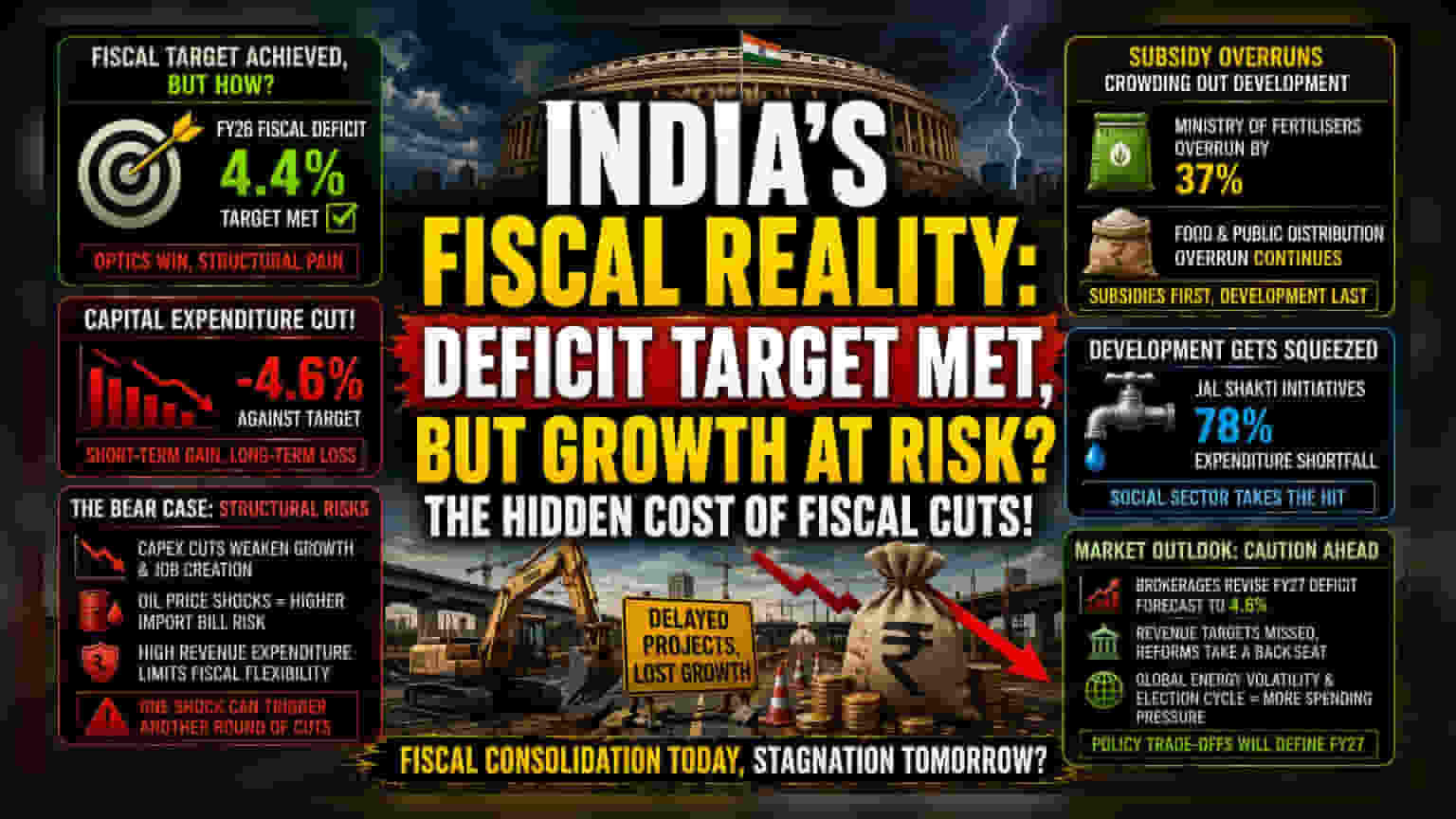

The Illusion of Fiscal Discipline

Meeting the 4.4% fiscal deficit target for FY26 serves as a temporary optics victory, yet the underlying composition of this achievement reveals a troubling reliance on expenditure compression. By curbing capital expenditure by 4.6% against initial targets, the administration has prioritized short-term accounting benchmarks over long-term growth. This strategy effectively hollows out the multiplier effect typically associated with government investment, leaving the economy vulnerable to a deceleration in infrastructure momentum that has defined the previous cycle.

Prioritizing Protection Over Progress

While the government maintains its narrative of fiscal responsibility, internal allocations tell a story of reactive policy rather than strategic planning. The budget overruns in the Ministry of Fertilisers—which exceeded allocations by a massive 37%—and the Ministry of Food & Public Distribution underscore the government’s exposure to global commodity price shocks. These mandatory welfare and agricultural subsidies essentially cannibalized the budgets of development-oriented departments. By shielding the electorate from inflationary pressures through massive subsidy injections, the state has been forced to cannibalize its own social sector projects, most notably the Jal Shakti initiatives, which saw a 78% expenditure shortfall.

The Forensic Bear Case: Structural Vulnerabilities

The contraction in spending is not merely a budgetary technicality; it represents a fundamental risk to the projected growth trajectory. When capital expenditure is the primary lever for fiscal consolidation, the economy risks a stagnation in demand and industrial capacity expansion. Furthermore, the persistent reliance on high-cost revenue expenditure, particularly within the Ministry of Defence, limits the government's ability to maneuver when external shocks occur. Any sustained disruption in the Strait of Hormuz will immediately spike the import bill for energy and fertilizers, likely forcing another round of painful, reactive spending cuts if tax buoyancy remains muted.

Market Outlook and Sovereign Risk

The shift in spending priorities suggests that the upcoming fiscal year will be defined by trade-offs rather than expansion. With private investment yet to reach a sustainable threshold of self-sufficiency, the government’s inability to meet its revenue receipt targets forces it into a corner. As brokerage houses like Kotak revise FY27 deficit expectations upward to 4.6%, the market is increasingly pricing in a scenario where structural reforms in tax collection become secondary to managing existing liabilities. Investors should prepare for a period where policy consistency is tested by the realities of global energy volatility and the inevitable demand for increased social spending as the election cycle approaches.