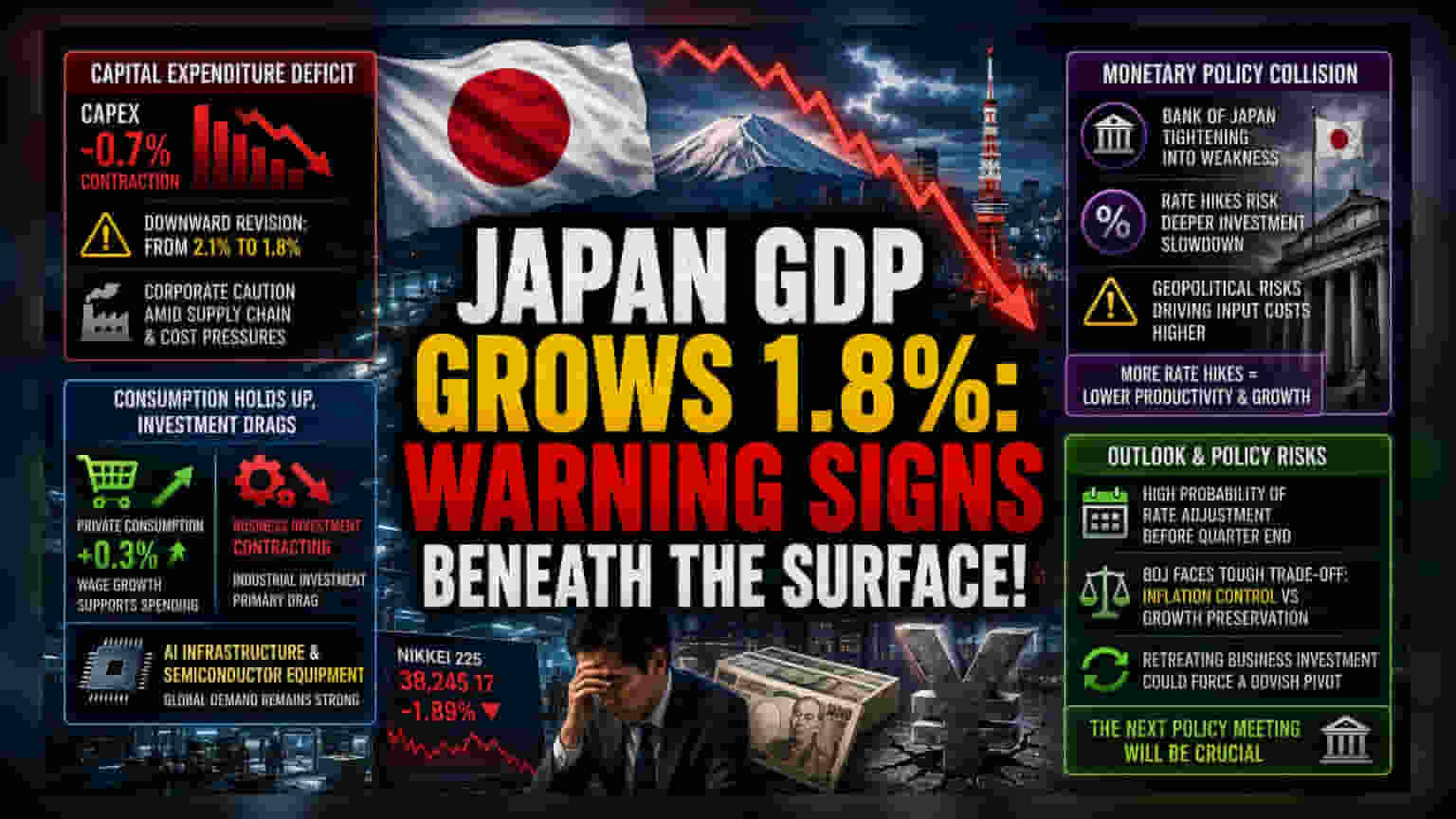

The Capital Expenditure Deficit

While the headline expansion of 1.8% suggests broad resilience, the underlying data reveals a concerning shift in corporate behavior. The downward revision from the initial 2.1% reading is tethered directly to a 0.7% contraction in capital expenditure. This decline signals that Japan’s largest corporations have adopted a defensive stance toward long-term asset allocation, likely influenced by the dual pressures of persistent global supply chain instability and the rising cost of capital. When major firms pull back on equipment and facility spending, it traditionally serves as a precursor to broader industrial stagnation.

Divergence Between Consumption and Investment

The Japanese economy currently relies on a fragile dichotomy: private consumption remains the primary defense against recessionary forces, while industrial investment serves as the primary drag. Household spending managed a 0.3% increase, benefiting from wage growth expectations. Simultaneously, the manufacturing sector is heavily insulated by the relentless global appetite for high-end AI infrastructure. This specific vertical allows Japanese exporters to bypass the broader slump in general capital investment, as demand for semiconductor manufacturing equipment and specialized components remains disconnected from domestic industrial sentiment.

The Forensic Bear Case: Monetary Policy Collision

Analysts are increasingly concerned that the Bank of Japan may be misreading the economic signal by prioritizing inflation control over growth preservation. Raising interest rates into a period where business investment is already contracting could trigger a deeper slump in corporate expansion. While the central bank aims to normalize policy after years of extreme accommodation, the timing remains precarious. If the current geopolitical friction in the Middle East continues to elevate input costs, Japanese firms may slash capital budgets further, creating a feedback loop of lower productivity and stagnant domestic growth. Unlike the United States, where high interest rates are currently absorbed by a robust service sector, Japan’s manufacturing-heavy index is significantly more vulnerable to sudden increases in borrowing costs.

Forward Trajectory and Policy Risks

Market participants are now pricing in a high probability of a rate adjustment before the quarter ends. The focus for investors remains on the upcoming policy board meeting, where the central bank must balance the necessity of curbing currency volatility against the risk of choking off nascent economic momentum. If business investment continues to retreat, the Bank of Japan may find itself forced to pivot back to dovish rhetoric, regardless of inflationary pressures, to prevent a hard landing for the nation’s industrial base.