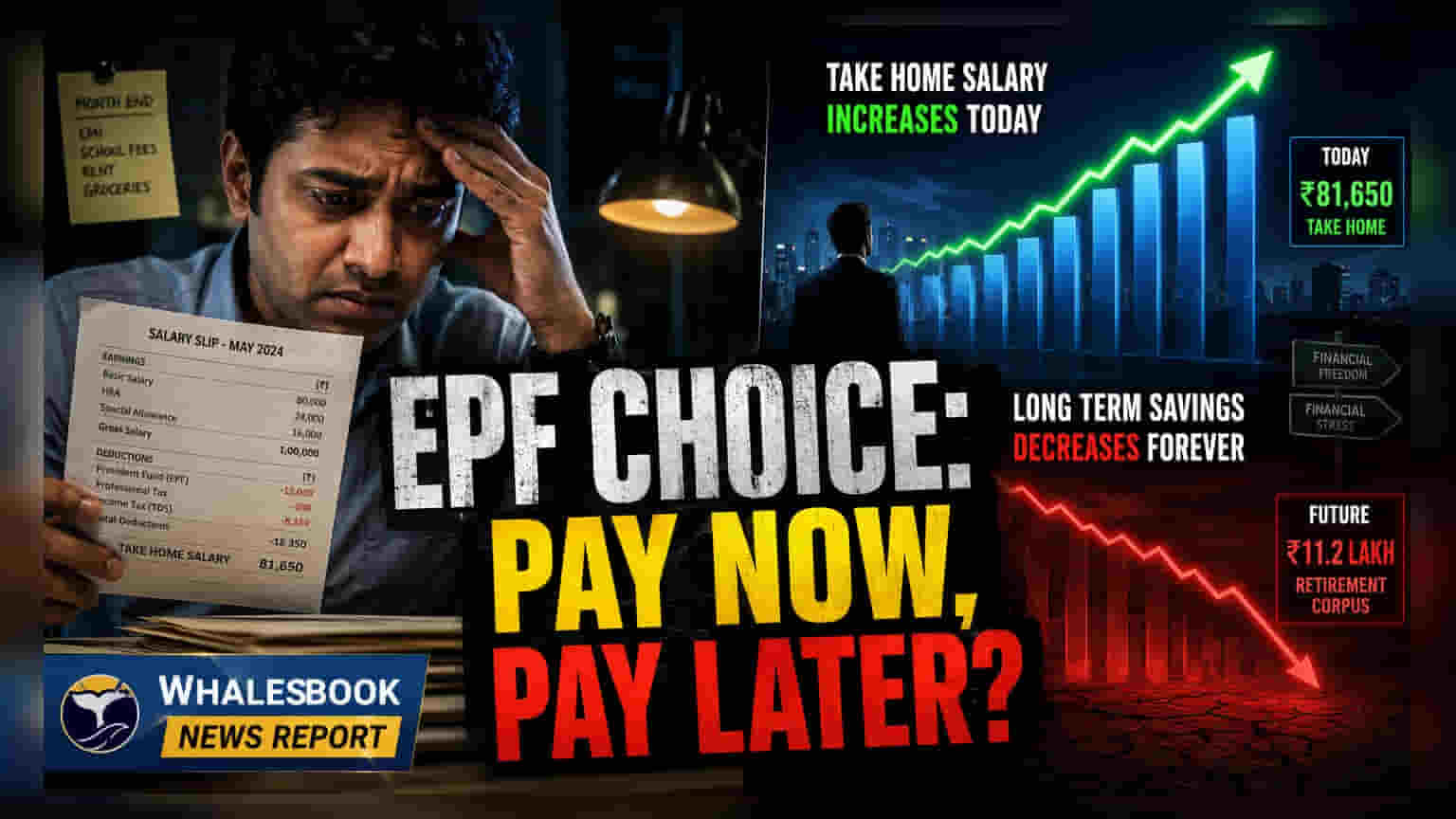

New labor codes may allow employees to reduce EPF contributions above the statutory limit to boost take-home pay. While this increases immediate cash flow, it risks reducing your long-term retirement savings and employer matching benefits.

What Happened

Under upcoming labor code changes, employees may gain the flexibility to lower their Employees' Provident Fund (EPF) contributions on salaries exceeding the statutory wage ceiling of ₹15,000 per month. Previously, while the 12% mandatory contribution was fixed on this ceiling, many employees contributed on their full basic salary by choice. The new framework allows for mutual agreements between employers and employees to restrict contributions to the statutory minimum of ₹1,800. This shift aims to provide immediate relief to those seeking higher monthly disposable income, but it alters a long-standing structure of automatic, long-term wealth creation for the Indian workforce.

The Math of Your Retirement Corpus

The primary impact of reducing your EPF contribution is the loss of compounding over time. EPF currently provides a government-backed interest rate of 8.25% for FY26. For an employee with a ₹50,000 basic salary, reducing a monthly contribution from ₹6,000 to the mandatory ₹1,800 adds ₹4,200 to the monthly paycheque. Over 25 years, that difference, if kept in the EPF, could have grown to over ₹40 lakh. This figure does not account for the additional loss if your employer also decides to reduce or stop their matching 12% contribution, which is only mandatory up to the ₹15,000 wage ceiling.

The Tax and Discipline Factor

Beyond the loss of interest, there is a tax trade-off. The additional take-home pay you receive will be treated as part of your regular salary and becomes subject to income tax according to your slab. Conversely, EPF interest remains tax-free for most subscribers, provided their annual contribution does not exceed ₹2.5 lakh. Furthermore, the EPF acts as a 'forced' savings mechanism. For individuals who struggle with consistent investing, the extra cash is often absorbed by daily expenses, leaving them with significantly less capital by the time they reach retirement.

When Might This Flexibility Make Sense?

Lowering your EPF contribution is generally only considered rational in specific, well-planned financial scenarios. If an individual carries high-interest debt, such as personal loans or credit card balances with interest rates between 12% and 14%, using the extra cash to prepay these loans may provide a better financial outcome than the 8.25% return from the EPF. Additionally, highly disciplined investors who intend to systematically move the extra funds into equity-based investments might seek higher potential growth. However, these moves require a concrete, written investment plan rather than a casual decision based on short-term liquidity needs.

What Investors and Employees Should Track

Before opting for any change, employees must review their company's updated EPF policy. The key monitorable is whether your employer will continue to pay their matching 12% contribution on your full salary if you choose to reduce your own. Without an employer matching that portion, the loss to your total retirement benefit increases significantly. It is essential to calculate the exact impact on your retirement corpus and verify if you have a reliable plan to invest the additional take-home pay before finalizing any reduction.