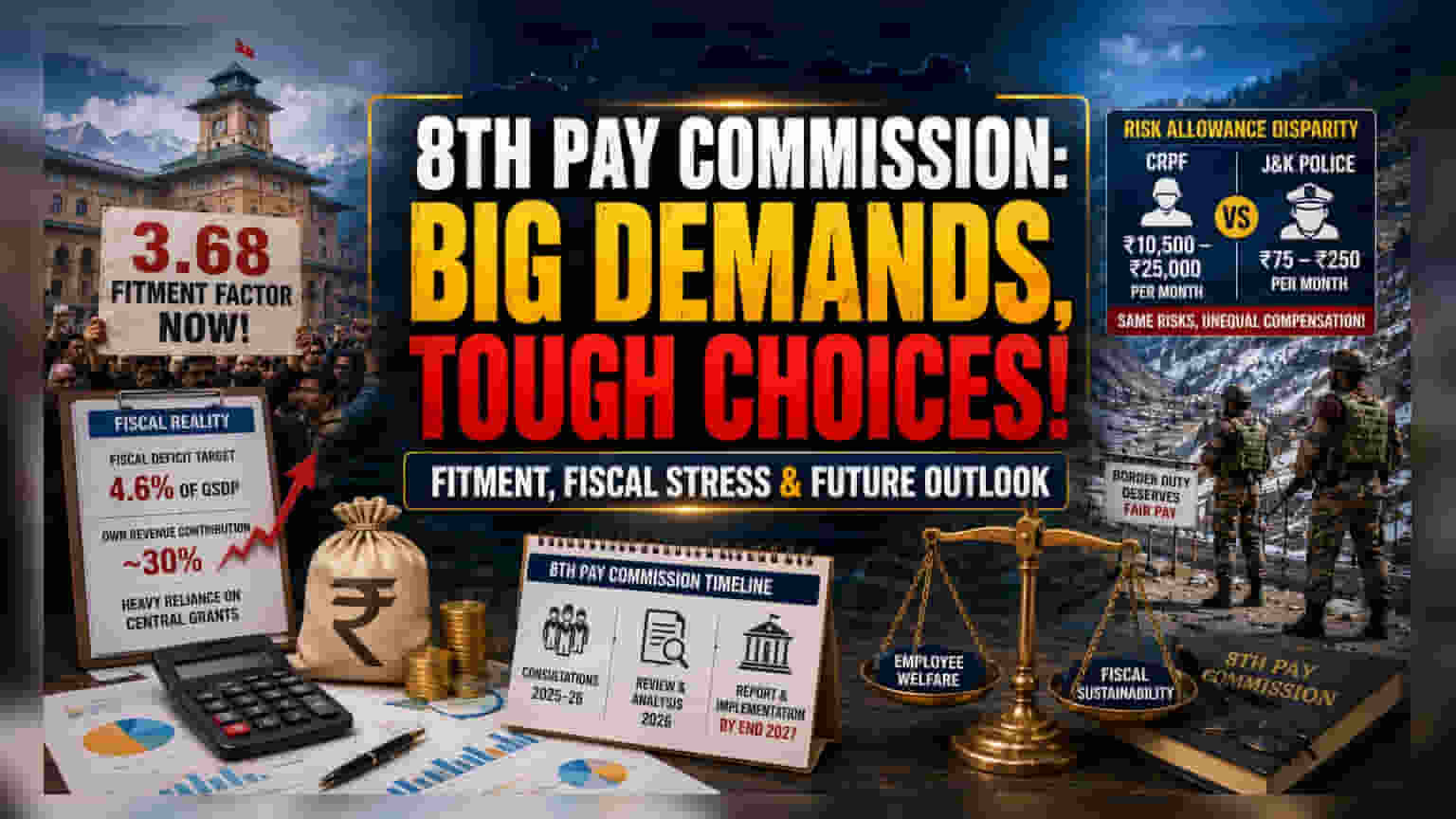

The Fiscal Balancing Act

The demand for a 3.68 fitment factor by Jammu and Kashmir employee unions marks a significant escalation in the 8th Pay Commission consultation cycle. While employee representatives view this as a necessary correction for inflationary pressures and systemic disparities, the proposal presents a formidable challenge to the Union Territory’s fiscal framework. With the UT’s fiscal deficit already under pressure—targeted at 4.6% of GSDP for the 2026-27 financial year—any upward revision in committed expenditure like salaries and pensions risks constraining the limited policy space available for capital investment. The current reliance on Central grants-in-aid, which form the bedrock of the UT’s budget, underscores the precarious nature of maintaining fiscal sustainability while accommodating substantial wage hikes.

Disparities in Risk and Remuneration

A core component of the employee memorandum centers on the demand for parity in risk allowances, highlighting a stark divide between the Jammu and Kashmir Police and central armed forces. While personnel from forces such as the Central Reserve Police Force (CRPF) receive monthly risk allowances ranging between ₹10,500 and ₹25,000, J&K Police personnel reportedly receive significantly lower amounts, sometimes in the range of ₹75 to ₹250 per month. This discrepancy has fueled long-standing grievances, with union leaders arguing that the operational hazards—ranging from counter-insurgency operations to border security—are shared equally, yet compensation remains fundamentally unequal. The push for a special border allowance further reflects the unique operational reality of the region, where duty near the Line of Control necessitates higher financial recognition.

The Forensic Bear Case: Structural Weaknesses

From a purely institutional perspective, the push for such aggressive pay revisions faces significant hurdles. Historically, the implementation of pay commission recommendations often forces state governments into a cycle of revenue deficit. With J&K’s own revenue generation contributing only a fraction of its total receipts—approximately 30%—the territory is uniquely vulnerable to shocks in central transfers. Furthermore, past audits have indicated that heavy reliance on revenue expenditure can "crowd out" essential capital projects. If the 8th Pay Commission adopts the requested 3.68 fitment factor, it could trigger a retroactive financial obligation for arrears dating back to January 2026, forcing the local administration to either aggressively curb developmental spending or request supplemental central assistance, neither of which aligns with the current push for fiscal discipline.

Future Outlook and Procedural Realities

While unions remain optimistic about a rollout by the end of 2027, the commission’s final report remains subject to comprehensive reviews of fiscal sustainability and inflation indices. The government’s mandate explicitly includes evaluating the fiscal impact of these hikes alongside national growth trajectories. Consequently, the final fitment factor may likely settle at a more conservative level than the 3.68 requested, as the commission attempts to balance social security improvements for nearly 4.8 million employees with the overarching requirement of maintaining national fiscal consolidation targets.