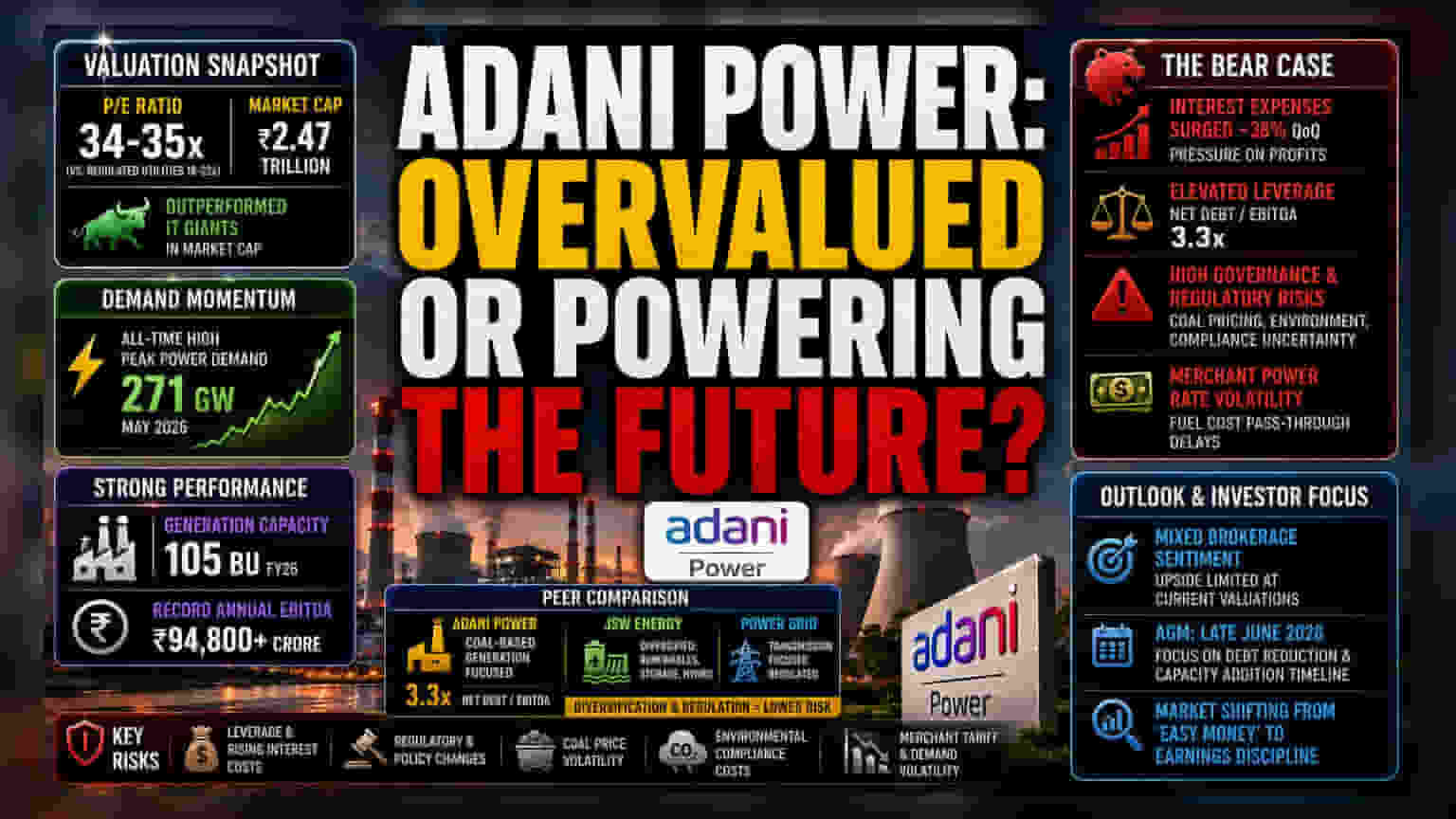

The Valuation Gap

Adani Power currently trades at a valuation that reflects strong market confidence in India's industrial energy demand, with the stock recently outperforming IT bellwethers in market capitalization. As of early June 2026, the company maintains a price-to-earnings ratio near 34-35x. While this valuation is supported by a robust 105 BU generation capacity in FY26, it sits at a premium compared to more stable, regulated utility counterparts. The current trading range suggests that the market has largely priced in the immediate benefits of higher power purchase agreement (PPA) coverage, leaving less room for error if merchant power rates face further volatility.

The Analytical Deep Dive

Market interest is anchored by India’s all-time high peak power demand, which reached 271 GW in May 2026. This environment has allowed private thermal generators to capitalize on tight supply-demand balances. Compared to peers like JSW Energy, which has diversified significantly into storage and pumped hydro, or the transmission-focused Power Grid Corporation, Adani Power remains a concentrated bet on coal-based thermal generation. While the company achieved a record annual EBITDA of over Rs 94,800 crore across its portfolio, the specific financial resilience of the power generation arm is being tested by an aggressive capital expenditure cycle. Analysts are now focusing on the company's ability to maintain its 3.3x Net Debt/EBITDA ratio while funding its next phase of infrastructure growth.

The Forensic Bear Case

Despite the positive momentum, institutional caution remains evident. The stock carries elevated governance and leverage risks that contrast sharply with the more conservative balance sheets of state-backed utilities. In the most recent quarterly data, interest expenses surged by approximately 38%, a development that directly challenges the sustainability of its net profit growth. Furthermore, while the company has largely moved past US-related legal scrutiny, the sector remains highly sensitive to regulatory shifts in coal pricing and environmental compliance. Unlike Torrent Power, which benefits from lower AT&C losses and a stable distribution monopoly, Adani Power’s reliance on generation makes it more vulnerable to cyclical swings in merchant tariffs and fuel cost pass-through delays.

Future Outlook

Brokerage consensus remains mixed; while some firms maintain aggressive price targets citing the ongoing demand upcycle, others have shifted to 'Hold' ratings, citing rich valuations and the limited near-term upside for earnings. With the Annual General Meeting scheduled for late June 2026, the primary focus for stakeholders will be the management’s guidance on debt reduction and the execution timeline for new capacity additions. Investors appear to be recalibrating their expectations as the 'easy money' phase of the power sector rally potentially gives way to a period of earnings-driven selection.