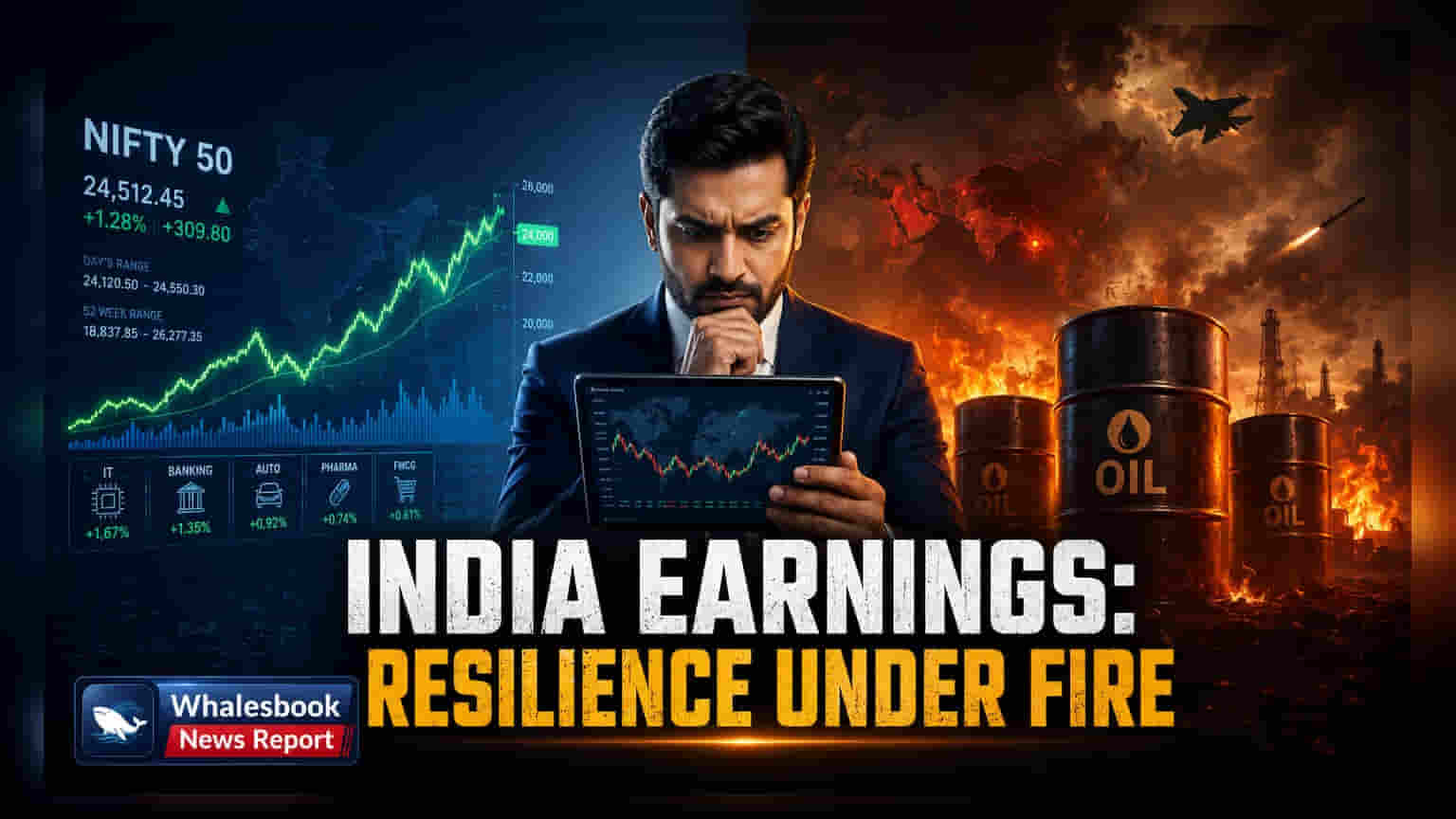

The Valuation Disconnect

Current market optimism for Nifty 50 earnings projections hinges on the assumption that geopolitical shocks will be brief. Analyst consensus has barely adjusted expectations downward, yet the gap between current stock valuations and rising operational costs is growing. The belief that global supply chains will soon return to normal overlooks the reality of higher freight costs and volatile oil prices, which directly increase expenses for India's manufacturing and logistics industries.

Sectoral Vulnerability and Margin Erosion

Looking beyond the main index figures, a closer review shows greater profit declines in sectors dependent on international shipping. Industries like aviation and processed exports are already experiencing reduced profit margins. The IT services sector adds another layer of complexity, as fewer new hires suggest companies are cutting back on future workforce expansion. This indicates that company leaders are preparing for a longer economic slowdown than current market sentiment suggests. While India's domestic demand has historically provided a cushion, high interest rates and ongoing retail inflation are beginning to slow spending on non-essentials. This threatens the revenue growth that currently supports high stock price multiples.

Structural Weaknesses and The Bear Case

Financial institutions are increasingly examining Indian corporate balance sheets, especially for highly indebted companies struggling with high interest rates. A major risk is India's reliance on energy imports; any further conflict escalation in the Strait of Hormuz could trigger a broad economic shock that overshadows domestic growth. Stress tests also indicate that a 2% drop in profitability is a likely outcome, not a worst-case scenario, if current shipping delays continue through the second half of the fiscal year. Skeptics note that if the rupee continues to fall, the cost of repaying foreign debt will increase, putting more pressure on cash flow already strained by operating expenses.

The Path Forward

Investors should monitor changes in management guidance on inventory and debt repayment. As the fiscal year progresses, relying solely on sales growth to hide shrinking profit margins will likely become unsustainable. Expect increased market swings as the gap between flat GDP growth forecasts and optimistic earnings estimates forces a reassessment of investment risk. Investors betting on a return to pre-conflict conditions might be disappointed if the current cycle of rising costs continues to reduce the purchasing power that has historically fueled India's growth.