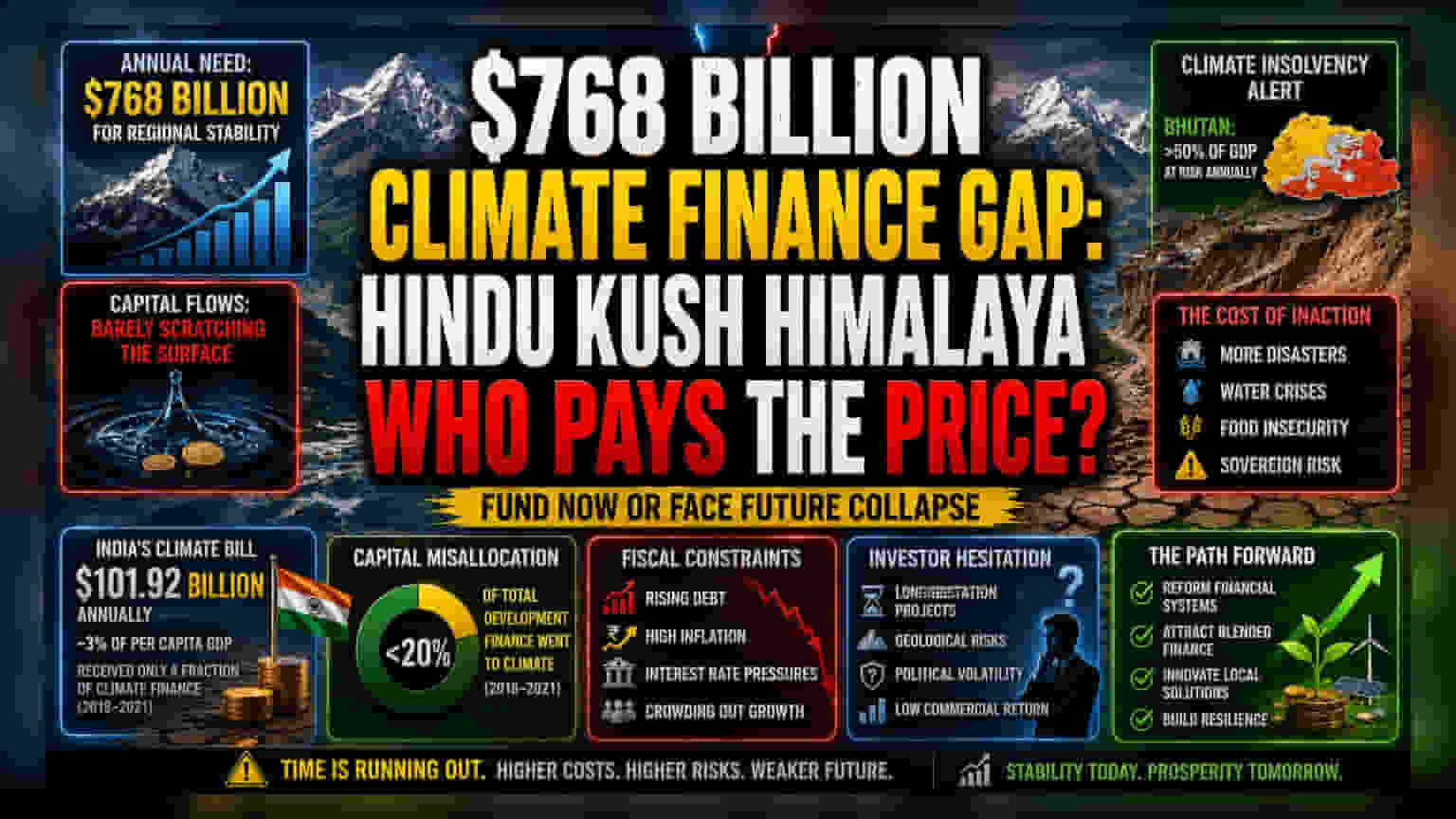

The Capital Allocation Failure

The climate transition in the Hindu Kush Himalaya region is increasingly defined not by technical barriers, but by a catastrophic misallocation of global capital. While the International Centre for Integrated Mountain Development projects a $768 billion annual necessity to secure regional stability, current liquidity flows are barely scratching the surface of these requirements. This structural imbalance represents more than a policy shortfall; it functions as an emerging sovereign risk premium for the involved nations. As governments grapple with the mandate to pivot toward green infrastructure, the inability to bridge this funding gap will likely necessitate higher fiscal deficits or the redirection of funds from core social spending programs.

Sovereign Impact and Fiscal Constraints

For major economies like India and China, the climate finance burden is no longer a peripheral environmental concern but a core macroeconomic variable. India’s requirement of $101.92 billion annually translates to a significant claim on national output, equivalent to roughly 3% of per capita GDP. When viewed alongside historical disbursement data—which saw India receive only a fraction of its total development finance in climate-specific funding between 2018 and 2021—it becomes clear that reliance on external climate concessions is a failing strategy. Meanwhile, smaller regional economies such as Bhutan, where annual needs consume over 50% of GDP, are approaching a state of effective climate insolvency. This trajectory forces a difficult choice: abandon critical infrastructure resilience or accumulate debt levels that may become unsustainable in an era of higher global interest rates.

The Forensic Bear Case

The most immediate danger lies in the disconnect between regional adaptation needs and the private sector’s risk appetite. Most institutional investors remain hesitant to deploy capital into high-altitude water and disaster management projects due to long-term geological and political volatility. Furthermore, the reliance on the public sector to fill this void is structurally flawed. Public budgets in Nepal, Pakistan, and Bangladesh are already under intense pressure from inflationary cycles and external debt servicing costs. If these nations attempt to fund these requirements via domestic credit markets, the resulting crowding-out effect could stifle private enterprise and exacerbate current account deficits, leading to currency devaluation risks that would only increase the cost of future imported climate technology.

Forward Outlook

Future capital flows will likely be dictated by the ability of these nations to reform domestic financial frameworks to attract blended finance, rather than waiting for traditional aid disbursements that have historically proven unreliable. The market is beginning to price in the divergence between countries that can successfully internalize climate costs and those that remain tethered to increasingly expensive international debt. Investors should monitor sovereign credit spreads in the region as a primary indicator of how these fiscal burdens are being reconciled with ongoing developmental growth.