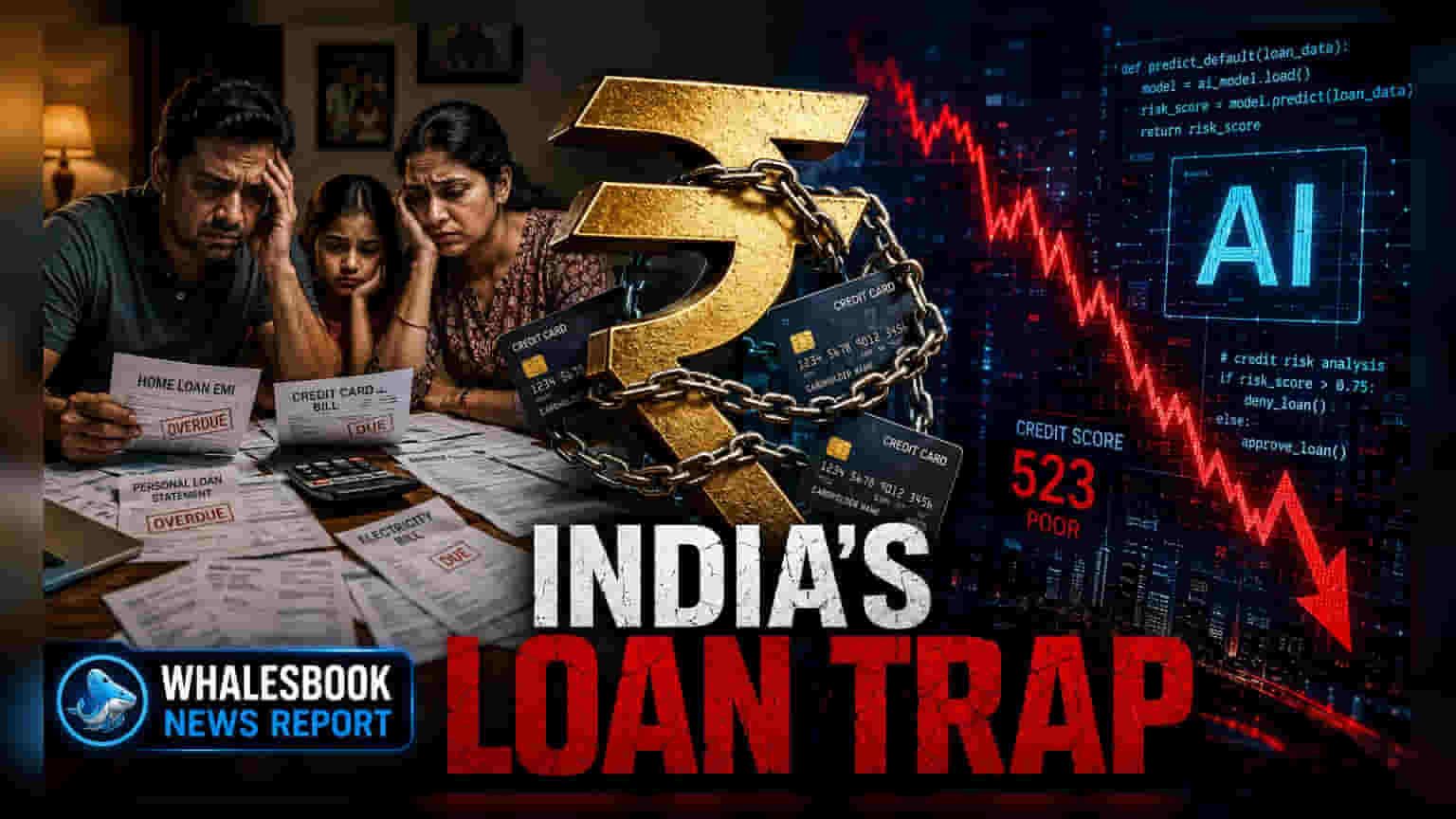

India's household debt has reached 45.5% of GDP, with growth primarily driven by personal consumption loans rather than long-term asset creation. This trend, highlighted in the latest Reserve Bank of India Financial Stability Report, signals potential pressure on consumer finances as wage growth remains modest.

What The RBI Report Says

The Reserve Bank of India’s latest Financial Stability Report has drawn attention to a significant shift in how Indian households are borrowing money. Household debt has risen to 45.5 percent of the country’s total economic output, known as the Gross Domestic Product (GDP). More importantly, the central bank noted that non-housing retail loans—which include personal loans, credit card debt, and vehicle loans—have quadrupled since March 2019. This pace of borrowing is now significantly faster than the growth seen in traditional housing loans.

Why This Matters For Investors

For the broader stock market, this shift in borrowing behavior is a double-edged sword. On one hand, easy access to credit has historically fueled consumer demand, supporting revenue growth for banks, non-banking financial companies (NBFCs), and consumer goods brands. However, when debt is used for daily consumption rather than building assets like homes or businesses, it can lead to financial stress for households over time. If consumers become over-leveraged, their ability to spend on non-essential items could decrease, potentially impacting future profit margins for companies in the retail, auto, and consumer discretionary sectors.

The Wage And Inflation Challenge

Economic data shows that wage growth has been modest, often failing to keep pace with inflation. When household income does not grow as fast as the cost of living, families often rely on credit to maintain their standard of living. This reliance on debt leaves households more vulnerable to economic shocks. Furthermore, the rapid integration of Artificial Intelligence in the workplace has created uncertainty regarding job security, particularly in the technology and services sectors, which may weigh on long-term consumer confidence.

Rural Income And External Risks

Beyond urban credit patterns, the rural economy faces its own set of challenges. Climate factors, specifically the impact of El Nino on monsoon patterns, continue to influence agricultural output and rural income levels. Recent trends show a rise in gold-backed loans, which often serves as a proxy for financial stress, as households turn to pledging assets to manage emergency cash needs. A sustained period of rural income pressure can dampen demand for fast-moving consumer goods (FMCG) and tractors, which are essential parts of the Indian consumer landscape.

What Investors Should Track

Investors may keep a close eye on the asset quality reports from major retail lenders in upcoming quarterly results. Specifically, tracking the delinquency rates—or the percentage of loans that are not being repaid on time—in the personal loan and credit card segments will be vital. Additionally, commentary from consumer-facing companies regarding rural demand and volume growth will provide a clearer picture of whether consumption patterns remain sustainable or if households are nearing their borrowing limits.