A new Deloitte report reveals a Rs 25 lakh crore credit gap for Indian MSMEs, with only 14% having formal access to finance. This massive untapped market presents a significant growth opportunity for banks and NBFCs, but investors should monitor the associated asset quality risks as lenders expand into this segment.

What Happened

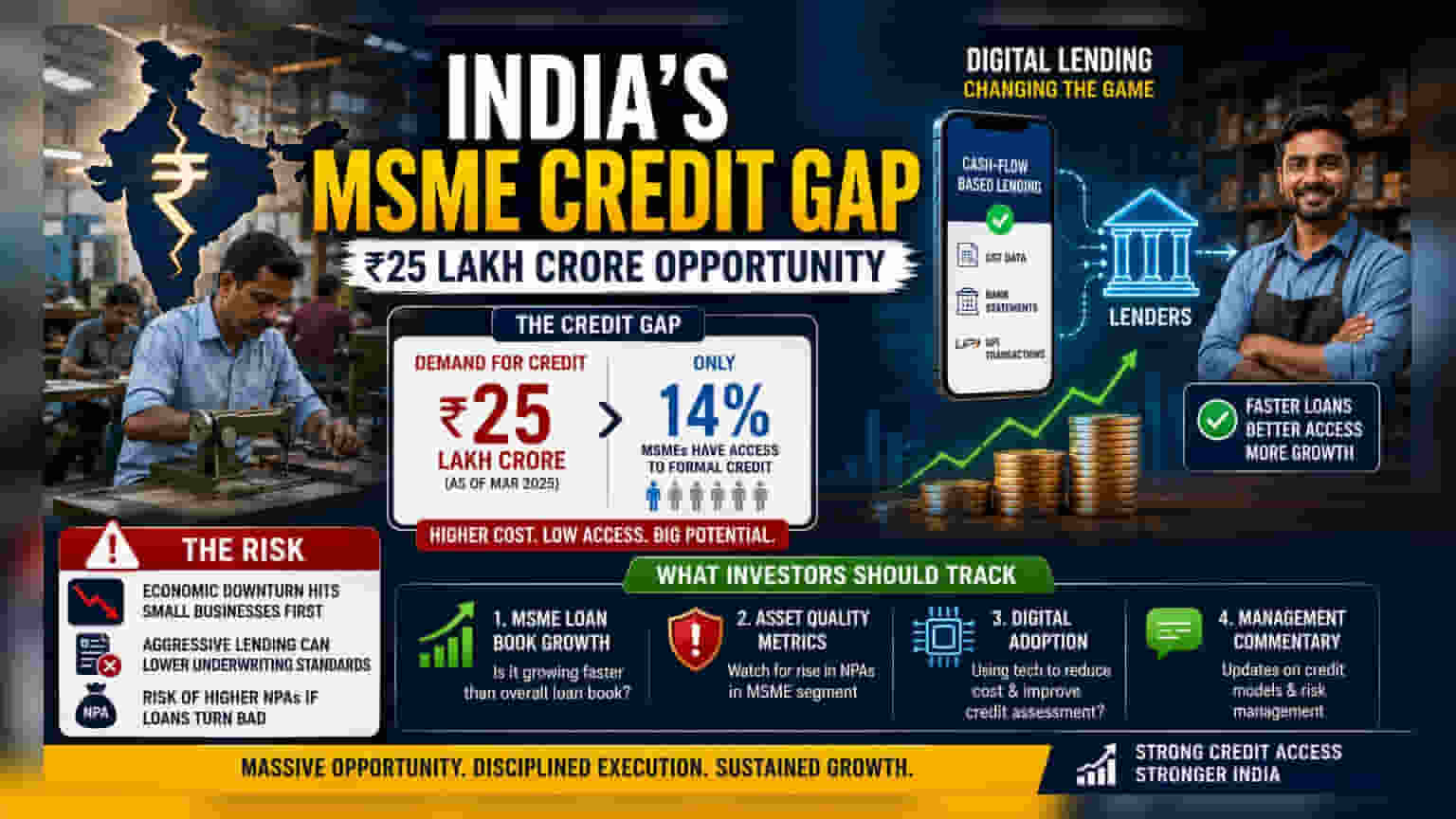

A recent report by Deloitte has highlighted a significant hurdle in the Indian economy: the massive credit gap faced by Micro, Small, and Medium Enterprises (MSMEs). The report estimates this credit gap—the difference between the demand for credit and the supply from formal sources—to be around Rs 25 lakh crore as of March 2025. Despite India’s rapid growth in digital payments and UPI transactions, only 14% of MSMEs currently have access to formal, institutional credit.

Most of these businesses still rely on informal sources, such as local money lenders, which typically charge much higher interest rates. This situation persists even though 89% of Indian adults now hold a financial account, suggesting that having an account does not automatically translate to getting a loan.

The Growth Opportunity For Lenders

For investors in the banking and non-banking finance company (NBFC) sectors, this data points to a massive potential market. Financial institutions have been actively trying to capture this segment for years because MSME loans generally offer higher profit margins compared to loans given to large corporations or retail home buyers.

To bridge this gap, many lenders are shifting their approach. Instead of asking for traditional collateral, such as land or property, they are increasingly using cash-flow-based lending. By analyzing digital data like GST filings, bank statements, and UPI transaction history, lenders can assess the repayment capacity of smaller businesses more accurately and quickly. This shift is a key strategic move for many banks and NBFCs aiming to expand their loan books in the coming years.

The Asset Quality Risk

While the growth potential is high, the MSME segment is not without risks. Investors should understand that MSME lending is typically more sensitive to economic cycles than large corporate lending. When the broader economy slows down, small businesses are often the first to feel the pressure, which can lead to higher defaults.

As banks and NBFCs aggressively chase this market, there is a risk of lowering underwriting standards to gain market share. If lenders do not monitor the quality of these loans carefully, it could lead to higher Non-Performing Assets (NPAs), which are loans where the borrower has stopped paying interest or principal. In previous cycles, excessive growth in unsecured or semi-secured MSME lending has often led to spikes in bad loans for lenders.

What Investors Should Track

As the banking sector seeks to tap into this Rs 25 lakh crore opportunity, investors should look beyond just loan growth numbers. When analyzing quarterly reports for banks and NBFCs, consider focusing on these areas:

- MSME Loan Book Growth: Is the lender growing its MSME book faster than its overall loan book?

- Asset Quality Metrics: Watch for any rise in NPAs specifically within the MSME or small-business category.

- Digital Adoption: Is the lender successfully using technology to reduce the cost of assessing and processing these smaller loans?

- Management Commentary: Listen for updates on their credit-scoring models and risk management strategies for this segment.

Ultimately, while the untapped MSME market offers a path for sustained long-term growth, the ability of lenders to maintain a balance between expanding credit and keeping bad loans under control will define the success of this strategy.