Many taxpayers are receiving tax notices despite TDS being deducted due to data mismatches. Common triggers include unreported income and differences between taxpayer claims and Form 26AS records. Checking your Annual Information Statement (AIS) before filing is crucial to avoid these automated alerts.

What Happened

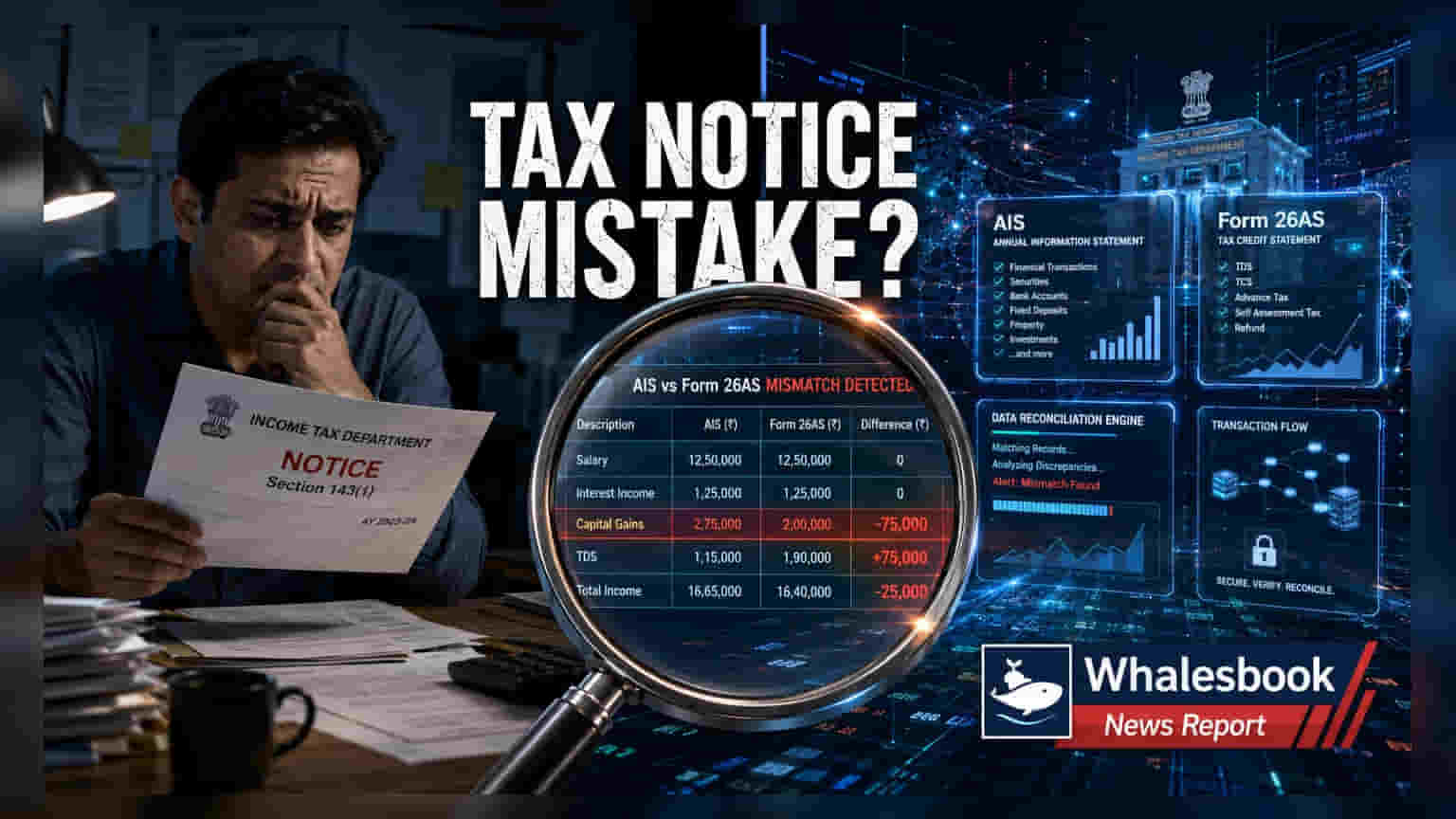

Taxpayers across India are increasingly receiving notices from the Income Tax Department even when they believe their tax obligations have been fully met through Tax Deducted at Source (TDS). Rather than indicating tax evasion, these notices are often generated by a modern, automated system that identifies data mismatches. The department now cross-references personal tax filings with central databases, including the Annual Information Statement (AIS) and Form 26AS, making any omission or inconsistency immediately apparent to tax authorities.

Why Income Reporting Gaps Occur

A primary driver of these notices is the incomplete reporting of income. Many taxpayers focus solely on their primary salary as reflected in Form 16, while overlooking secondary sources. These include interest from savings accounts, fixed deposits, dividends, rental income, and gains from the sale of shares or mutual funds. Financial institutions are now required to report these transactions to the government electronically, meaning that if a taxpayer does not manually declare these amounts, the system automatically flags a discrepancy.

The Importance of TDS Reconciliation

Even when tax is deducted by an employer or bank, discrepancies can arise. A notice may be triggered if the entity that deducted the tax—the deductor—files an incorrect statement, enters an incorrect Permanent Account Number (PAN), or revises their filing after the taxpayer has already submitted their return. Relying solely on a salary certificate is no longer sufficient; investors and professionals must reconcile their TDS claims against the official Form 26AS, which serves as the tax credit statement recognized by the Income Tax Department.

High-Value Transactions and Reporting

The tax department keeps a close watch on significant financial movements, often referred to as High-Value Transactions (HVTs). This includes large cash deposits, property purchases, major investments, or significant foreign remittances. When these transactions are reported by banks or registrars but not reflected in the taxpayer’s declared income, the department will issue a notice seeking clarification on the source of funds. These flags are designed to verify that the taxpayer’s spending and investment power align with their disclosed financial profile.

What Investors Should Track Next

To minimize the risk of receiving a notice, taxpayers should adopt a proactive approach before the final filing deadline. First, download and thoroughly review the Annual Information Statement (AIS) and Taxpayer Information Summary (TIS) available on the income tax portal. These documents provide a comprehensive view of the data the government already holds regarding your finances. If you receive a notice, do not panic; identify the specific assessment year and the nature of the discrepancy. Reconcile your records with bank statements and investment proofs before providing a factual response through the online portal. Ensuring all income streams—no matter how small—are reported accurately is the most effective way to avoid unnecessary scrutiny and ensure that your tax refunds are processed without delay.