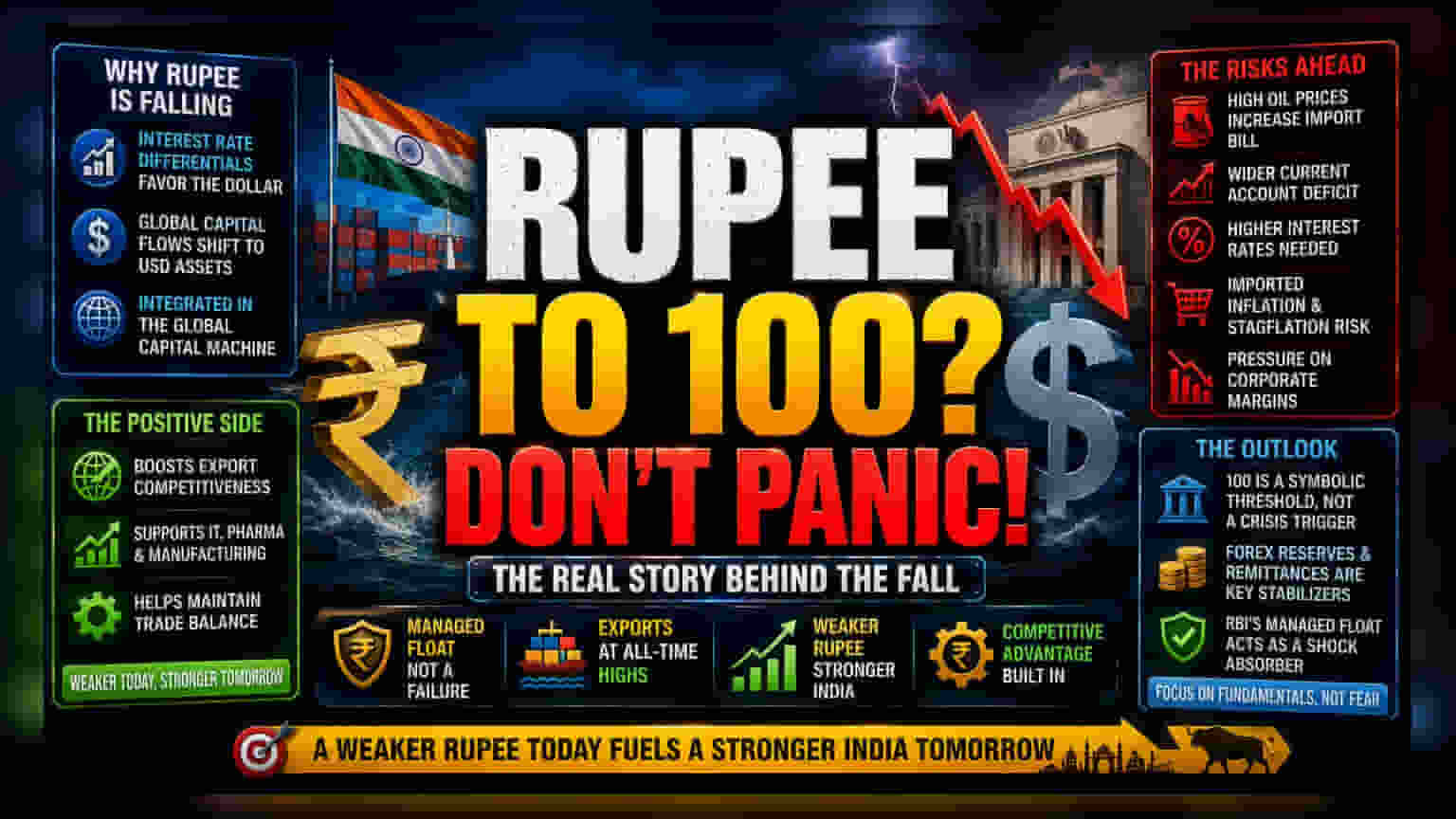

The Valuation Mirage

The obsession with the 100-rupee handle is a classic case of anchor bias. In currency markets, nominal levels are secondary to real effective exchange rate (REER) stability and trade competitiveness. The current slide is not a sudden decoupling of the Indian economy but a calculated reflection of interest rate differentials between the Federal Reserve and the Reserve Bank of India. When the dollar maintains a higher yield profile, capital flows naturally gravitate toward USD-denominated assets, putting persistent pressure on the rupee. This is not a failure of domestic policy, but a reflection of India’s integration into the global capital machine.

Competitive Advantage and the Export Engine

Unlike economies that rely on artificially propping up their currency to stave off inflation, the Indian approach—a managed float—prioritizes long-term export viability. By allowing the rupee to depreciate in line with inflation differentials, the RBI effectively subsidizes the nation's manufacturing and service sectors. With FY2026 export figures reaching historical highs, the narrative that a weaker currency signals weakness is demonstrably false. Sectors like IT services and high-value pharmaceuticals rely on this margin-friendly environment to maintain global competitiveness against regional peers like Vietnam or Thailand, which often engage in more aggressive competitive devaluations.

The Forensic Bear Case

While the macro outlook remains constructive, risks reside in the cost of capital and imported inflation. If the rupee’s decline accelerates beyond a controlled slope—often cited by economists as the 4-6% annual band—it forces the RBI into a corner. Should global oil prices remain elevated due to the ongoing West Asia volatility, the import bill for India’s energy requirements will balloon. This creates a feedback loop: higher energy costs translate into a wider current account deficit, which in turn demands higher interest rates to attract foreign portfolio investment. The structural risk here is 'imported stagflation,' where domestic consumer demand is stifled by high borrowing costs necessary to defend the currency, even if that defense is only partial. Furthermore, historical data shows that persistent currency weakness can erode the pricing power of local firms that rely on imported raw materials, creating a squeeze on corporate operating margins that hasn't yet fully manifested in earnings reports.

The Future Outlook

Institutional analysts increasingly view the 100-rupee milestone as a symbolic threshold rather than a catalyst for capital flight. The primary focus for the remainder of the fiscal year will be the stability of foreign exchange reserves and the success of inward remittance flows. As long as the RBI maintains its liquidity management framework, the rupee will likely continue its managed descent, functioning as a shock absorber rather than a source of systemic stress. Investors should monitor the gap between domestic manufacturing growth and the rising costs of energy imports to gauge the true health of the nation's trade position.