The Reserve Bank of India’s latest Financial Stability Report notes that while banks remain strong, rising loan defaults in the MSME sector and NBFC vulnerabilities require caution. Investors should track how potential global equity market corrections and high household debt might impact domestic financial stability in the coming months.

What Happened

The Reserve Bank of India (RBI) released its latest Financial Stability Report on July 3, 2026, highlighting the current health of the Indian financial ecosystem. While the report describes the banking sector as resilient, it identifies specific areas of concern that could affect the broader economy. The regulator specifically flagged rising loan stress among Micro, Small, and Medium Enterprises (MSME), particularly within the micro-enterprise segment. Industries such as retail trade, tourism, engineering, and agro-products are experiencing higher levels of stressed accounts, which may eventually lead to an increase in Non-Performing Assets (NPAs) for lenders.

The Banking vs. NBFC Divide

According to the report, the banking sector continues to perform well with gross NPAs at 1.8% and healthy capital buffers. However, the report highlights a shift in risk profile for Non-Banking Financial Companies (NBFCs). These lenders are beginning to show a slight weakening in both profitability and liquidity metrics, suggesting that their ability to absorb financial shocks may be narrowing compared to traditional banks. Investors in the financial sector often monitor these metrics to gauge which lenders may face stricter regulatory scrutiny or higher provisioning costs in the future.

Household Debt and Consumption Trends

Another key observation in the report is the rise in household debt, which has reached 45.5% of GDP. The RBI pointed out that a significant portion of this debt is linked to consumption loans rather than asset-creating loans like home or business loans. This trend is important because it suggests that household finances are becoming increasingly sensitive to interest rate changes and employment stability. Relying heavily on consumption-based credit can make the economy more fragile if income growth slows down.

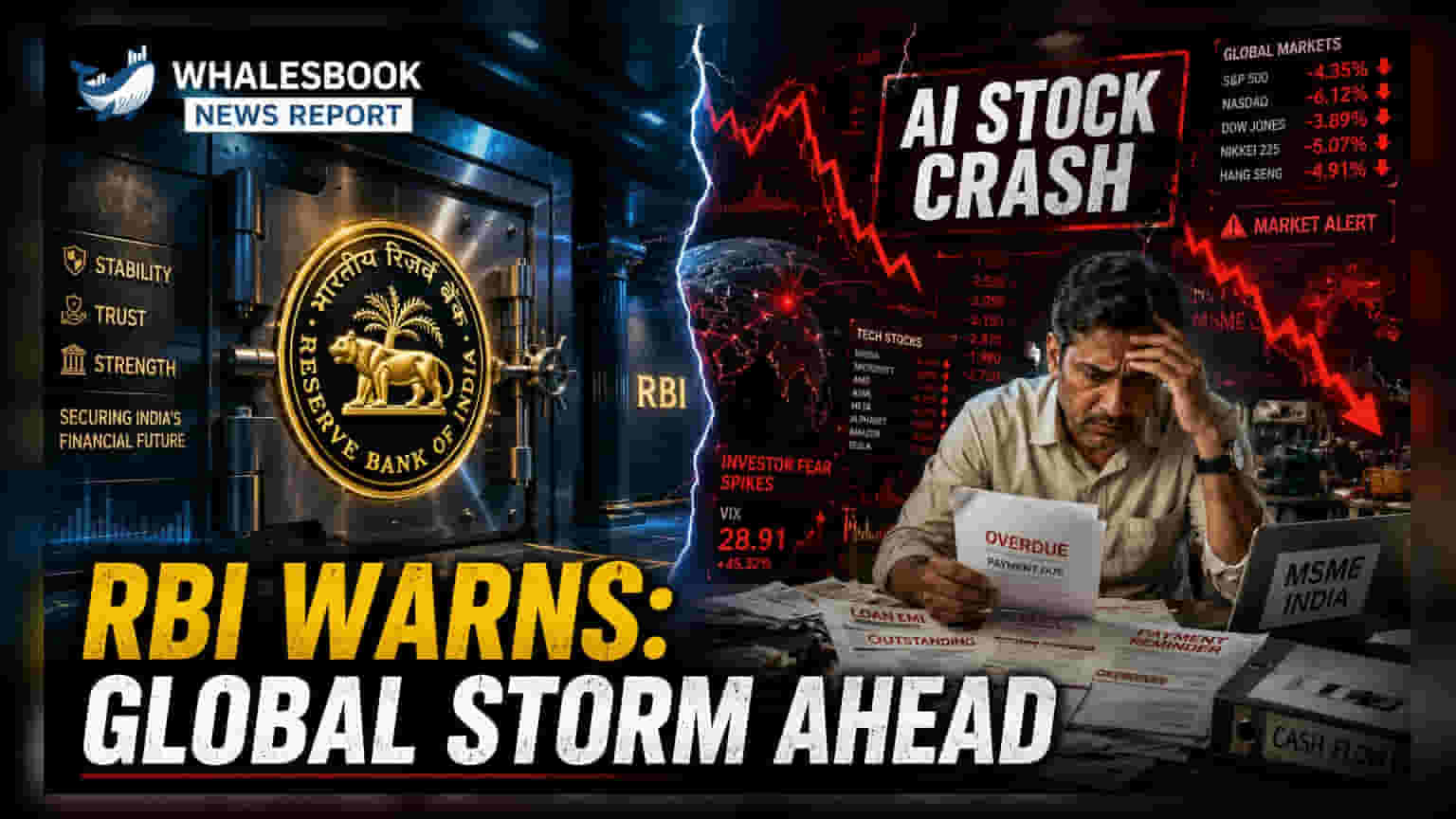

Global Risks and Market Impact

The RBI also cautioned that the Indian financial system remains vulnerable to external shocks. Despite domestic resilience, the report warns of potential volatility in exchange rates due to global supply chain issues and liquidity risks. A major point of concern is the possibility of a sharp correction in global equity markets. If global investors begin to re-evaluate corporate earnings or valuations—particularly in technology and AI-linked stocks—this could lead to negative spillover effects on Indian stock indices.

What Investors Should Track

Investors and market observers may focus on the following monitorables to understand how these risks could evolve:

- Loan quality data from commercial banks and NBFCs, specifically focusing on the MSME book.

- Quarterly commentary from financial institutions regarding provisioning for stressed assets in the retail and engineering segments.

- Data on household debt levels and credit growth rates in subsequent RBI bulletins.

- Movements in global equity markets and their impact on foreign capital flows into India, as identified by the regulator.