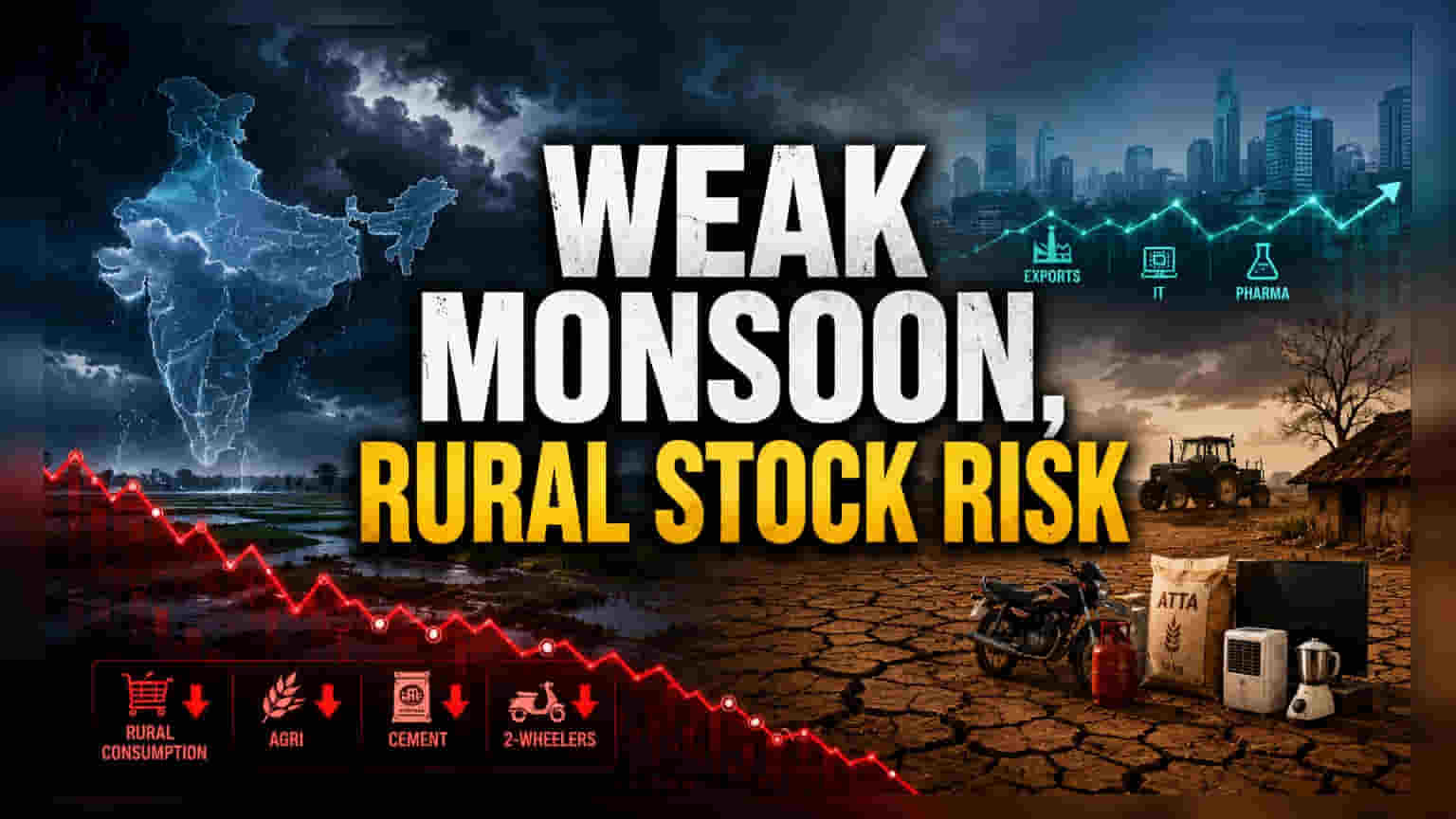

Concerns over a weak 2026 monsoon are highlighting potential risks for rural demand-dependent sectors. While the broad market outlook remains steady, investors should watch for selective pressure on farm equipment, two-wheelers, and rural-focused consumer goods. Conversely, urban-centric businesses and export-heavy sectors like IT are expected to remain insulated.

What Happened

The 2026 monsoon season has become a key point of focus for the Indian markets as reports of potential rainfall deficits emerge. While investors often worry about a broad economic downturn during weak monsoon years, the current market structure suggests a more specific, selective impact rather than a systemic crash. The primary concern is not a market-wide failure, but rather how reduced agricultural income could dampen spending power in India's rural regions.

Why Rural Demand Matters

Agriculture remains a pillar of the Indian economy, supporting nearly half the workforce and contributing a significant portion to the GDP. When rainfall is insufficient, the Kharif (summer) crop output can decline, directly impacting the income of farmers. Because a large section of the population relies on this income to make purchases, a weak monsoon often leads to a slowdown in discretionary spending. Companies that rely heavily on rural sales—such as those selling tractors, motorcycles, and daily-use household items—are usually the first to feel this pinch.

Sectors Under Potential Pressure

Investors are keeping a close watch on companies where rural sales drive a significant portion of revenue. Farm equipment manufacturers, particularly tractor makers, face the most direct risk, as low crop income reduces the ability of farmers to upgrade or buy machinery. Two-wheeler manufacturers, which have seen growth from rural penetration in recent years, could also face volume pressure if rural wallets shrink. Additionally, consumer goods firms that have built extensive distribution networks in villages may see lower volume growth, as rural consumers tend to cut back on non-essential purchases when farm income is uncertain. Rural lenders and microfinance institutions are also on the watchlist, as a potential hit to farm incomes can make it harder for borrowers to repay loans on time.

Segments Likely To Remain Shielded

Not all parts of the market are vulnerable to rainfall patterns. Businesses that cater primarily to urban consumers often move to a different rhythm and are less sensitive to monsoon performance. Furthermore, export-oriented sectors, such as IT services and pharmaceutical companies, generate the bulk of their revenue from global markets, meaning they remain largely de-linked from local weather events. Private sector banks and large financial institutions with a diversified loan book—balancing both urban and rural exposures—are also expected to remain more resilient compared to those focused exclusively on rural credit.

What Investors Should Track Next

For investors evaluating the impact on their portfolio, the focus should be on data rather than sentiment. Key monitorables include official updates on rainfall distribution and water reservoir levels, which help sustain crops even if the rain is slightly below average. Additionally, tracking Kharif sowing data as it becomes available will provide a clearer picture of potential crop output. If the deficit leads to high food inflation, it could also impact broader economic policy, such as interest rate decisions, which remains a key monitorable for the wider equity market.