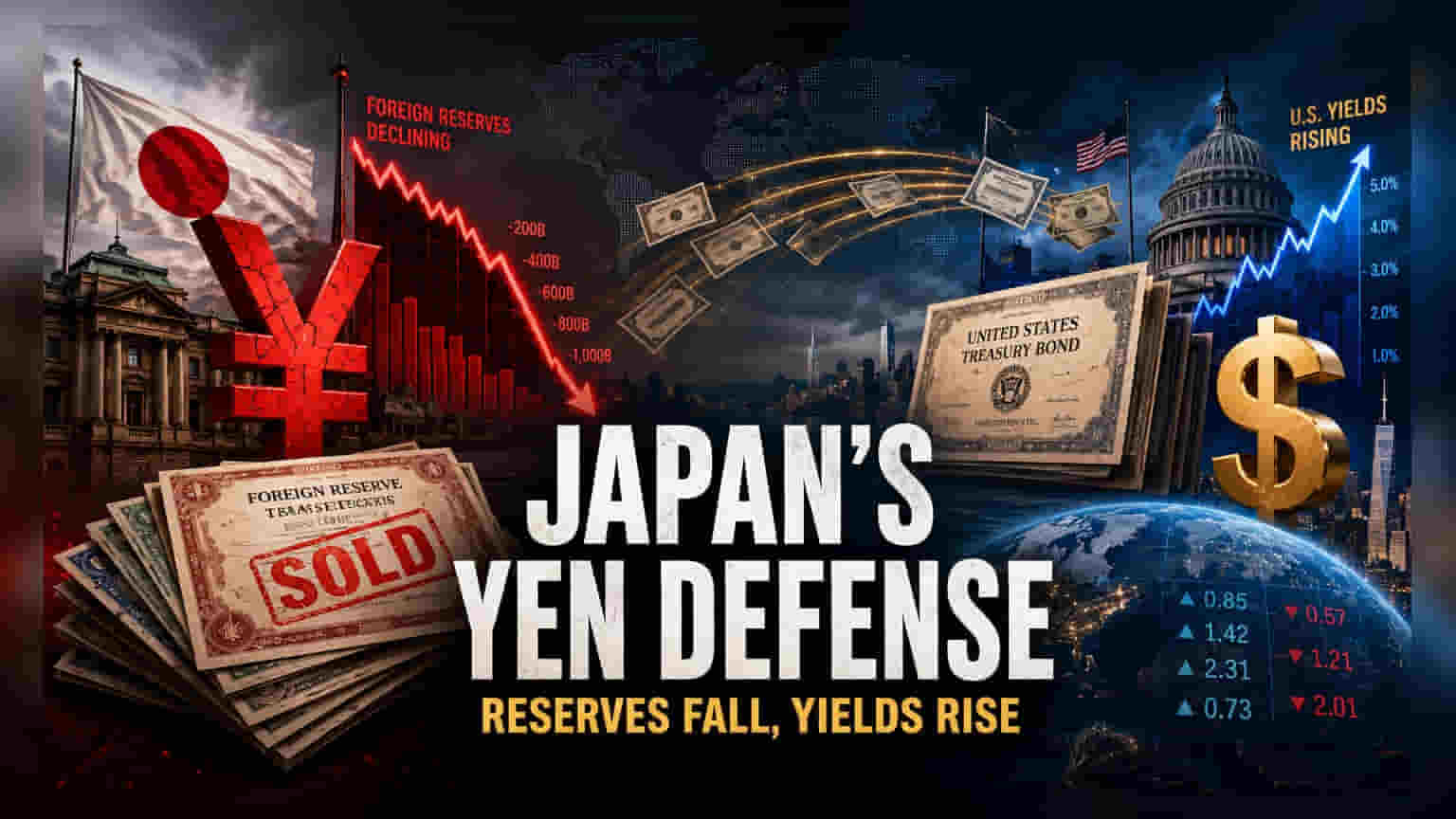

The Mechanism of Currency Defense

The contraction in Japanese foreign reserves stems directly from a tactical deployment of liquidity to counter aggressive yen depreciation. By liquidating $75.6 billion in foreign securities, the Ministry of Finance has effectively prioritized currency stability over the long-term preservation of its dollar-denominated asset portfolio. The timing of this drawdown, which aligns precisely with the record intervention cycle ending May 28, confirms that Tokyo is systematically cannibalizing its investment base to provide a backstop for the yen.

The Bond Market Transmission

While officials often attribute reserve fluctuations to mark-to-market adjustments, the scale of this outflow relative to U.S. Treasury price action during May indicates a deliberate divestment. Historical data from similar interventions suggests that Tokyo favors the liquidation of shorter-dated Treasury bills over longer-duration notes to maintain yield curve integrity. However, the sheer volume of this exit exerts upward pressure on U.S. yields, creating an inverse correlation between Japan's currency defense and American borrowing costs. As the largest foreign holder of U.S. debt, Japan’s decision to reduce exposure forces the market to grapple with a potential shift in the supply-demand equilibrium of global debt securities.

Structural Vulnerabilities and Risks

The primary danger lies in the pro-cyclical nature of this policy. If the yen continues to face selling pressure due to the persistent interest rate differential between the Bank of Japan and the Federal Reserve, Tokyo will inevitably reach a limit on its liquid reserves. Unlike foreign currency deposits, which remained stagnant at $162 billion, U.S. Treasuries represent the only portion of the portfolio deep enough to absorb such massive capital deployments. Any further deterioration in the yen will likely necessitate an escalation in asset sales, which could trigger a disorderly repricing in the bond market. Furthermore, Washington’s heightened sensitivity toward foreign-led volatility creates a regulatory overhang that may complicate future intervention efforts, should U.S. policymakers perceive these actions as detrimental to their own domestic monetary objectives.

Future Trajectory and Policy Outlook

Market participants are currently re-evaluating the terminal capacity of Japan’s interventions. Institutional desks remain split on whether Tokyo can sustain this level of market interference without triggering a broader sell-off in U.S. duration. Should the yen remain anchored near the 160 level against the dollar, the mandate for continued reserve liquidation will likely persist, forcing a re-alignment of global asset allocations and increasing the sensitivity of U.S. Treasury prices to Japanese macroeconomic policy adjustments.