The Policy Dilemma

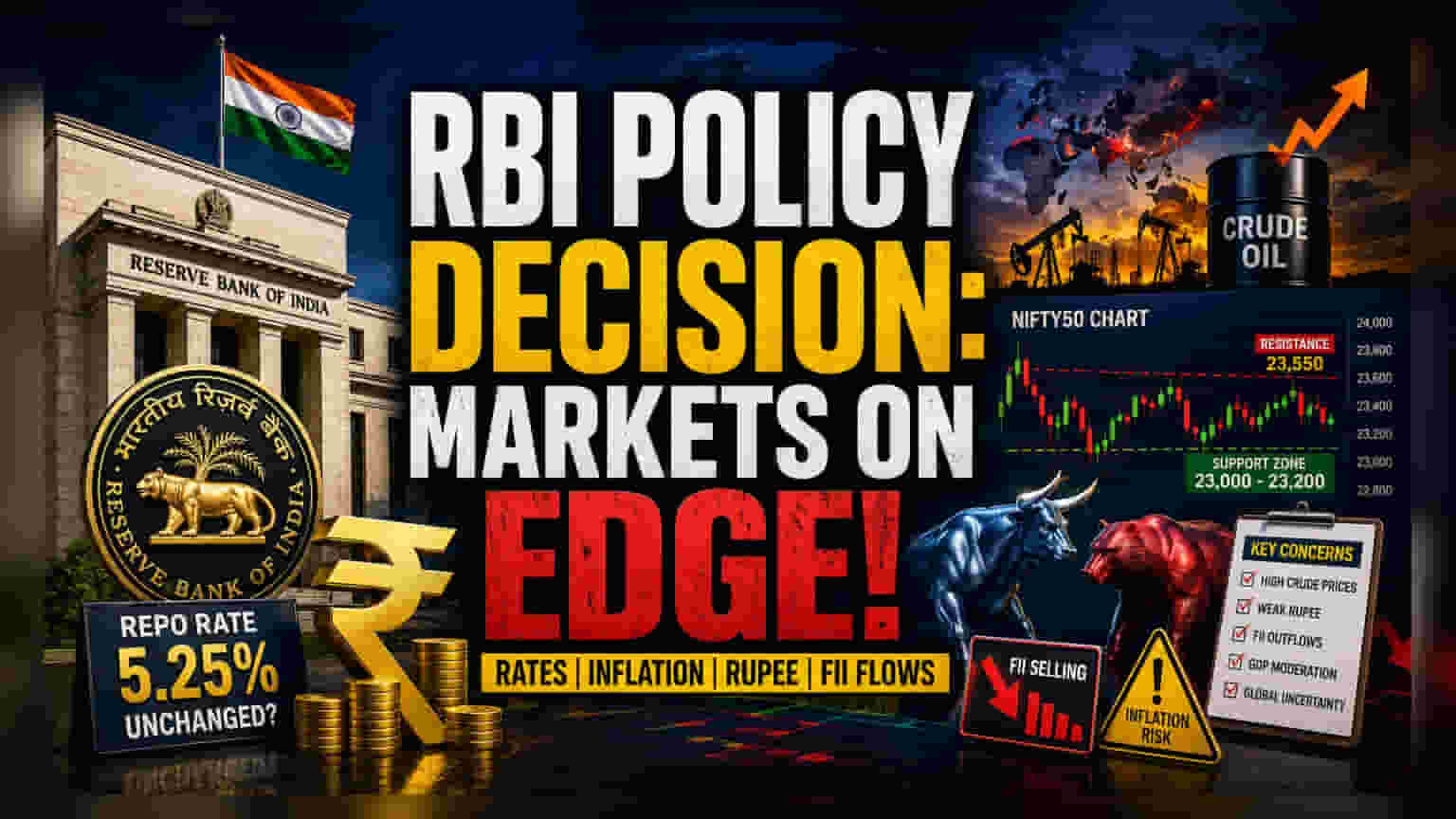

The Indian equity markets are bracing for the Reserve Bank of India’s (RBI) latest monetary policy decision, with the Monetary Policy Committee (MPC) widely expected to maintain the repo rate at 5.25%. While domestic growth remains statistically resilient, the central bank’s leadership is facing a difficult balancing act. Governor Sanjay Malhotra’s commentary will be scrutinized for how the RBI intends to navigate the dual pressures of a weakening rupee—which has faced sustained downward pressure this year—and the imported inflation risks stemming from persistent West Asian geopolitical tensions.

The Volatility Anchor

Market sentiment continues to be tethered to the volatility of global energy markets. With India importing over 85% of its crude oil requirements, the current price environment—where Brent and WTI futures remain elevated—directly impacts the country's fiscal management and consumer price index (CPI) trajectory. Recent trading sessions have demonstrated that Nifty50 is particularly sensitive to these energy price fluctuations and the ongoing, relentless selling streak from foreign institutional investors (FIIs), which has acted as a persistent headwind for frontline indices.

The Technical Stagnation

The Nifty50 index has spent the week locked in a defensive consolidation pattern. Technical analysis reveals a confluence of support between 23,000 and 23,200, which aligns with previous structural gaps and Fibonacci retracement levels. While the index has managed to defend these levels, the absence of a decisive breakout above the 23,550 resistance zone suggests that institutional participants are prioritizing capital preservation over aggressive accumulation. The Relative Strength Index (RSI) remains in a muted range, reflecting the current lack of strong directional momentum.

Structural Risks and the Bear Case

A cautious outlook is warranted given the confluence of macroeconomic headwinds. Unlike previous quarters, where domestic consumption provided a reliable buffer, current inflationary pressures are beginning to stress household budgets and corporate margins. Furthermore, the persistent FII exodus, driven by a stronger US dollar and broader emerging market risk aversion, creates a liquidity vacuum that is difficult for domestic retail inflows to fill. Management and regulatory risks are also increasingly centered on the potential for volatility in bond markets and the sustainability of corporate earnings if the higher-for-longer interest rate environment continues to compress operational cash flows. The looming GDP data, which is expected to show moderation, adds another layer of concern for investors anticipating a robust growth trajectory in the remainder of FY27.

Future Outlook

Analysts suggest the central bank is likely to retain a neutral stance, signaling a willingness to remain vigilant without committing to immediate rate cuts. Market participants will prioritize the RBI's updated inflation and growth forecasts, as these will serve as the primary indicators for how India’s monetary policy might shift should geopolitical tensions further disrupt global supply chains. Until a breakout above current resistance levels is confirmed, the market is expected to remain range-bound and highly reactive to external news flow.