A new NIPFP report reveals that two-thirds of India's informal businesses struggle to secure formal credit. Manufacturing units, women-led firms, and businesses owned by SC/ST and OBC groups face the most severe barriers. For investors, this data highlights a large, untapped lending opportunity but also points to potential risks in supply chain stability and asset quality for financial institutions.

What Happened

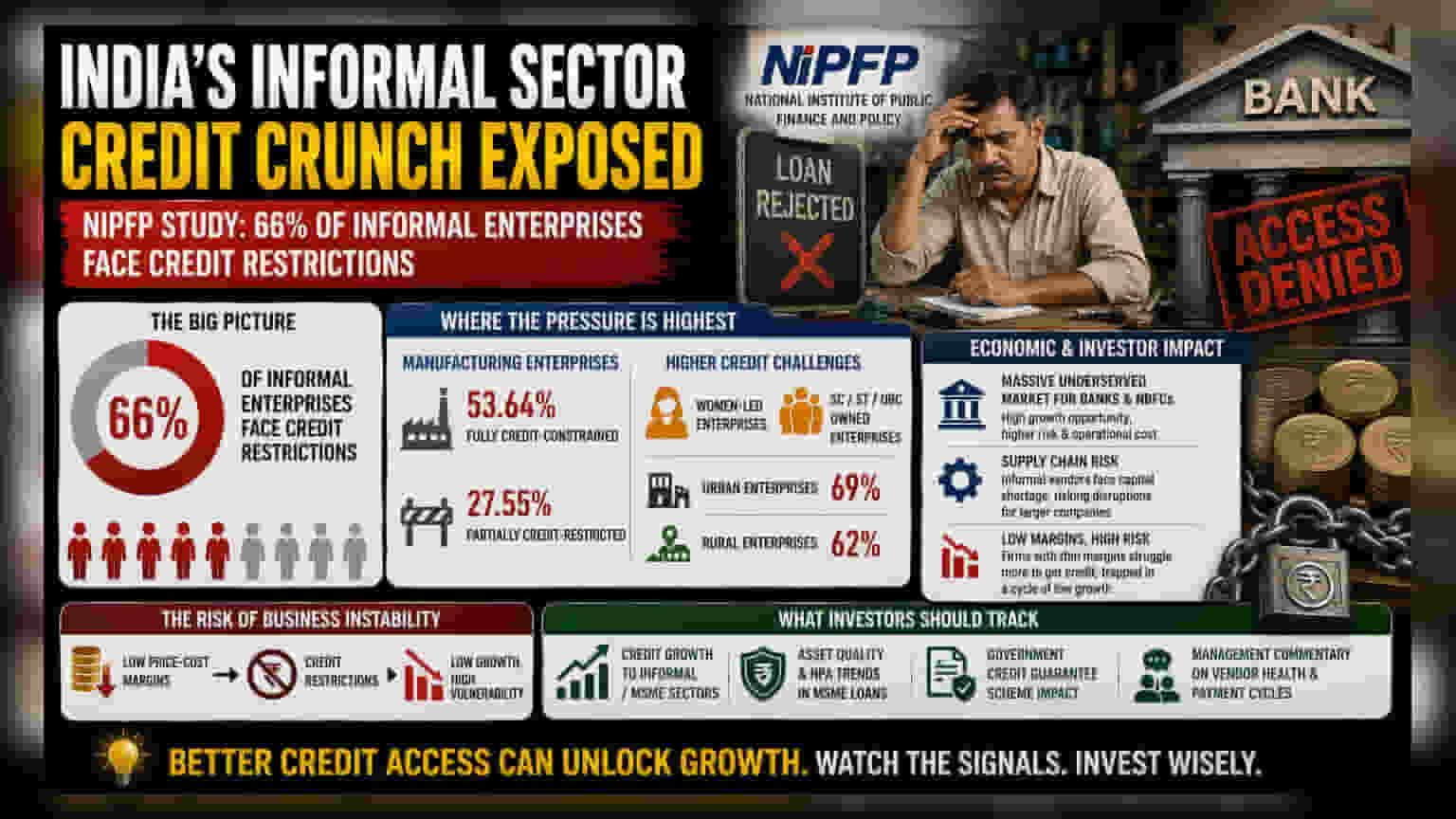

A recent study by the National Institute of Public Finance and Policy (NIPFP) has highlighted a deep-seated issue within India's informal economy: the lack of access to formal credit. The report, which analyzed government data, found that nearly 66% of informal enterprises in India are struggling with some form of credit restriction. This means a vast majority of these businesses cannot secure the capital needed for operations or growth through regular banking channels, forcing them to rely on less reliable or more expensive sources of funding.

Where The Pressure Is Highest

The study identified specific groups that find it hardest to access finance. Manufacturing enterprises are among the most severely impacted, with approximately 53.64% categorized as fully credit-constrained and another 27.55% facing partial restrictions. This is significant because manufacturing often requires upfront capital for raw materials and equipment, unlike some service-based businesses that might operate on lower cash requirements.

Furthermore, the research showed that credit access is not equal across demographics. Women-led enterprises and businesses owned by entrepreneurs from Scheduled Caste (SC), Scheduled Tribe (ST), and Other Backward Classes (OBC) face a higher probability of being fully or partially credit-constrained. Additionally, urban enterprises are reporting greater difficulties (69% facing constraints) compared to their rural counterparts (62%).

The Economic And Investor Impact

This credit crunch carries meaningful implications for Indian investors. For the banking and non-banking financial company (NBFC) sectors, this data highlights a massive, underserved market. Lenders that can effectively assess and manage the risk of these small, informal borrowers could unlock significant growth. However, this comes with the challenge of higher operational costs and the need for better technology to underwrite loans for businesses that may lack formal financial records or collateral.

For investors in large manufacturing and FMCG companies, the health of the informal sector is a direct supply chain monitorable. Many large corporations rely on informal, smaller vendors for distribution or component manufacturing. If these smaller entities face persistent capital shortages, it creates a risk of supply chain disruptions, operational delays, or lower quality output, which can eventually impact the margins and reliability of larger listed companies.

The Risk Of Business Instability

The study suggests a direct link between profitability and credit access. Firms with lower price-cost margins—essentially those with less buffer in their profit margins—are more likely to be credit-constrained. This creates a cycle where businesses with tight margins cannot get the capital to modernize or expand, which keeps their margins low, making them even less attractive to traditional lenders. This structural barrier makes these firms particularly vulnerable to economic slowdowns, rising raw material costs, or sudden changes in demand.

What Investors Should Track

Investors may look closely at how financial institutions adjust their MSME (Micro, Small, and Medium Enterprises) lending strategies. Key indicators include the growth rate of credit to informal sectors, the non-performing asset (NPA) quality within these loan books, and the success of government-backed credit guarantee schemes designed to reduce the risk for lenders. Additionally, management commentary from listed manufacturing firms regarding vendor payment cycles and supplier health may provide a clearer picture of how this credit gap is affecting the ground-level operations of their ecosystems.