Confederation of Indian Industry (CII) leadership is calling for a strategic shift in India’s growth model, moving from basic infrastructure expansion to a complex integration of AI infrastructure and energy-intensive industrialization. The mandate emphasizes that sustaining global competitiveness now hinges on aligning data center proliferation with a massive scaling of nuclear and renewable power, while simultaneously accelerating second-generation structural reforms.

The Shift Toward Resource-Intensive Growth

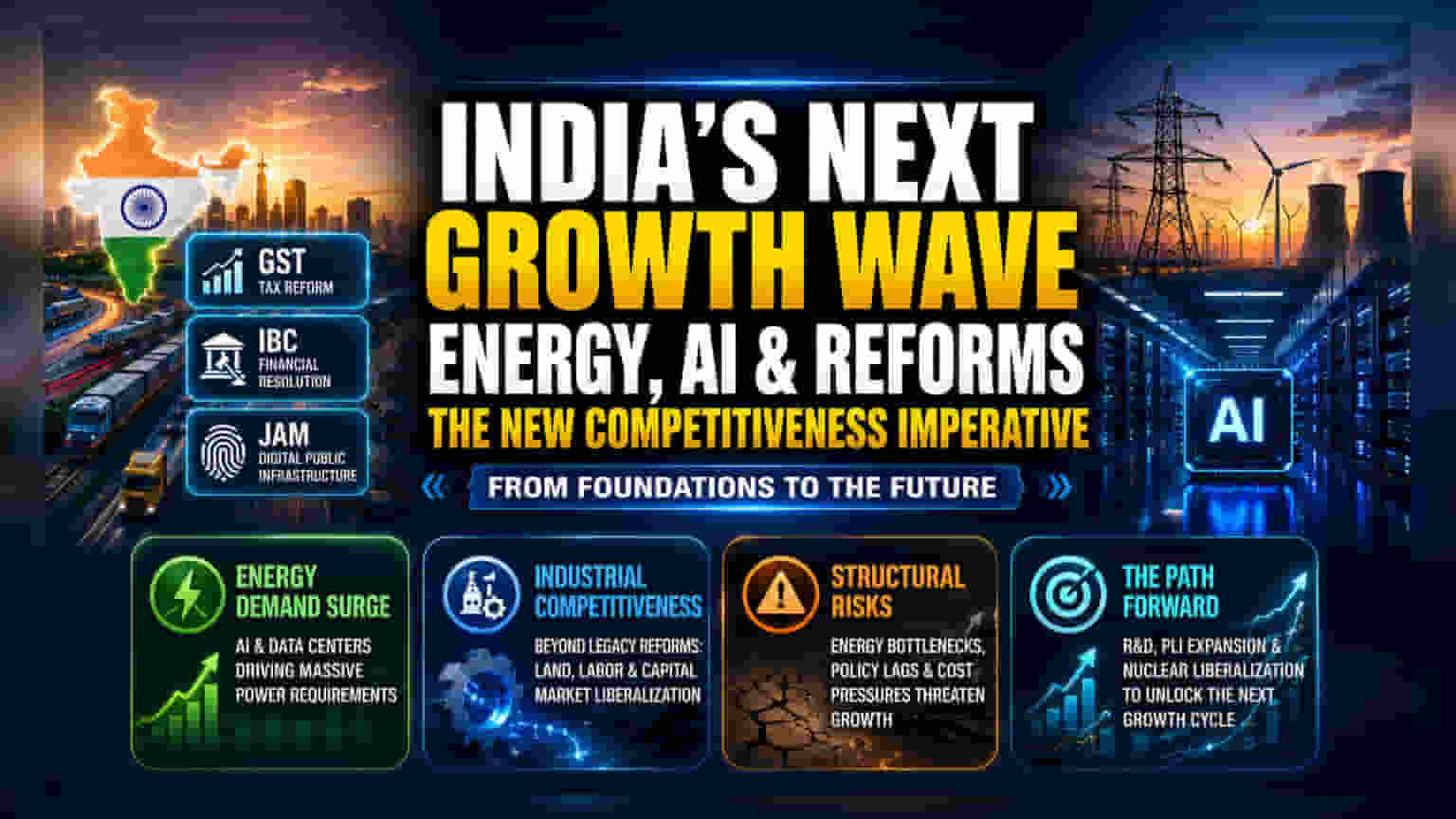

The narrative surrounding India’s economic evolution is transitioning from the foundational gains of the previous twelve years—defined by digital public infrastructure and logistics—toward a more demanding phase of industrial strategy. The Confederation of Indian Industry (CII) now highlights that the country’s next stage of competitiveness is tethered to a high-voltage requirement: the massive energy demand of artificial intelligence and data center clusters. This transition signals an industrial reality where energy policy is no longer a peripheral concern but the primary bottleneck for technological scaling.

The Infrastructure-Innovation Paradox

While the past decade featured the successful deployment of the Goods and Services Tax, the Insolvency and Bankruptcy Code, and the JAM trinity, analysts argue that the law of diminishing returns may soon apply to these legacy reforms. The current push for increased research and development spending by private enterprise suggests an admission that capital expenditure on physical assets alone is insufficient. Market participants are increasingly monitoring whether India can successfully attract high-end manufacturing and AI investment without further aggressive liberalization of land, labor, and capital markets. The competitive gap compared to emerging peers remains tied to the execution speed of these secondary-tier reforms.

The Structural Bear Case: Energy Bottlenecks and Policy Lag

Despite the optimistic outlook on green energy and nuclear expansion, significant structural risks persist. The primary concern is the synchronization of regulatory frameworks with private capital requirements. For instance, the transition toward private participation in nuclear energy involves complex regulatory hurdles and long gestation periods that may not satisfy immediate growth targets. Furthermore, the push for energy-intensive AI infrastructure risks placing localized pressure on grid stability. Skeptics note that unless India achieves a drastic reduction in the cost of industrial power, the margin profiles for energy-heavy, data-reliant industries may face persistent compression. Historical precedent in similar developing economies suggests that massive infrastructure transitions are often accompanied by significant fiscal strain and inflation volatility if private sector R&D does not match public investment.

Outlook on Industrial Competitiveness

Looking forward, the success of India’s economic trajectory will likely be measured by the fluidity of the energy-data nexus. The focus remains on whether policy moves can shift from enabling basic connectivity to fostering high-value innovation. Investors are watching for tangible updates on Production-Linked Incentive (PLI) expansions and specific nuclear sector liberalization, which serve as bellwethers for the government’s willingness to cede control to private enterprise in critical, high-barrier sectors.