A trend of mid-term auditor resignations in India is raising concerns about corporate governance. While not every departure signals wrongdoing, investors are advised to treat sudden exits as a potential red flag, requiring deeper scrutiny of financial disclosures and management transparency before making investment decisions.

What Happened

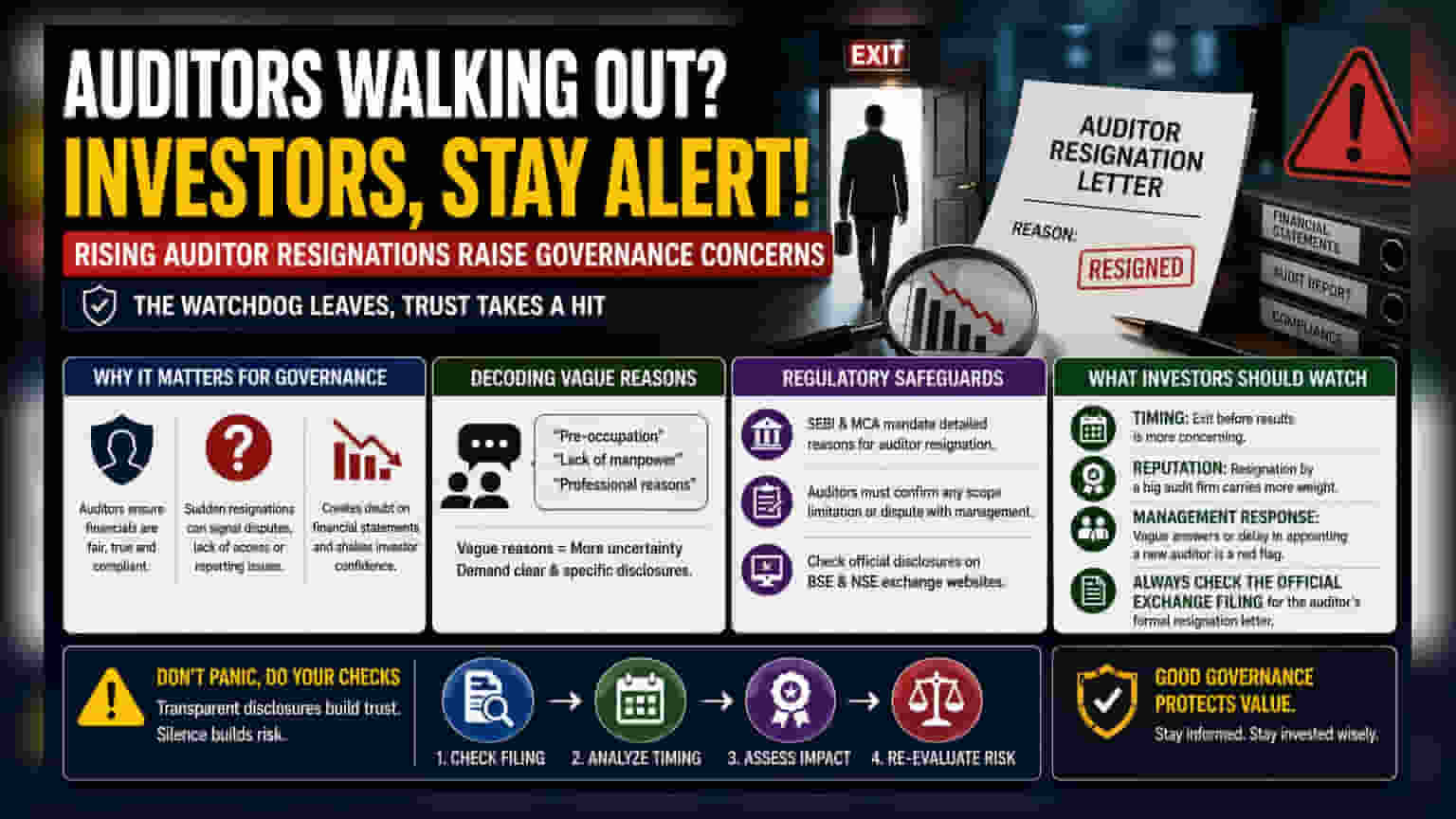

There has been a noticeable increase in auditors resigning from their roles before their term ends across various companies in India. An auditor is the primary watchdog responsible for verifying a company’s financial health and ensuring that accounting standards are followed. When an auditor steps down unexpectedly—especially in the middle of a fiscal year or just before quarterly results are announced—it often creates uncertainty in the market.

While resignation is a professional choice, the timing and the justification provided in company filings are critical details that investors must interpret carefully. This trend has drawn increased attention from regulators and market analysts alike.

Why It Matters For Governance

For investors, an auditor's presence provides a layer of trust. A sudden resignation can signal that the auditor and the company management may have disagreed on how numbers are reported, or that the company was not providing necessary documents or access to information.

When this happens, the market often reacts negatively because it creates doubt about the reliability of the company's past and current financial statements. Governance is about how a company is run, and the auditor is the key person verifying that the rules are being followed. If the watchdog leaves, the trust in those financial figures can drop significantly.

Decoding Vague Reasons

Companies often explain these exits using terms like "pre-occupation," "lack of manpower," or "professional reasons." While these might be genuine in some cases, investors often view these vague explanations with skepticism.

In the financial world, clear communication is essential. If a company does not provide a specific, transparent reason for why their auditor left, it leaves room for speculation. Investors are generally advised to look for detailed disclosures in the exchange filings. If the reason remains unclear even after the filing, it adds to the risk profile of the stock.

Regulatory Safeguards

To address these concerns, regulators like the Securities and Exchange Board of India (SEBI) and the Ministry of Corporate Affairs (MCA) have strengthened rules over the years. Auditors are now required to provide detailed reasons for their resignation to the company and the regulator. If an auditor resigns, they must also confirm whether there was any limitation on the scope of their work or any dispute with the management. Investors can access these official disclosures on exchange websites like BSE and NSE to understand the reality behind the exit.

What Investors Should Watch

Investors should not panic immediately but should perform a basic check when they hear of an auditor resignation.

First, check the timing. An exit right before the announcement of quarterly results is more concerning than one happening at the start of a financial year. Second, look at the reputation of the firm that resigned. A resignation from a large, reputed audit firm often carries more weight than one from a smaller, less-known entity. Third, monitor management's follow-up explanation. If the company fails to appoint a new auditor quickly or provides vague answers, it may be a sign to re-evaluate the investment thesis. Always check the official exchange filing for the auditor's formal letter.