The Middle East Flashpoint and India's Response

The recent escalation in the US-Israeli conflict with Iran and the demise of Supreme Leader Ayatollah Ali Khamenei have plunged the Middle East into a state of heightened geopolitical turmoil, directly impacting global energy markets. Threats to the strategic Strait of Hormuz, a chokepoint responsible for approximately 20% of global oil flows, have led to a de facto disruption, sending crude oil prices sharply higher. By March 3, 2026, Brent crude futures surged past $81 per barrel, reaching levels not seen since early 2025. West Texas Intermediate (WTI) crude also saw significant gains, trading above $72. This volatility has directly pressured the Indian Rupee, which weakened to approximately 91.9 per US dollar on March 3, 2026, reflecting heightened import costs and market uncertainty. Analysts warn that a sustained $10 per barrel increase in crude oil prices could widen India's current account deficit by 0.4% of GDP and add significantly to its annual import bill.

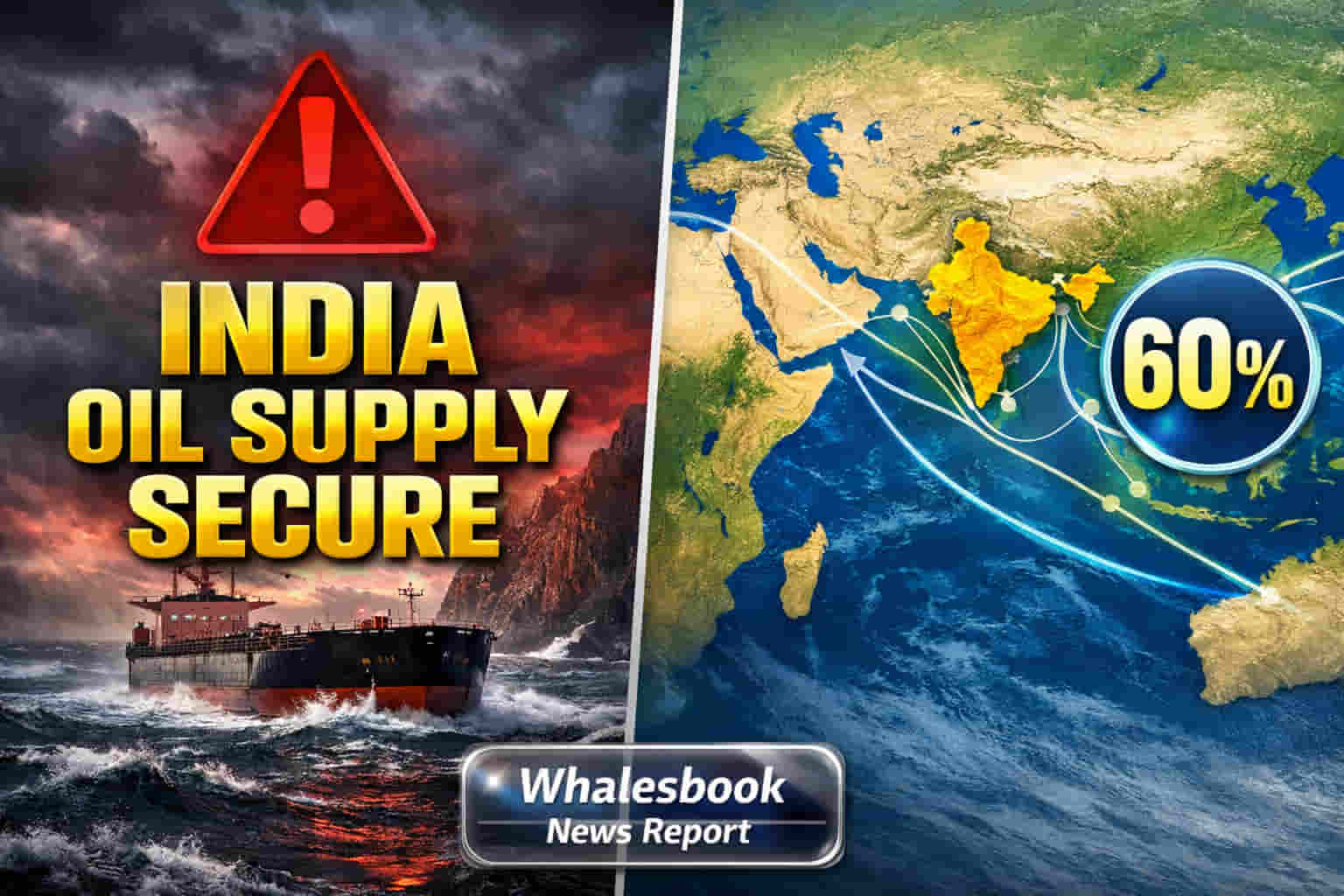

India's Diversified, Yet Vulnerable, Import Strategy

While government sources initially suggested that 60% of India's crude supplies bypass the Strait of Hormuz, more granular analysis indicates that between 35% and 50% of crude imports, and a higher proportion of Liquefied Natural Gas (LNG) and Liquefied Petroleum Gas (LPG) supplies, transit this critical waterway. India, importing nearly 90% of its crude oil requirements, has strategically diversified its sourcing, with imports from Saudi Arabia hitting a record high in February 2026, and Russia remaining its largest supplier during the same period. However, this pivot to Middle Eastern suppliers heightens exposure to Hormuz-related risks. The nation holds strategic reserves and commercial inventories theoretically capable of covering approximately 60 days of crude imports, offering some short-term buffer. Yet, the immediate risk lies in price surges, not outright supply absence, impacting inflation and trade balances.

The Russian Crude Conundrum and Trade Diplomacy

India finds itself navigating a complex geopolitical tightrope regarding its continued purchases of Russian crude oil. Following an interim trade agreement with the US in early February 2026, which included India's commitment to curb Russian oil imports in exchange for reduced US tariffs, the situation became muddled. A subsequent US Supreme Court ruling striking down broad tariffs introduced uncertainty, while new global tariffs imposed by the US administration under Section 122 of the Trade Act potentially maintain pressure. Despite these developments, Russian oil remains India's top supplier, with February 2026 arrivals around 1 million barrels per day. This strategy, driven by commercial considerations and widening discounts on Russian grades, risks diplomatic friction, even as formal trade agreements remain elusive.

