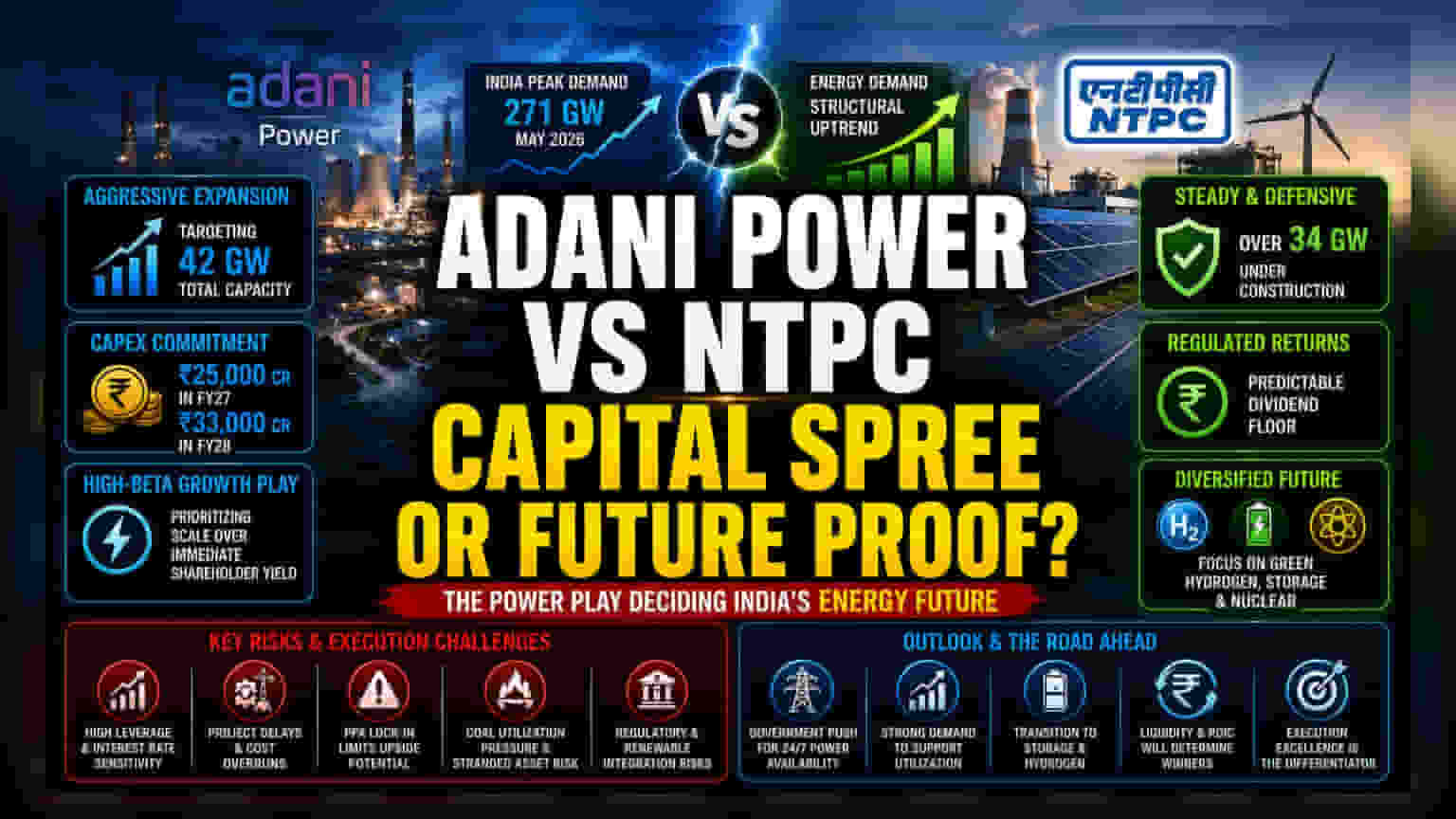

The Capital Expenditure Trap

The strategic pivot by Adani Power and NTPC toward commissioned capacity marks a transition from cyclical profit-seeking to a utility-like asset-heavy model. By prioritizing massive portfolio expansion—Adani targeting a 42-gigawatt footprint and NTPC advancing over 34 gigawatts of construction—both firms are effectively betting that long-term Power Purchase Agreements (PPAs) will outpace the cost of capital. However, this creates a rigorous dependency on execution efficiency. Adani Power’s projected capital expenditure, scaling from ₹25,000 crore in FY27 to ₹33,000 crore in FY28, highlights a heavy reinvestment cycle that sacrifices immediate shareholder yield for asset dominance.

Sector Benchmarking and Valuation Dynamics

Unlike traditional utilities, these companies are currently trading at premiums reflective of growth expectations rather than historical dividend yields. NTPC maintains a more defensive stance, utilizing its regulated return model to provide a predictable dividend floor. In contrast, Adani Power acts as a high-beta growth vehicle. Market data indicates that while both benefit from the structural tailwind of rising national peak demand—which hit 271 GW in late May 2026—the market is increasingly scrutinizing the Return on Invested Capital (ROIC) of these new projects. Investors are pricing these stocks not on current thermal margins, but on the successful integration of green hydrogen, pumped storage, and nuclear assets.

The Forensic Bear Case: Execution and Leverage

Despite the optimistic growth narrative, several structural risks remain. The aggressive expansion phase necessitates sustained debt financing, leaving both firms sensitive to interest rate fluctuations and potential cost overruns in large-scale infrastructure projects. Adani Power, in particular, faces the challenge of managing a balance sheet designed for rapid scaling; any delay in commissioning these multi-gigawatt projects could lead to significant interest coverage pressure. Furthermore, while long-term PPAs hedge against merchant price volatility, they also lock in fixed returns, potentially capping upside if electricity prices spike during national shortages. Regulatory shifts regarding renewable integration could also pressure existing thermal asset utilization rates, forcing these companies to manage the delicate transition from coal dominance to diversified energy fleets without suffering stranded asset impairment.

Outlook on Demand and Policy Integration

Forward projections remain tied to the government’s push for 24/7 power availability. Management teams are banking on a sustained economic recovery to keep utilization high. However, the true test lies in the transition to non-thermal energy. As both companies pivot into battery storage and hydrogen, they move into nascent markets where technology costs remain volatile. The coming fiscal years will be defined by their ability to maintain liquidity while transitioning to these capital-intensive, lower-margin new energy technologies.