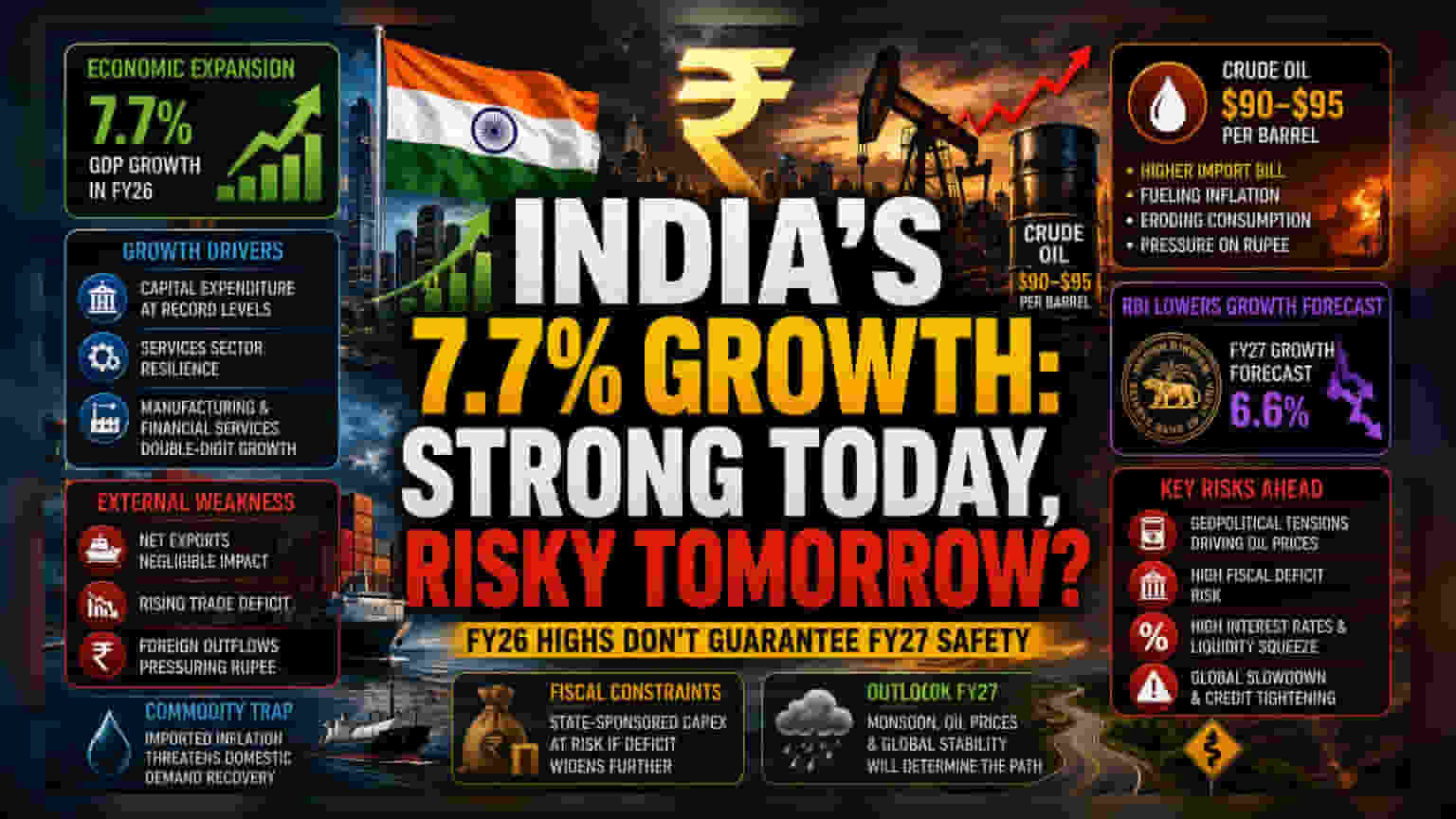

The Illusion of Domestic Decoupling

While the 7.7% expansion headline serves as a testament to the economy’s internal momentum, the divergence between headline GDP and the deteriorating external environment is widening. The growth was heavily skewed toward government-mandated capital expenditure and service-sector resilience, effectively masking the negligible contribution of net exports. While manufacturing and financial services posted double-digit gains, these metrics are inherently lagged, capturing a pre-conflict environment that is rapidly dissolving.

The Commodity Trap and External Exposure

The pivot point for the current fiscal year is the energy import bill. Unlike previous years where India’s trade deficit was somewhat manageable, the escalation of the US-Iran conflict has introduced structural volatility into the crude oil markets. With the Reserve Bank of India lowering its growth forecast to 6.6%, the central bank is implicitly admitting that the protective wall around the Indian economy is thinning. Crude oil prices, now hovering in the $90-$95 per barrel range, act as a direct tax on the Indian consumer, potentially triggering a vicious cycle of cost-push inflation that could erode the very discretionary spending that powered the FY26 recovery.

The Forensic Bear Case

A critical risk factor often ignored in the bullish consensus is the high correlation between current capital formation and state-funded projects. If the fiscal deficit widens due to ballooning energy subsidies or debt-servicing costs from a weakening rupee, the government’s ability to sustain this level of investment will be severely curtailed. Furthermore, the external sector’s weakness is not merely a matter of lower exports; it represents a fundamental liquidity squeeze. Foreign institutional outflows have intensified as global risk sentiment deteriorates, placing persistent downward pressure on the rupee and complicating the central bank’s interest rate strategy. The assumption that the domestic sector can remain decoupled from global trade contraction for another four quarters ignores historical precedents where high interest rates and imported inflation eventually forced a correction in private investment.

The Outlook for FY27

Moving forward, the economy faces a transition from growth-at-all-costs to a period of consolidation. The 6.6% growth target remains an optimistic ceiling, contingent upon the stability of the monsoon cycle and the containment of geopolitical escalation. While the government remains focused on long-term structural integrity, the immediate outlook is characterized by a thinning buffer, where any further spike in commodity prices or a sharper-than-anticipated tightening of global credit conditions will likely force further downward revisions to growth expectations.