The Shift in Market Mechanics

The traditional dominance of equity-centric analysis often leaves retail participants exposed to interest rate risk. While stocks capture headlines, the underlying pricing of risk in the Indian debt market dictates the cost of capital across the entire financial system. Current indicators suggest a decoupling from historical stability as structural liquidity management by the Reserve Bank of India (RBI) meets a demanding borrowing schedule from the central government.

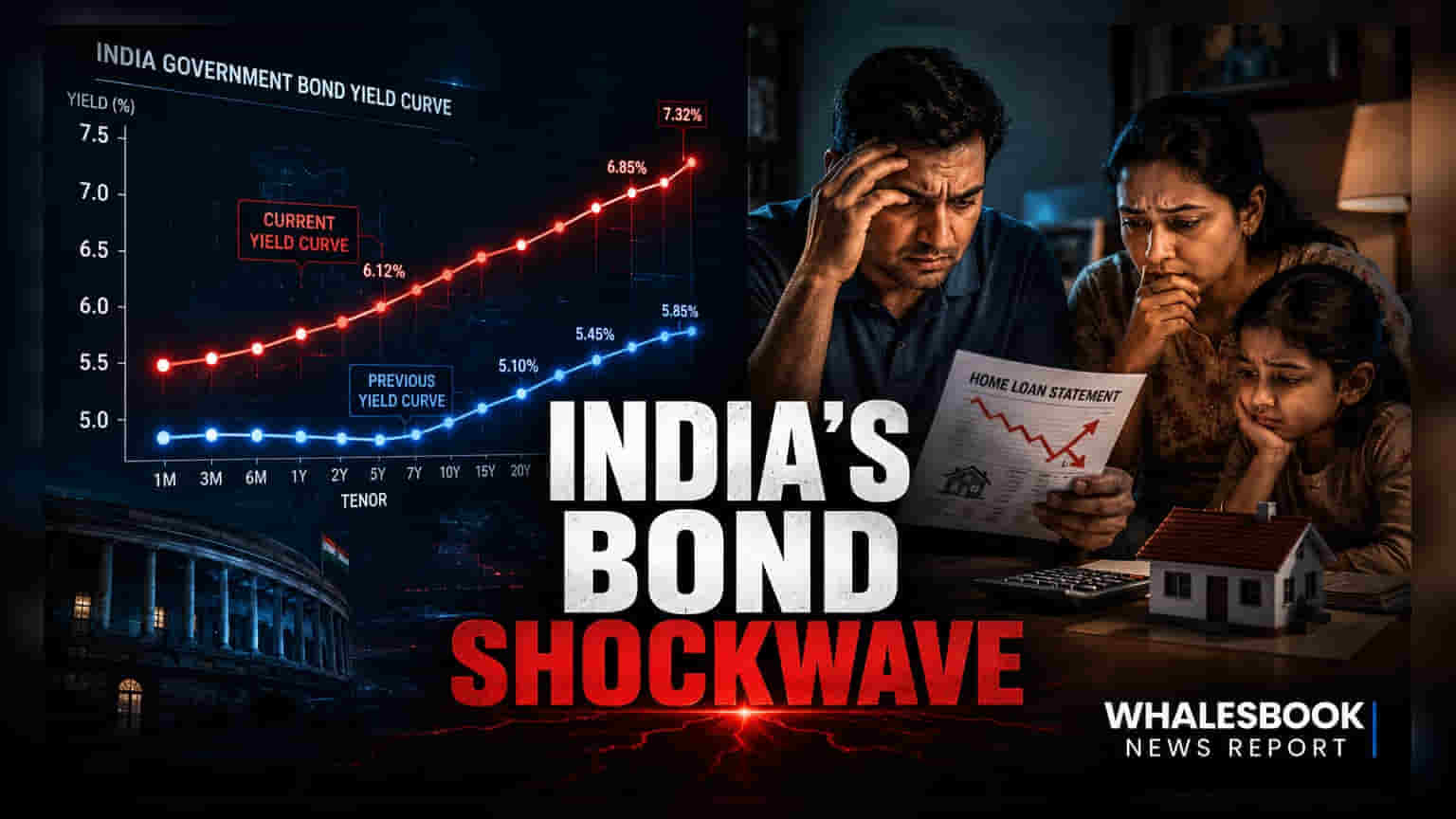

Yield Curve Dynamics and Systemic Impact

Unlike markets where yield curve inversion serves as a reliable recessionary signal, the Indian context remains heavily influenced by the Statutory Liquidity Ratio (SLR) and internal accounting standards like 'Held to Maturity' (HTM) classifications. These structural buffers effectively dampen volatility but can mask underlying duration risk. When banks maintain large HTM portfolios, the transmission of policy rate changes to the real economy often experiences significant lag. However, as foreign institutional participation rises following global index inclusions, the insulating effect of domestic mandates is beginning to erode. This integration with global capital flows means that domestic yields are increasingly susceptible to US Treasury volatility, necessitating a sharper focus on the correlation between long-term bond yields and currency stability.

The Forensic Bear Case: Vulnerabilities in Debt Exposure

Investors currently positioned in long-duration debt funds face significant structural risks if inflationary pressures force the RBI into a 'higher-for-longer' rate posture. The primary weakness in the current environment is the lag between policy rate hikes and the subsequent repricing of floating-rate home loans, which creates a 'debt trap' for highly leveraged retail borrowers. Furthermore, corporate credit spreads over government securities remain thin, suggesting the market is not yet fully pricing in potential defaults should the cost of borrowing remain elevated. If systemic liquidity evaporates—a scenario often triggered by aggressive open market operations—the lack of depth in the secondary corporate bond market could lead to liquidity crunches, forcing fund managers to mark down assets precisely when cash is needed for redemptions.

Forecasting the Path Forward

Market participants should shift their focus from headline repo rate adjustments toward the spread between the 10-year and 2-year government securities. This specific differential provides a cleaner read on medium-term growth expectations and inflation risk premiums. As the government continues its fiscal consolidation path, the reduction in gross market borrowing remains the most significant tailwind for yields. Conversely, any deviation from fiscal targets would likely trigger an immediate sell-off in the long end of the curve, pressuring valuations for both fixed-income portfolios and interest-rate-sensitive equity sectors like banking and real estate.