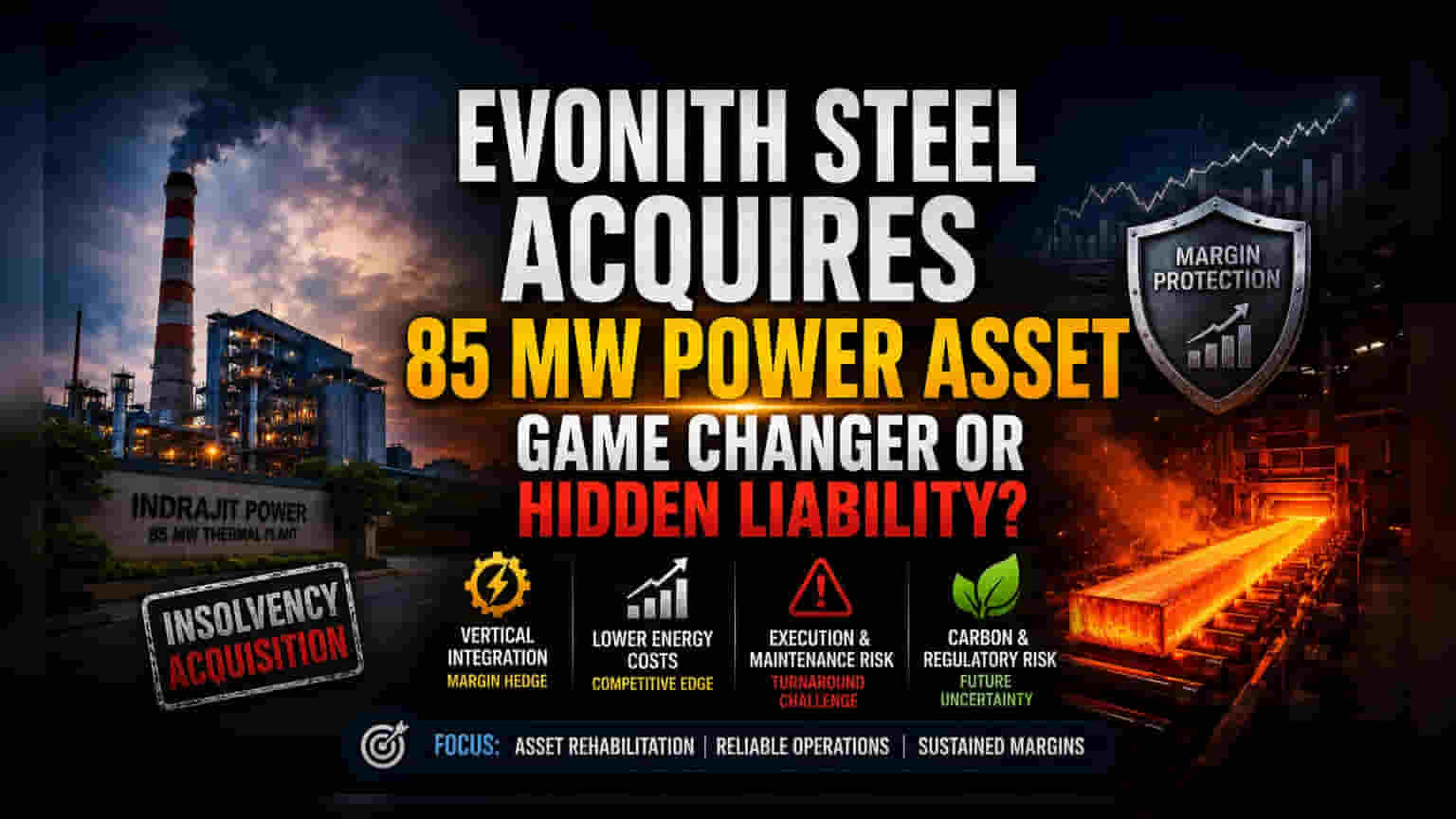

Vertical Integration as a Margin Hedge

Transitioning from dependence on grid-level power procurement to captive generation is a classic play for steel manufacturers attempting to insulate bottom-line performance from energy price volatility. By securing the Indrajit Power asset through the insolvency process, Evonith Steel effectively eliminates the intermediary premium on power supply for its primary Wardha manufacturing site. This operational proximity allows the company to integrate energy logistics directly into its value chain, potentially lowering the per-unit production cost of finished steel in a market where energy intensity often dictates competitive pricing power.

The Operational Reality of Distressed Assets

While the acquisition secures 85 MW of thermal capacity, the integration of an asset passing through the National Company Law Tribunal process carries inherent execution risks. Historically, plants sourced via insolvency resolution require significant capital expenditure to restore peak operating efficiency after periods of financial distress. Investors should note that while the purchase price of ₹232 crore appears accretive compared to greenfield project development costs, the ongoing maintenance and compliance expenses associated with a legacy thermal facility in Maharashtra will weigh on near-term cash flow. Unlike market leaders that utilize diverse renewable energy portfolios, Evonith remains heavily committed to coal-fired thermal generation, creating potential vulnerability to future carbon emission regulations and environmental audit mandates.

The Forensic Bear Case

Acquiring a distressed thermal asset during a period of shifting energy policy presents a multi-layered risk profile. The reliance on coal-based power, while efficient for current furnace technology, may become a structural liability as the Indian government accelerates the integration of green energy mandates for the heavy industrial sector. Furthermore, the management must overcome the historical operational hurdles that drove Indrajit Power into insolvency originally. If the facility fails to reach its 85 MW nameplate capacity or faces frequent downtime due to aging infrastructure, Evonith Steel will be forced to return to the spot power market, effectively negating the expected cost savings. Management’s ability to turn around this specific asset will be the primary metric for judging capital allocation efficiency over the next three fiscal quarters.

Forward-Looking Guidance

Market participants will likely focus on the speed of asset rehabilitation and the resulting impact on operating margins. If successful, the reduction in energy overhead will provide a cleaner balance sheet and greater flexibility during cyclical downturns in steel prices. However, until the power facility achieves steady-state operation, the market may maintain a neutral stance, balancing the long-term cost benefits against the immediate liquidity outflow required for facility upgrades.