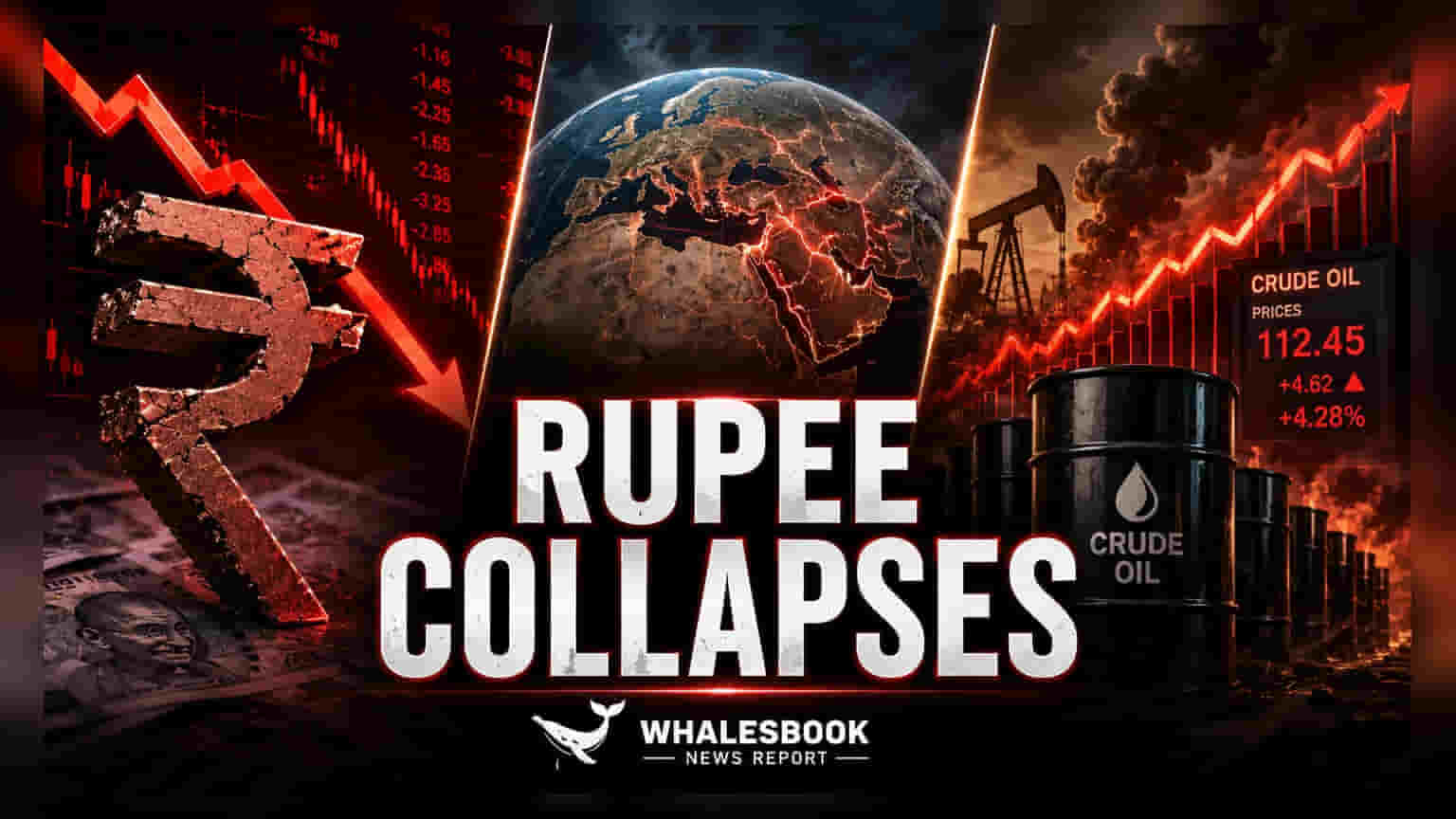

The Valuation Gap and Capital Flight

The recent slide in the rupee represents more than just knee-jerk geopolitical anxiety. While the headlines focus on regional tensions, the structural reality is a widening trade deficit exacerbated by the surge in Brent crude. As a major oil importer, India faces a direct drain on dollar reserves when energy prices escalate, creating a self-reinforcing depreciation loop. This pressure is compounded by the aggressive retreat of foreign institutional investors, who offloaded over Rs 3,900 crore in a single session, signaling a broader re-allocation of capital away from emerging markets toward safer havens as the US dollar index maintains its firm grip near 99.

Assessing the Macro Divergence

Historically, the Indian currency exhibits high sensitivity to the Brent-to-Rupee correlation, yet this week’s action suggests a deeper fracture in market confidence. Unlike periods of past volatility where domestic industrial resilience provided a floor, the current equity market liquidation—marked by significant declines in both the Sensex and Nifty—suggests that investors are prioritizing liquidity over fundamental growth. While GST collections and industrial output data remain relatively robust, the market is currently ignoring these lagging indicators in favor of immediate hedging against dollar-denominated import costs. This disconnect between domestic fiscal health and currency valuation creates a potential entry point for contrarian players, provided the Reserve Bank of India adopts a hawkish stance to curb volatility in the upcoming June meeting.

The Forensic Bear Case

The primary risk for the rupee remains the dual threat of imported inflation and aggressive central bank intervention exhaustion. Should the Reserve Bank of India fail to provide a definitive signal regarding its interest rate trajectory, the currency risks testing the lower bound of the 95.30 resistance level. Critics argue that the central bank’s recent attempts to manage volatility have primarily drained forex reserves without providing a lasting buffer against global sentiment. Furthermore, the persistent selling by foreign institutional investors suggests a lack of confidence in near-term equity valuations, which typically precedes a wider sell-off. If the geopolitical situation continues to disrupt supply chains, the resulting inflationary pressure may force the monetary policy committee to choose between supporting the currency through rate hikes or protecting domestic industrial growth, a classic dilemma that often leads to policy paralysis and further currency devaluation.

The Future Outlook

Analysts are now monitoring the 95.30 level as the critical pivot point for the USDINR pair. With the monetary policy decision slated for June 5, volatility is expected to remain elevated. Consensus among institutional desks suggests that until Brent crude stabilizes below the 90-dollar threshold, the rupee will likely maintain a defensive bias, placing the onus on local policymakers to articulate a credible strategy for curbing the current capital outflow.