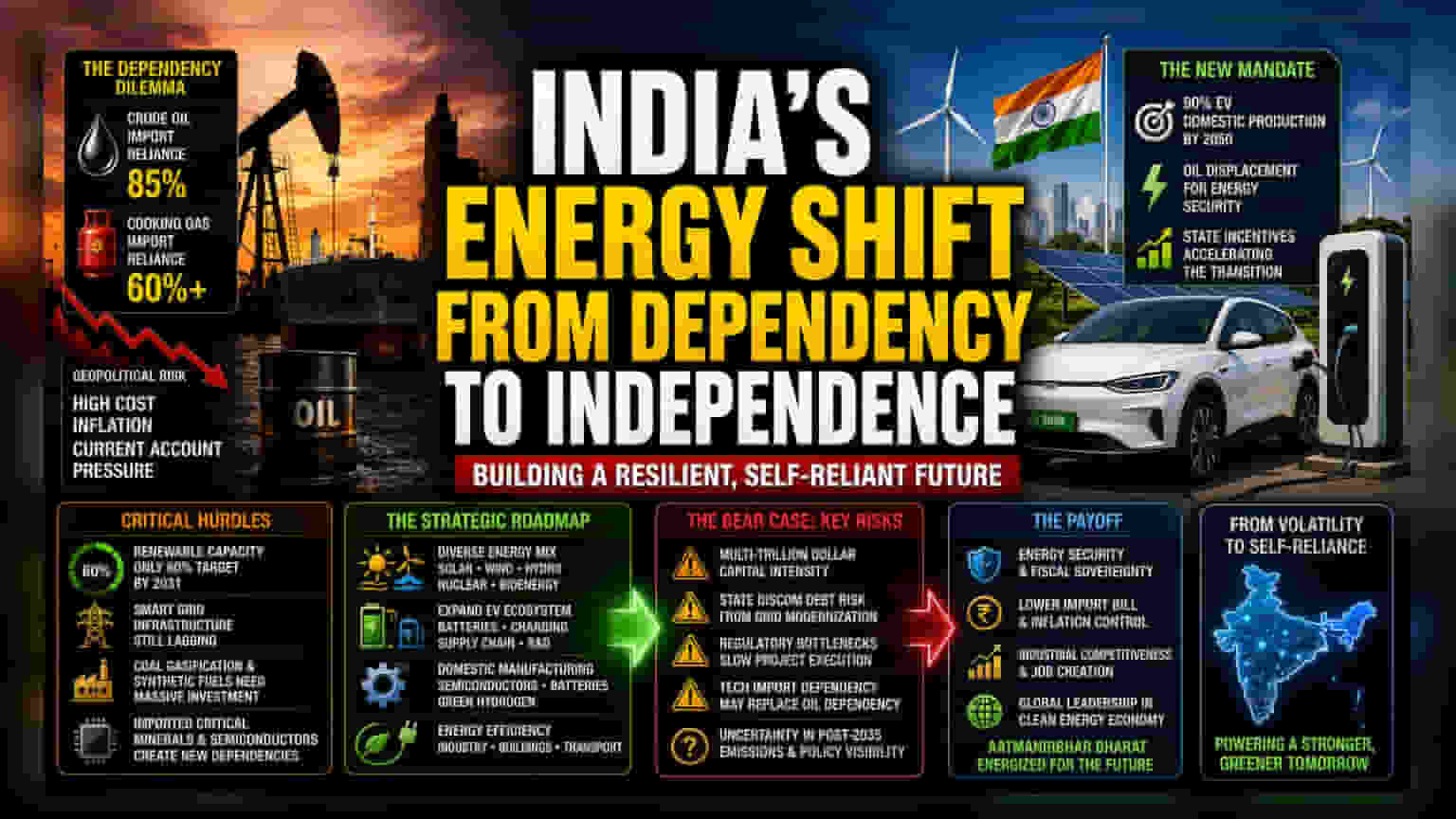

The Geopolitical Impetus for Structural Decoupling

India’s strategic vulnerability to energy supply shocks has reached a point where traditional hedging is no longer sufficient. With import reliance for crude oil at 85% and critical cooking gases exceeding 60%, the nation is effectively underwriting the geopolitical instability of West Asia. This dependency acts as a permanent drag on the current account, creating a recurring inflationary impulse whenever global supply chains fracture. The shift toward renewables is not merely an environmental mandate but a calculated move to establish fiscal sovereignty.

The Shift Toward Managed Autonomy

Unlike previous decarbonization efforts, which were heavily influenced by external international climate protocols, the current policy evolution emphasizes domestic energy resilience. The government is recalibrating its industrial policy to prioritize oil displacement. By accelerating the adoption of electric vehicles to a target of 90% in domestic production by 2050, the state aims to bypass the volatile global price fluctuations inherent in petroleum and CNG markets. This initiative is supported by aggressive state-level incentives designed to break the reliance on fossil-fuel-intensive transportation before the broader grid decarbonization is fully realized.

Critical Hurdles and the Infrastructure Gap

While the mandate for energy independence is clear, the transition faces significant friction regarding infrastructure and capital allocation. A robust, smart-grid architecture is a prerequisite for a fleet-wide electric vehicle transition, yet current renewable generation targets for 2031 only cover 60% of total capacity. Furthermore, the push for coal gasification and synthetic fuel production represents a bridge technology that requires massive front-loaded capital expenditures. Investors must monitor whether the government can balance these industrial investments without ballooning the fiscal deficit. The reliance on imported critical minerals for both battery storage and semiconductor manufacturing creates a new, albeit different, form of supply chain dependency that may replace oil-based vulnerabilities in the coming decade.

The Forensic Bear Case: Risks to the Transition

The primary structural risk remains the pace of capital intensity. Replacing 85% of crude import demand necessitates a multi-trillion dollar overhaul of both the power grid and the domestic automotive supply chain. Skeptics point to the potential for significant debt accumulation among state-owned utility providers, who bear the brunt of managing intermittent renewable loads. Moreover, historical data shows that aggressive transitions often encounter regulatory bottlenecks. If the domestic manufacturing of semiconductors and battery-grade minerals stalls, India may simply transition from an oil-import economy to a technology-import economy, failing to achieve the desired degree of true strategic autonomy. The lack of granular, post-2035 emissions clarity further complicates long-term capital forecasting for private institutional investors.