Sector Performance and Valuation Amidst Volatility

The Indian energy sector, represented by the Nifty Energy Index, has shown resilience, trading at a P/E ratio of 15.3 as of early March 2026. Major players like Bharat Petroleum Corporation (BPCL) and Hindustan Petroleum Corporation (HPCL) exhibit attractive valuations. BPCL trades at a P/E ratio around 6.6, with a market capitalization nearing ₹1.63 trillion. HPCL boasts a P/E ratio below 6 and a market cap of approximately ₹90,300 crore. However, the sector faces significant headwinds. Rising crude oil prices, while potentially boosting revenues for refiners, directly increase the cost of refined products and inflate the import bill. The weakening rupee further exacerbates these import costs. Analysts remain cautious, with projections suggesting continued volatility and geopolitical risk as a major wildcard for India's economic stability.

The Forensic Bear Case: Underlying Risks and Vulnerabilities

Despite India's strategic efforts to secure energy supplies, several critical risks persist. The continued reliance on Russian oil, even at reduced volumes, carries the potential for diplomatic repercussions from the US, particularly if trade deal finalization stalls. While crude imports may be somewhat insulated by alternative routes and reserves, India's exposure to LNG and LPG transiting the Strait of Hormuz is significantly higher, posing a more acute vulnerability. The de facto closure of the strait, coupled with escalating shipping and insurance costs, means that even diversified routes will face price inflation. Furthermore, the geopolitical instability has already prompted rerouting of vessels and increased freight rates, impacting India's broader trade flows beyond just energy commodities. The recent drone strike on Saudi Aramco's Ras Tanura refinery underscores the fragility of regional energy infrastructure, a risk that could directly impact India's primary suppliers.

Future Outlook: Navigating Uncertainty

Looking ahead, market sentiment remains cautious, with analysts expecting continued price volatility for crude oil. Bernstein has revised its 2026 Brent oil price assumption upwards to $80 per barrel, acknowledging the substantial geopolitical risks as a key determinant of future prices. For India, balancing energy security imperatives with geopolitical alignments remains a paramount challenge. The nation's ability to manage its energy import bill, control inflation, and maintain currency stability will hinge on the de-escalation of Middle East tensions and its strategic navigation of international energy policy. The focus on clean energy investments, though significant, will be tested by the immediate need to secure fossil fuel supplies in a turbulent global environment.