The Anatomy of the Financial Stress Cycle

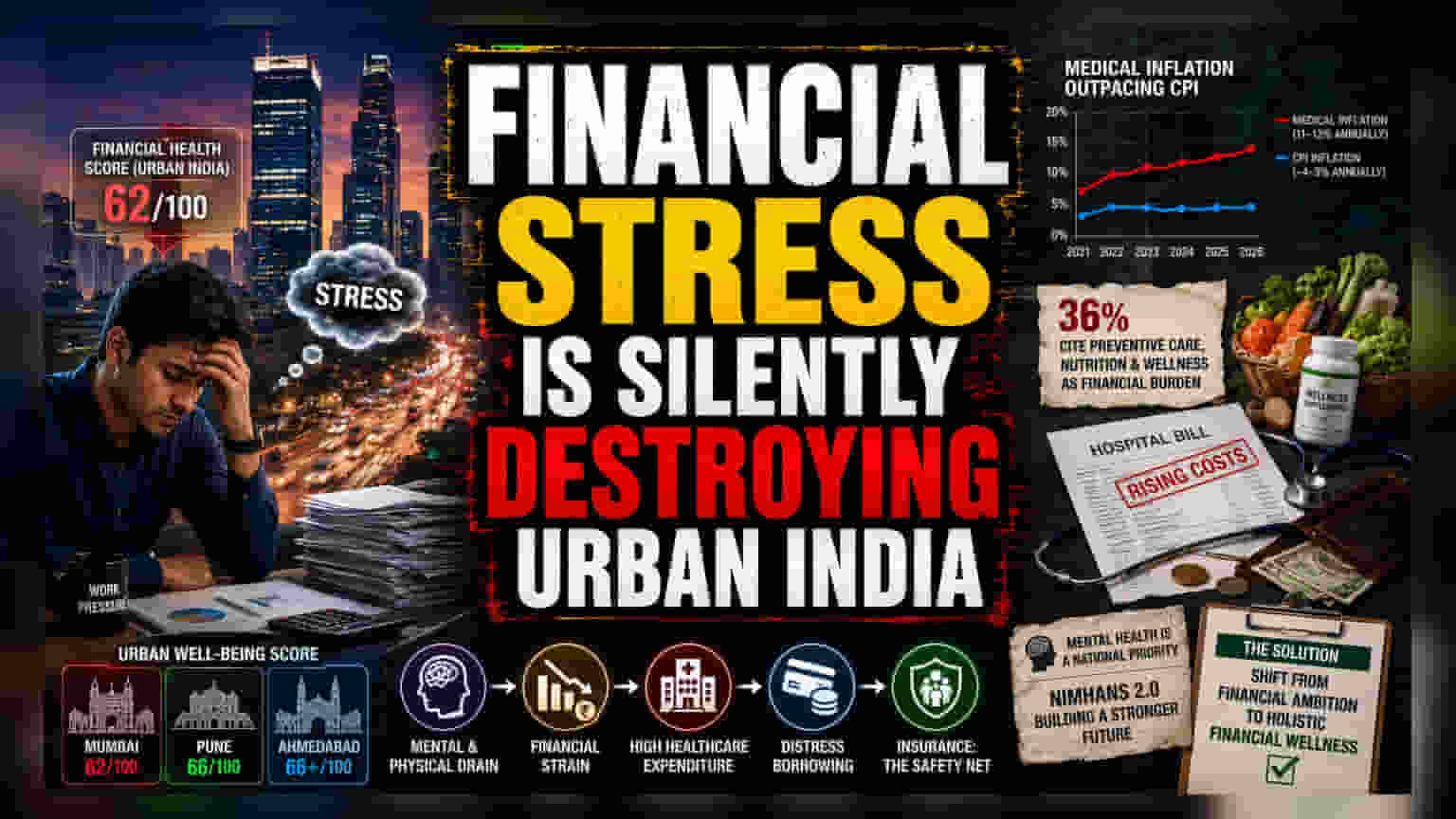

Urban India is currently grappling with a paradox where the pursuit of prosperity is actively undermining the foundation of individual productivity. The latest data from the India Health Quotient 2026 study highlights that financial health is the weakest pillar of the urban experience, scoring a mere 62 out of 100. This struggle creates a self-reinforcing loop: the drive to secure future wealth generates acute, unmanageable stress, which in turn manifests as physical and mental degradation, leading to further financial outlays for healthcare.

The Health Debt Trap

Beyond mere savings accounts and portfolio returns, the real cost of this ambition is being paid in 'health debt.' Approximately 36% of urban residents report that the necessary expenditures on preventive care, high-quality nutrition, and wellness supplements act as a primary source of economic strain. This pressure is compounded by medical inflation, which has consistently tracked between 11% and 13% annually—significantly outstripping general consumer price indices. For many, this leaves little room for error, as an unexpected health event can quickly turn a manageable budget into a cycle of distress borrowing.

Disparities in Urban Well-being

Evidence suggests that the pressure is not distributed equally. While larger metropolitan hubs like Mumbai scored lower (62/100) on the overall well-being index, smaller cities, including Pune and Ahmedabad, demonstrated higher resilience with scores reaching 66 or above. This geographical divide hints at the hidden costs of life in major economic centers, where higher living expenses and greater professional competition exacerbate the feeling of falling behind. Furthermore, the salaried demographic reports lower well-being outcomes compared to the self-employed, suggesting that the traditional corporate employment model may be failing to buffer against the modern stressors of the Indian economy.

The Forensic View: Risks and Structural Weakness

From a risk-averse perspective, the reliance on out-of-pocket healthcare financing represents a structural vulnerability for the Indian middle class. With roughly 60% of total health expenditure still funded through personal reserves, the demographic dividend is increasingly at risk. If current trends continue, the erosion of the workforce’s mental and physical health could dampen the very economic growth that these financial goals were meant to secure. The government’s recent move to strengthen mental health infrastructure, including the announcement of NIMHANS 2.0, reflects an institutional admission that the current health-financial nexus is reaching a breaking point.

Forward Guidance and Outlook

As the economic landscape shifts, the focus is moving from simple wealth accumulation to holistic financial wellness. Analysts note that resilience now depends on shifting household credit from a source of distress to a lever for long-term protection, primarily through increased insurance penetration. Without this transition, the gap between financial ambition and health reality will likely continue to widen, creating a long-term drag on both corporate productivity and national economic stability.