For the fiscal year 2025-26, the new income tax regime is the default option and provides significant tax savings for individuals earning between ₹25 lakh and ₹1 crore. While the new system is generally more cost-effective, taxpayers with large deductions should compare both regimes before filing their returns.

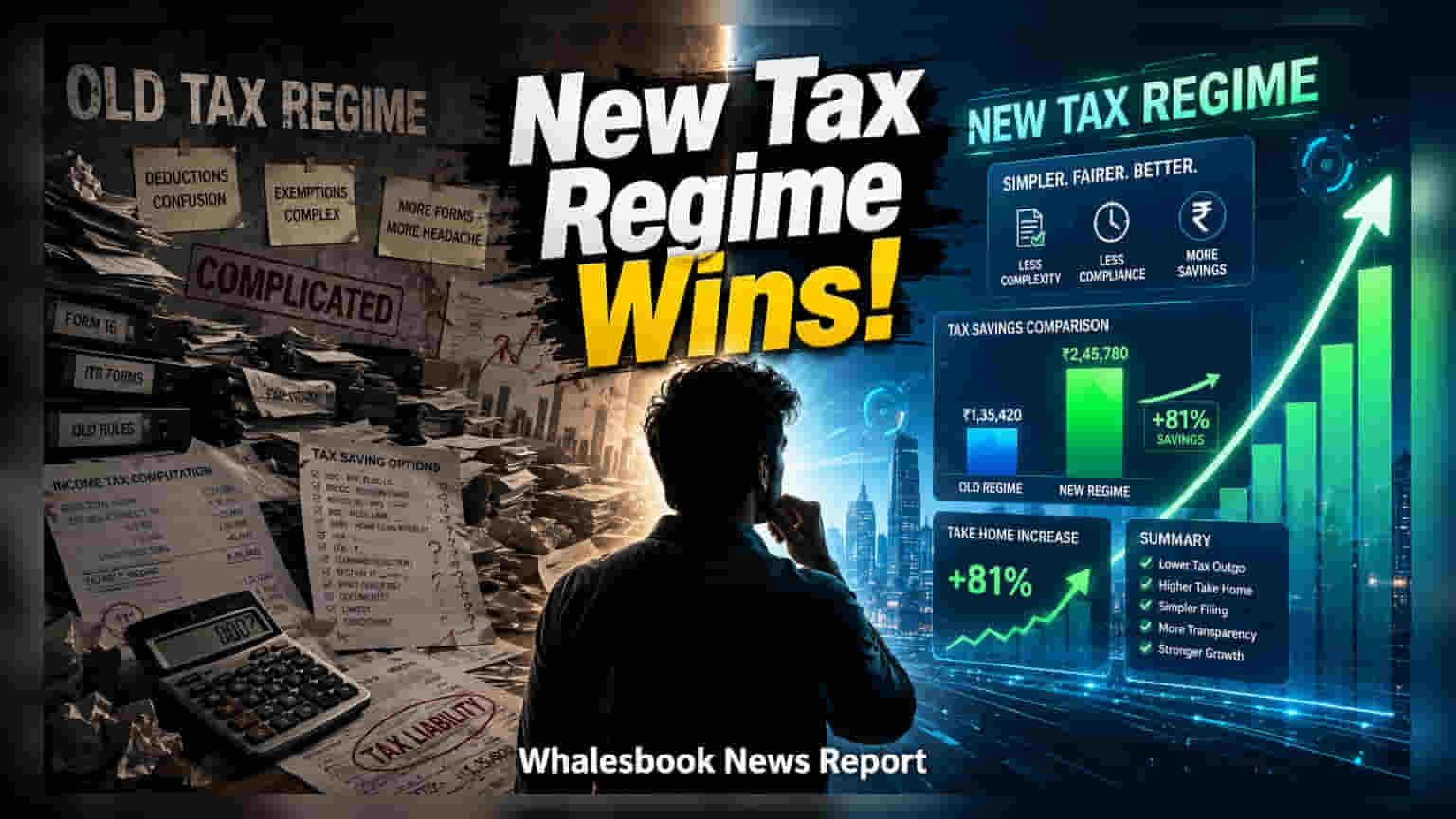

For the fiscal year 2025-26, the new income tax regime stands as the default choice for taxpayers. This system has gained traction for its simplified structure and lower tax rates, which often result in a lower total tax liability compared to the traditional old regime. Recent data indicates that high-income earners, specifically those with annual incomes ranging from ₹25 lakh to ₹1 crore, may see tax savings of approximately ₹1.5 lakh by opting for the new system.

The financial advantage of the new regime is primarily due to its lower slab rates, which outweigh the benefit of most tax-saving deductions available under the old system. When comparing a salaried individual earning ₹25 lakh—who might otherwise claim deductions such as ₹1.5 lakh under Section 80C, ₹25,000 for health insurance under Section 80D, and ₹2 lakh for House Rent Allowance—the new regime can result in a tax saving of over ₹1.3 lakh. This trend persists even as income reaches the ₹1 crore mark, where the impact of the surcharge is mitigated by the lower base tax rates provided by the new regime.

Despite the mathematical edge of the new regime, the old system retains relevance for a specific segment of taxpayers. Individuals who maintain high levels of tax-efficient spending, such as significant home loan interest payments under Section 24(b) or substantial contributions to the National Pension System under Section 80CCD(1B), may still find the old regime more beneficial. Because personal financial situations vary, tax experts emphasize that a direct, personalized comparison remains the most reliable way to determine the optimal choice rather than relying on standard assumptions.

For salaried employees, the selection made at the start of the year for payroll purposes is not permanent. Even if an employer deducts tax based on the new regime, employees can opt for the old regime at the time of filing their Income Tax Return. If the old regime results in a lower tax liability, the difference can be claimed as a refund. However, this flexibility is more restrictive for those with business or professional income. Such individuals must use Form 10-IEA to communicate their choice to the tax department, and they may face limitations on how frequently they can switch between the two regimes. Taxpayers should ensure all relevant income and deduction documents are organized before the final filing date to avoid last-minute errors.