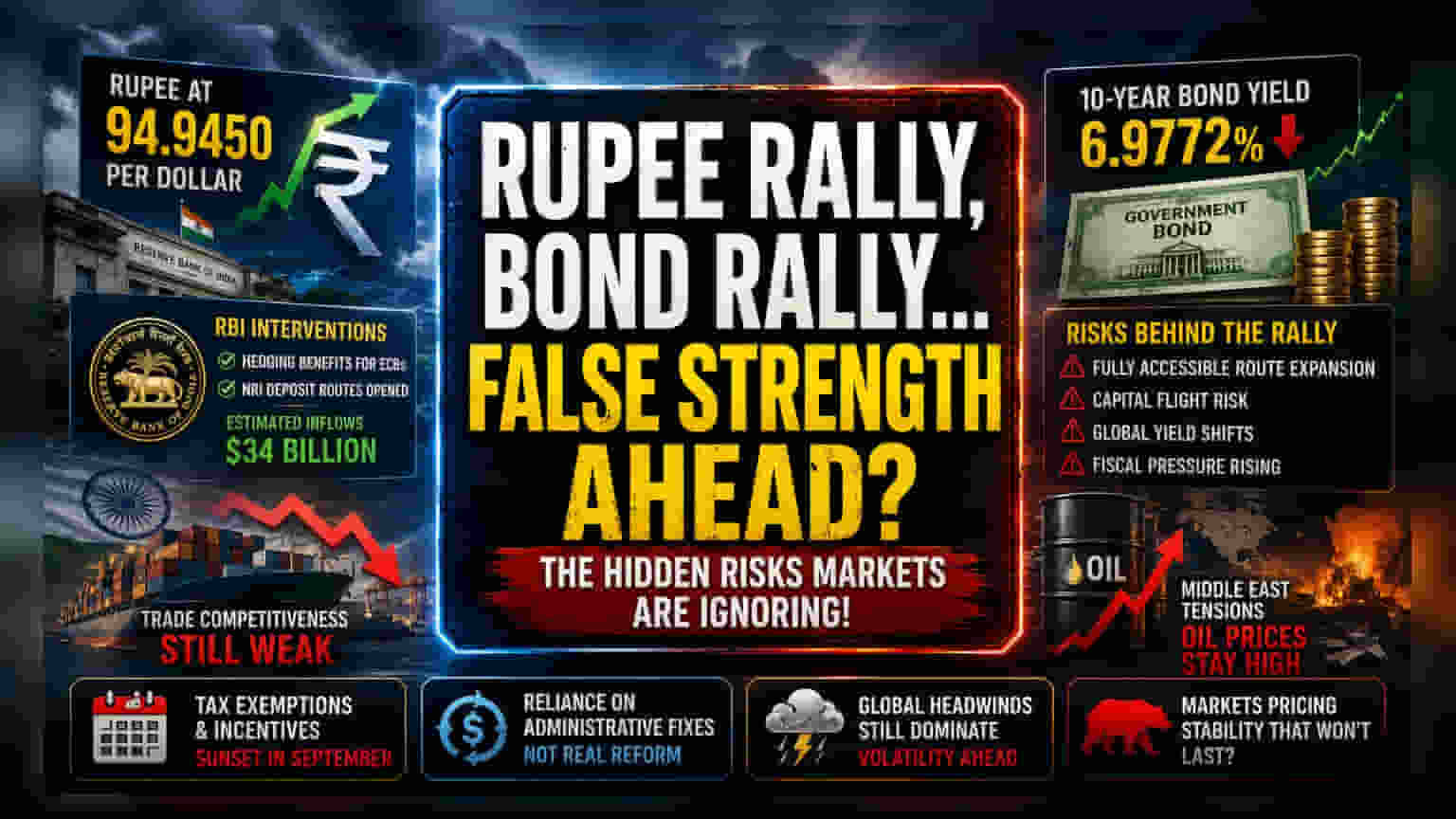

The Liquidity Facade

The recent appreciation of the rupee, which touched 94.9450 per dollar, is less a reflection of structural economic strength and more a direct consequence of the Reserve Bank of India’s managed interventionism. By granting hedging benefits for external commercial borrowings and opening specific deposit routes for Non-Resident Indians, the central bank has essentially engineered an artificial supply of foreign exchange. While these measures are projected to draw significant inflows—with estimates reaching $34 billion—they serve primarily to mitigate the immediate pressure on the current account rather than addressing the core competitiveness of the Indian export sector.

The Bond Market’s Misplaced Optimism

Fixed-income investors have responded to the RBI’s decision to bypass an interest rate hike with enthusiasm, driving the 10-year benchmark yield down to 6.9772%. This rally assumes that the central bank can successfully decouple Indian monetary policy from global trends. However, this optimism ignores the inherent risk of the Fully Accessible Route expansion. By incentivizing foreign participation in long-duration government bonds, India is increasingly susceptible to capital flight if global risk appetite shifts or if real yields in developed markets widen significantly. The move to exempt overseas investors from capital gains tax on these instruments is a desperate attempt to maintain this inflow, yet it complicates the fiscal ledger as the government seeks to balance rising infrastructure expenditure with debt sustainability.

The Structural Weakness

Despite the current euphoria, the underlying macroeconomic reality remains precarious. The stalling of critical geopolitical de-escalation efforts in the Middle East continues to create a floor for crude oil prices, which remains the single most significant threat to India’s trade balance. Unlike historical periods of stability, the current environment is defined by a robust US labor market, which complicates the trajectory for the Federal Reserve. Should the Fed maintain high rates for longer than anticipated, the interest rate differential that the RBI is attempting to manage will erode, forcing the central bank to choose between defending the rupee and curbing domestic inflation.

The Bear Case for Policy Dependence

Reliance on administrative fixes—tax exemptions and artificial hedging facilities—rather than organic economic reform creates a fragile equilibrium. If global oil shocks intensify, the projected $34 billion in inflows may prove insufficient to bridge the widening current account deficit. Furthermore, foreign investors are hyper-aware that these incentives have a sunset clause in September. Any hesitation by the central bank to renew these measures or a sudden shift in global liquidity could lead to a rapid unwinding of long positions, triggering volatility that the current policy framework is ill-equipped to absorb. The market is currently pricing in a duration of stability that is fundamentally at odds with the escalating complexity of global macro headwinds.