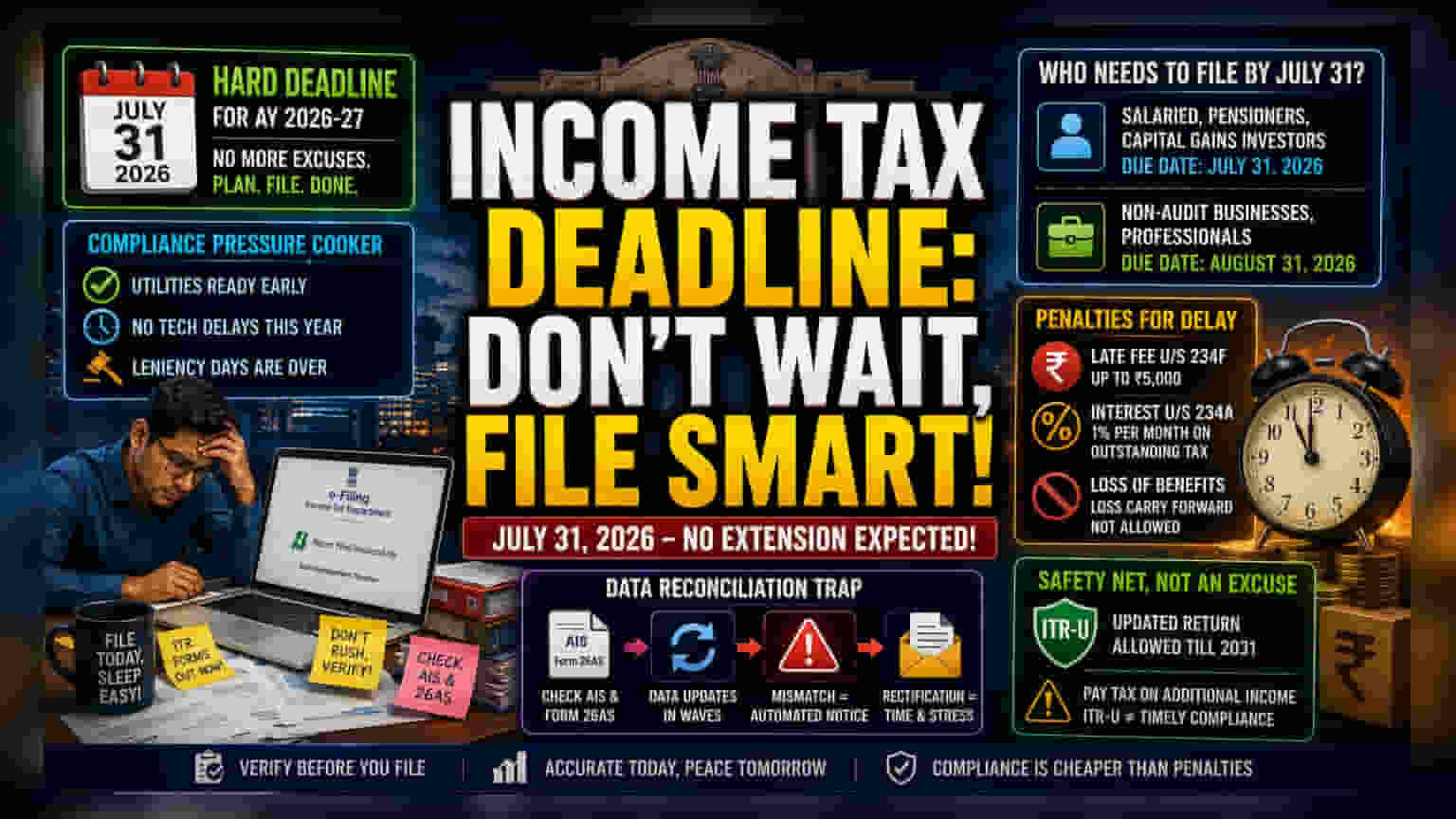

The Compliance Pressure Cooker

The Income Tax Department has signaled a firm stance on the July 31, 2026, deadline for Assessment Year 2026-27, marking a departure from the administrative leniency seen in prior cycles. By ensuring that major filing utilities were accessible well ahead of the summer months, the tax authorities have effectively stripped away the common justification for previous extensions: the delayed availability of digital infrastructure. For the average taxpayer, this creates a concentrated window of compliance activity that prioritizes immediate submission over the cautious wait-and-see approach that often precedes data finalization.

The Data Reconciliation Trap

Modern income tax filings are no longer a simple exercise of reporting salary and interest. The AY 2026-27 forms demand granular disclosures regarding capital gains, losses from share buybacks, and intricate financial transactions. This complexity is where the strategy of early filing clashes with the reality of data integrity. Taxpayers frequently rely on the Annual Information Statement (AIS) and Form 26AS to confirm their financial footprint. Because these systems often update in waves throughout June and July, rushing to submit a return in early June risks creating a mismatch between self-declared income and third-party reporting. Such discrepancies are primary triggers for automated notices from the Central Processing Center, which can turn a straightforward filing into a multi-month rectification ordeal.

Structural Hurdles for Non-Audit Filers

While salaried individuals and pensioners face the July 31 cliff, the broader ecosystem of non-audit business and professional taxpayers remains constrained by an August 31 cut-off. This tiered structure creates a staggered demand on tax professionals, often leading to a bottleneck in technical support and advisory availability. Unlike large corporate entities that manage audits through October or November, individual filers are currently navigating an environment where the burden of proof for complex capital transactions rests entirely on the taxpayer’s ability to interpret fluctuating reporting standards. Those relying on aggressive tax-saving strategies or complex asset liquidations are particularly vulnerable to the current, stricter regulatory oversight regarding stock market activity.

Risks of Delayed Compliance

Adopting a wait-and-see approach for an extension is an increasingly high-stakes gamble. Beyond the base late filing fee under Section 234F, which can reach ₹5,000 for those with taxable income, taxpayers must account for the accumulation of interest under Section 234A. This interest applies to any outstanding tax liability, accruing at a rate of 1% per month from the original due date. Furthermore, failing to file by the July 31 deadline strips the taxpayer of the ability to carry forward certain losses to subsequent assessment years, potentially impacting long-term tax optimization. The availability of the ITR-U, or updated return, until 2031 serves as a safety net for genuine errors, but it is not a substitute for timely compliance and carries its own significant tax costs on additional income reported.