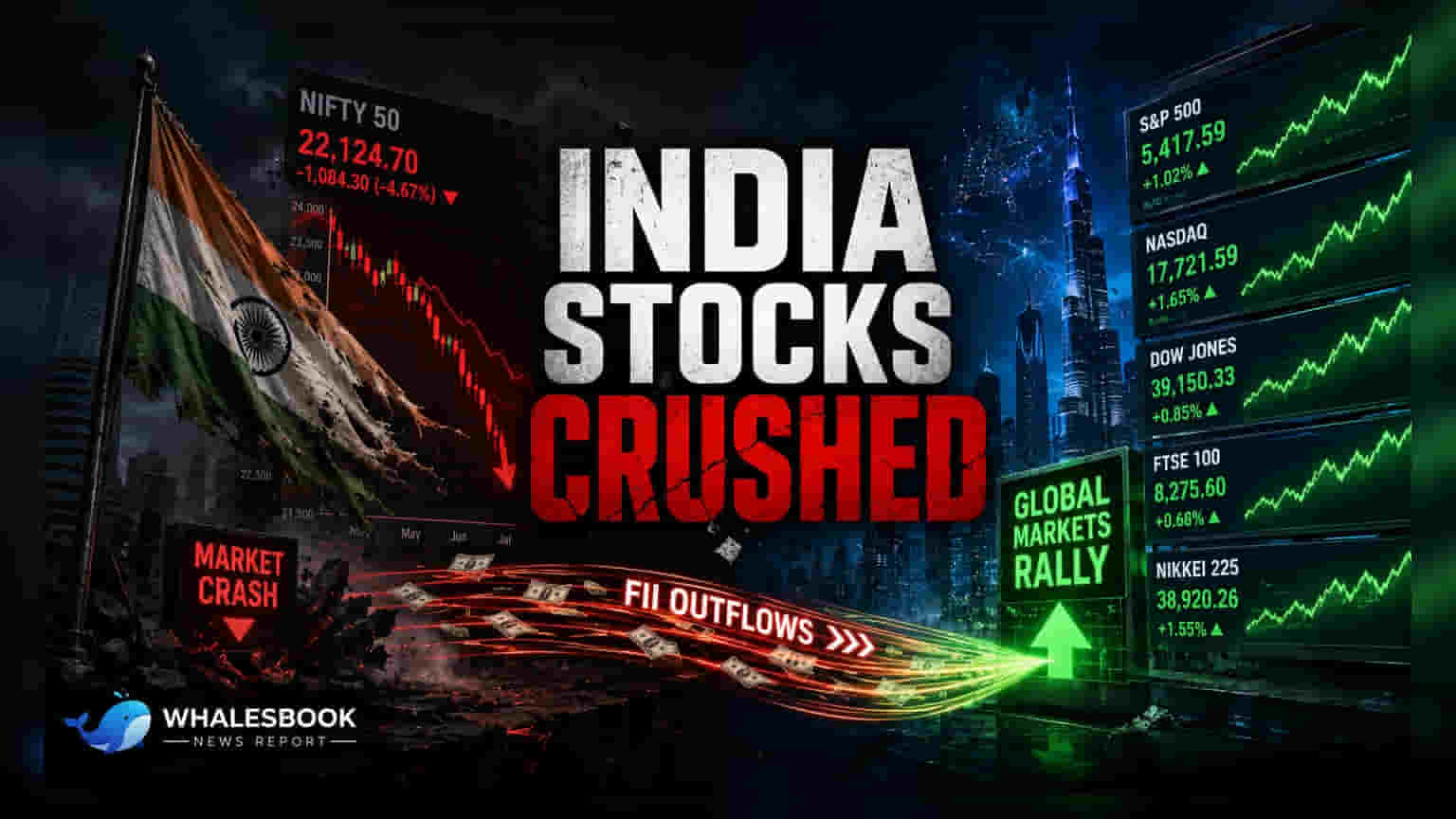

The MSCI India Index has fallen 13% in 2026 as foreign investors pulled out $29 billion, making India a global laggard. While domestic investors have invested over $50 billion, they could not fully offset this selling pressure. Despite the market correction, India's GDP growth remains strong at 7.7%, and stock valuations have become more reasonable compared to historical averages.

Indian stock markets have faced a difficult year in 2026, significantly trailing behind other global markets. While global indices have seen strong gains, often driven by the worldwide boom in artificial intelligence and semiconductors, the MSCI India Index has recorded a decline of 13% in dollar terms. This underperformance marks a shift from previous years, as investors have moved capital toward other emerging markets that currently offer more attractive valuations.

Foreign Selling and Domestic Response

The primary reason for the market pressure is a sustained exit of foreign institutional investors. Since the start of 2026, foreign investors have sold approximately $29 billion worth of Indian equities. This trend has been driven by several factors, including the high stock valuations seen at the beginning of the year, a slowdown in corporate earnings growth, and concerns regarding global trade policies and geopolitical tensions in West Asia. In response, domestic institutional investors have acted as a buffer, injecting more than $50 billion into the market. However, this domestic support has not been enough to fully counteract the scale of foreign selling, leaving the Nifty 50 down 8.7% year-to-date.

Valuation and Sector Trends

Recent market movements have brought valuations down to more reasonable levels. The Nifty 50 index currently trades at 18.8 times one-year forward earnings, which is lower than its long-term average of 21 times. This suggests that the valuation premium that existed earlier has largely moderated. Nearly two-thirds of sectors are now trading below their historical average valuations. Specifically, sectors like private banks, consumer goods, technology, and retail are currently available at a discount compared to their historical norms. Conversely, areas such as capital goods, public sector banks, metals, healthcare, and utilities continue to trade at a premium.

Economic Performance and Future Outlook

Despite the decline in share prices, India’s underlying economy remains resilient. GDP grew by 7.7% in the 2026 fiscal year, beating earlier projections. Corporate profitability has also reached record levels, with the profit-to-GDP ratio for Nifty 500 companies hitting a peak of 5.2%. Sectors like automobiles, oil & gas, metals, and insurance have been major contributors to this strong profit performance.

Looking ahead, analysts suggest that future market returns will be less about the performance of the broad index and more about the growth of individual companies. Key factors that could support a market recovery include a potential return of foreign capital if global interest rates fall, sustained GDP growth above 7%, and continued government spending on infrastructure. Investors will likely monitor the trajectory of foreign inflows and corporate earnings growth, which will be critical in determining whether the market can recover from its current slump.