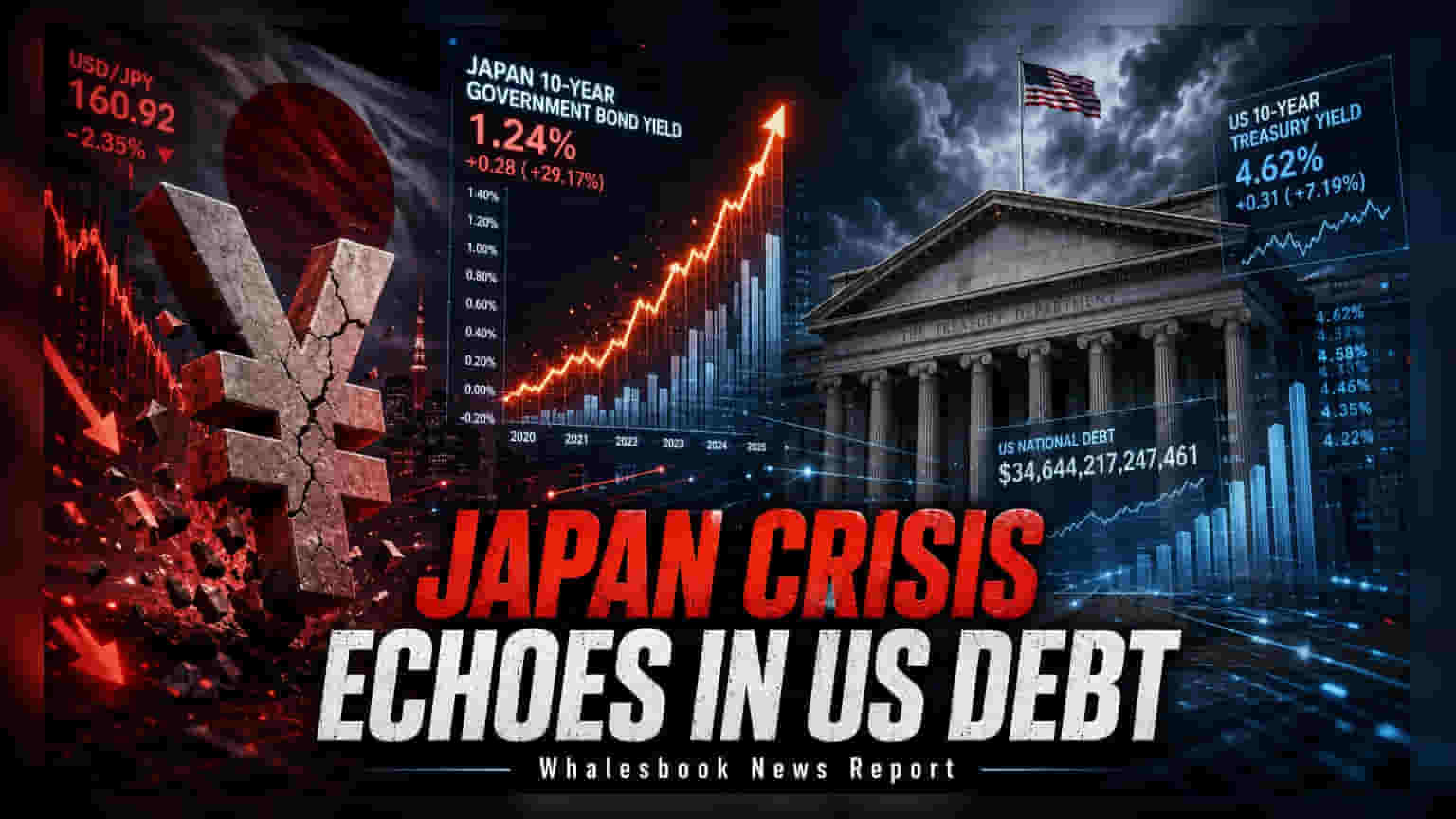

The Japanese yen has touched a 40-year low against the US dollar, even after intervention efforts, while long-term bond yields climb to multi-decade highs. The market instability highlights deep-seated fiscal challenges, including a high public debt-to-GDP ratio, which investors are now comparing to fiscal risks in the US, France, Italy, and the UK.

Japan is currently grappling with a significant currency and bond market crisis that has drawn global attention. Despite Japanese authorities spending over $70 billion in May to defend the yen, the currency has depreciated to levels not seen in 40 years. This decline is happening alongside a sharp rise in long-term government bond yields, following the Bank of Japan’s decision to move away from its yield-curve control policy.

Fiscal and Monetary Pressures

The root of the instability lies in Japan’s challenging public finances. With a public debt-to-GDP ratio of 230%, Japan faces the largest debt burden among G7 countries. The government continues to run a primary budget deficit, and policies like increased energy subsidies—introduced to combat oil price shocks—have added pressure to the national budget. The Bank of Japan now faces a difficult dilemma. While it may feel pressure to raise interest rates to combat accelerating inflation and support the yen, doing so would increase borrowing costs for the government, further straining its already fragile fiscal position.

The Carry Trade Impact

A major factor keeping the yen weak is the persistent interest rate gap between Japan and the US. With the Bank of Japan keeping rates relatively low at 1% compared to the US Federal Reserve’s 3.5% policy rate, investors continue to use the yen for the "carry trade." This involves borrowing money in the cheaper Japanese currency to invest in higher-yielding assets denominated in US dollars. This cycle of selling yen to buy dollars has created a self-reinforcing loop that keeps the Japanese currency under consistent pressure.

Global Debt Implications

Financial analysts are closely monitoring these events as a potential warning for other major economies with high debt levels. Nations such as the United States, France, Italy, and the UK are also managing significant fiscal deficits. The US, for instance, is projected to maintain a budget deficit exceeding 6% of its GDP, pushing its debt ratio to levels unseen since World War II. Because a significant portion of US Treasury bonds is held by foreign investors, market participants are concerned that a loss of confidence in fiscal management could trigger volatility in the global bond market similar to past regional debt crises. The key monitorable for investors will be how central banks in these major economies manage the balance between controlling inflation and maintaining stable public debt levels as global borrowing costs remain high.