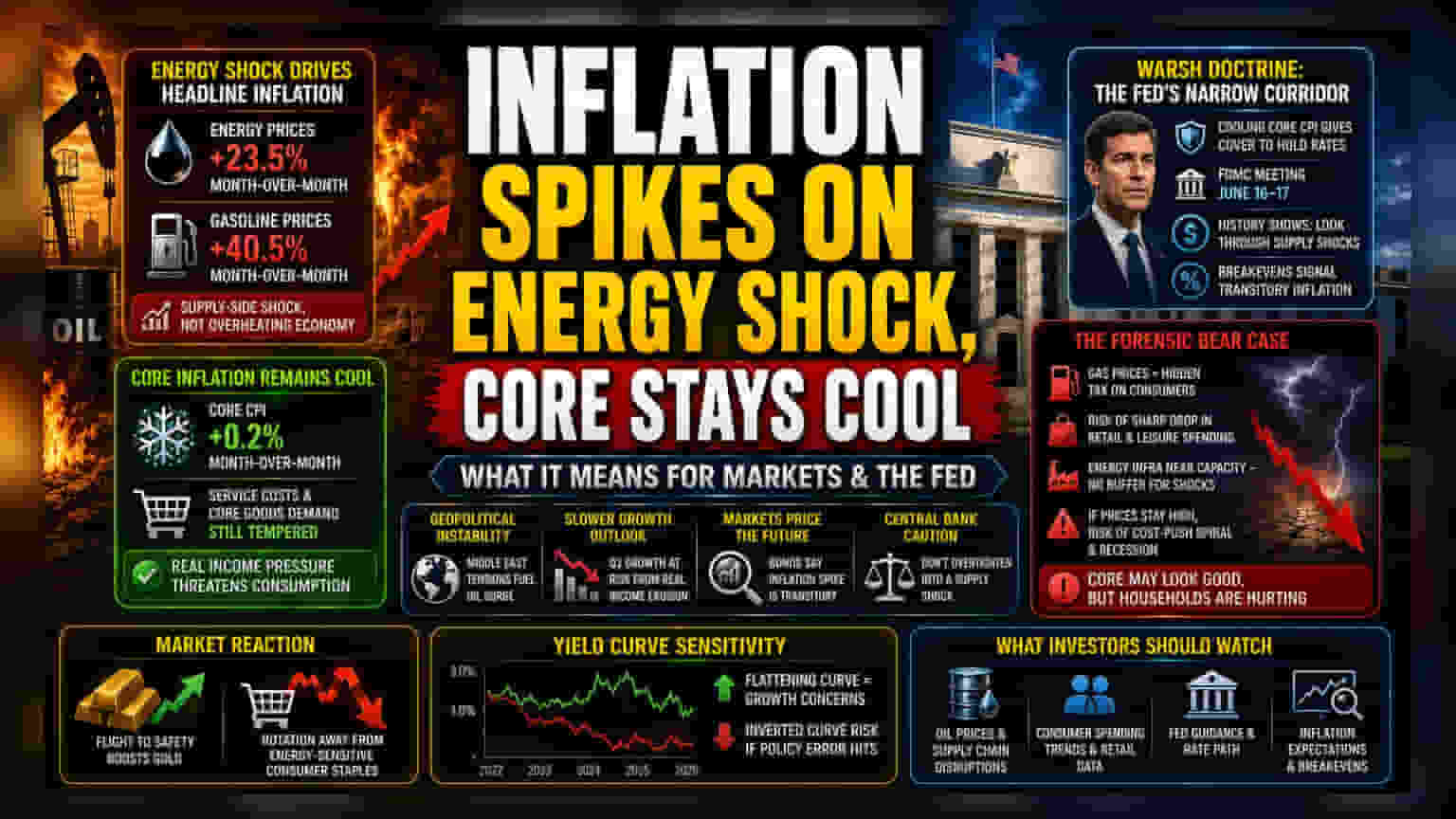

US headline inflation reached 4.2% in May, fueled by a 23.5% spike in energy costs tied to the Iran conflict. While the headline figure stings, the cooling core CPI suggests price pressures are contained, complicating the Federal Reserve's path ahead of next week's policy meeting.

The Divergence Between Energy and Underlying Demand

The headline inflation acceleration reflects a supply-side shock rather than an overheating domestic economy. By stripping away the volatile 23.5% energy spike, the core consumer price index indicates that service costs and core goods demand remain relatively tempered. This divergence highlights a critical distinction for market participants: the surge in living costs is driven by geopolitical instability in the Middle East rather than a fundamental breakout in domestic wage-price spirals. Market participants are now pricing in a broader economic slowdown, as the real income erosion caused by higher fuel prices threatens to curb discretionary consumption in the third quarter.

The Warsh Doctrine and Monetary Policy Shifts

With the upcoming FOMC gathering on June 16-17, Chair Kevin Warsh faces a narrow corridor. The cooling core CPI print—which landed at a softer 0.2% month-over-month—provides just enough cover for the committee to maintain the current federal funds rate. Historical data from similar supply-side shocks, such as the 1973 or 1990 oil price escalations, suggest that central banks typically look through temporary energy spikes unless they show signs of feeding into long-term inflation expectations. Current breakeven inflation rates in the bond market indicate that investors still believe this is a transitory, albeit painful, geopolitical anomaly rather than a structural change in the price environment.

The Forensic Bear Case: Structural Risks

While current figures suggest stability, the structural risk remains significant. The 40.5% jump in gasoline prices acts as a de facto tax on the consumer, potentially triggering a sharp contraction in retail and leisure spending if the Iran-related supply chain disruptions persist through the summer. Unlike previous cycles where the Fed could rely on energy abundance, the current domestic energy infrastructure operates near capacity, leaving little buffer to absorb further geopolitical shocks. If these energy costs remain elevated through the fourth quarter, the risk of a cost-push inflationary spiral increases, forcing the Federal Reserve into a restrictive stance that could inadvertently trigger a recession. Critics argue that relying on core inflation as a gauge of success masks the genuine financial distress currently felt by households facing historic utility and transport costs.

Future Trajectories and Yield Curve Sensitivity

The market response has been characterized by a flight to safety in gold and a rotation away from energy-sensitive consumer staples. Forward-looking guidance from various financial institutions suggests that if energy prices fail to retreat by late summer, the focus will shift from headline inflation to potential long-term growth degradation. Investors should monitor the two-year and ten-year Treasury yield spread closely; a continued flattening could serve as a leading indicator that the bond market is anticipating a policy error if the Fed keeps rates too high while supply-side shocks erode economic output.