in international markets. The government's explicit aim is to ensure local fuel availability, a move that signals a departure from maximizing export profits during periods of global price volatility.

Historical Context and Sector Valuation

Past instances of increased export levies by the Indian government have historically led to stock market volatility for oil marketing companies (OMCs) and refiners. For example, a significant hike in windfall taxes in April 2026 saw Reliance Industries' shares decline by over 4-5% following earlier reintroductions of similar levies. This suggests that investors often react bearishly to interventions that crimp export-driven profitability. The current P/E ratios for major Indian OMCs reflect this dynamic. Indian Oil Corporation (IOCL) trades at a P/E of approximately 5.86, Bharat Petroleum (BPCL) at around 5.36, and Hindustan Petroleum (HPCL) at about 5.14. These relatively low P/E ratios, often considered indicative of value stocks, may partly reflect investor anticipation of regulatory interventions or slower growth prospects due to such policies. Reliance Industries, with a P/E ratio closer to 24.06, presents a different valuation profile, possibly reflecting its diversified business segments beyond just refining and exports.

The Bear Case: Regulatory Risk and Margin Erosion

The recurring nature of export levies introduces significant regulatory risk for Indian refiners. The government's continued reliance on these taxes as a tool to manage domestic energy security, especially amidst global geopolitical crises like the West Asia war, implies that such interventions could become more frequent. Unlike nations with more stable export tax regimes, Indian refiners must contend with policy shifts that directly impact their profitability. While the recent duties represent a reduction from earlier peaks in April 2026 (e.g., ₹55.5 per litre for diesel), the fact that they remain substantial—₹23 for diesel and ₹33 for ATF—highlights the government's leverage. Furthermore, factors beyond export duties, such as increased freight costs for Very Large Crude Carriers (VLCCs) and potential fuel losses at complex refineries, can further erode realized margins, making reported gross refining margins (GRMs) potentially misleading. The lack of clarity on SEZ unit exemptions for Reliance Industries also adds to this uncertainty, creating a potential bear case centered on margin erosion and policy unpredictability.

Future Outlook and Analyst Sentiment

Analyst sentiment towards the Indian refining sector remains cautiously optimistic, with a general consensus leaning towards 'Buy' for major OMCs like IOCL, BPCL, and HPCL. However, these recommendations often come with caveats regarding regulatory headwinds. While measures like excise duty cuts provide some relief to Oil Marketing Companies (OMCs) by reducing marketing losses, they cap the upside for integrated refiners like Reliance Industries. The government's ability to balance domestic supply needs with the profitability of its refining sector will be crucial. Should global energy prices remain volatile, further policy adjustments cannot be ruled out, potentially leading to continued scrutiny of refiner margins and the strategic viability of export-oriented operations.