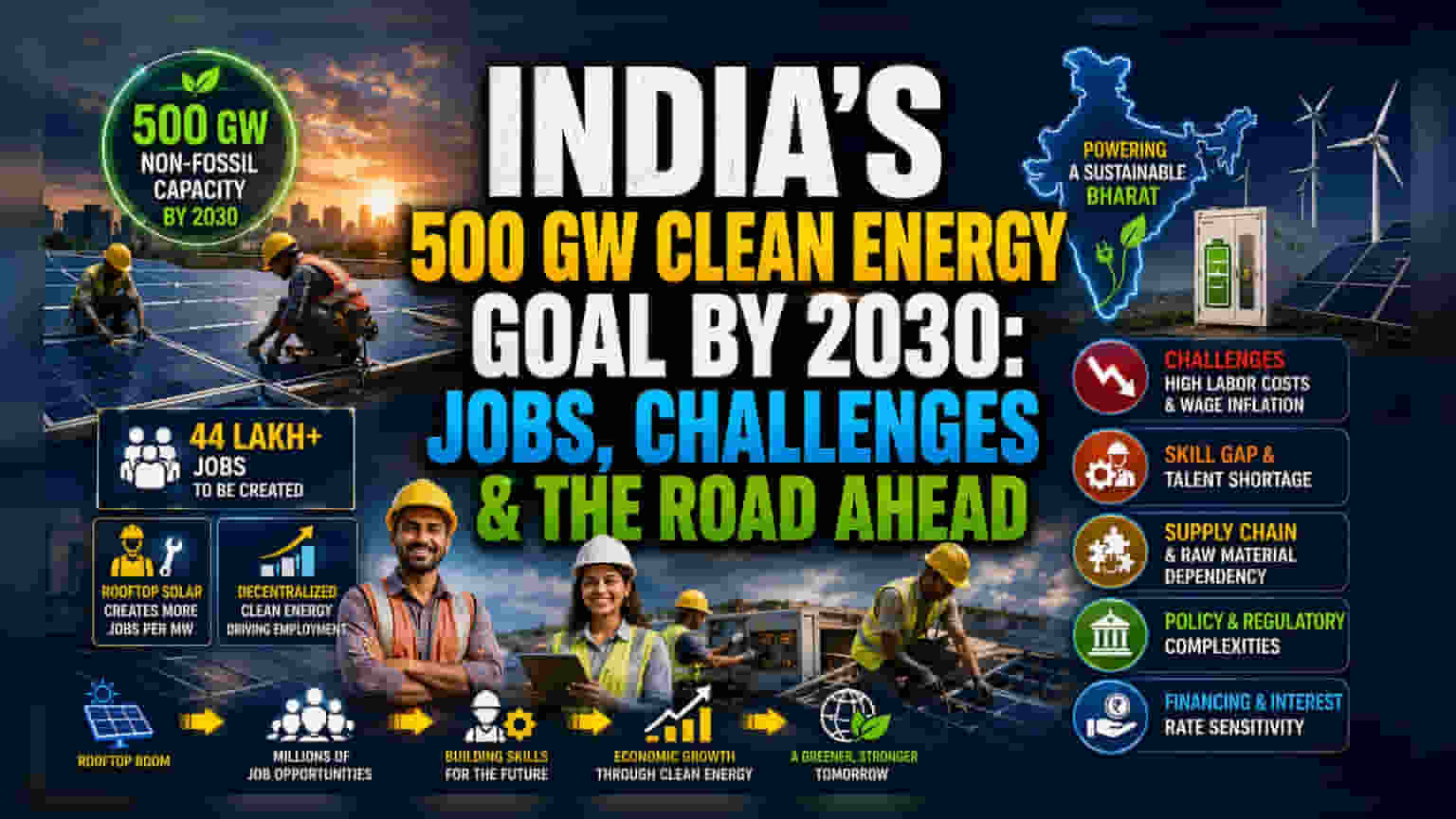

The Labor-Capital Paradox

The economic narrative surrounding India’s 500 GW non-fossil capacity mandate often centers on generation potential, but the underlying labor dynamics reveal a more complex operational reality. The transition toward decentralized energy, particularly rooftop solar, necessitates a shift from capital-intensive utility projects to labor-heavy, site-specific installations. While this promises to create millions of full-time equivalent positions, the reliance on manual labor-intensive deployment models introduces significant scalability friction. Efficiency metrics suggest that while rooftop solar creates exponentially more jobs per megawatt than utility-scale alternatives, this higher headcount requirement correlates with increased per-unit overhead and complex project management, potentially straining thin profit margins for domestic installers if wage inflation outpaces productivity gains.

Scaling Against Regional Headwinds

Unlike the aggressive expansion observed in the European or Chinese renewables sectors, India’s progress remains tethered to domestic manufacturing capacity and land-use policies. Competitor benchmarks indicate that India’s ability to hit the 2030 goal is constrained by raw material volatility—specifically the dependence on imported photovoltaic cells and specialized components. While local initiatives aim to boost module production, the current pipeline suggests a persistent supply-demand gap. Furthermore, when compared to the historical pace of grid-scale wind and solar deployment, the rooftop sector faces fragmented regulatory hurdles across individual states, which often creates a patchwork of implementation challenges that can stall growth cycles.

Structural Weaknesses and Human Capital Risks

The sector’s rapid expansion masks a deep-seated talent void that threatens long-term operational stability. Data indicates that gender parity remains a peripheral concern, with the majority of female participation confined to administrative rather than technical or engineering roles. This lack of technical integration restricts the available labor pool in a market already struggling to find specialized skill sets. If the industry fails to bridge this gap through structured vocational partnerships, the cost of labor is likely to spike, driven by a shortage of qualified site engineers and specialized installation technicians. Management teams in the energy space are currently grappling with high attrition rates, a byproduct of the sector’s struggle to professionalize its decentralized workforce while maintaining the thin price premiums demanded by budget-conscious residential consumers.

Future Outlook and Policy Sensitivity

Future growth hinges on the government's ability to simplify the PM-KUSUM scheme and standardize grid-connection protocols. Market participants are watching for shifts in subsidy structures, which have historically dictated the pace of adoption. Analysts suggest that without a transition toward higher automation in module manufacturing and streamlined permitting, the 44 lakh job projection may be hampered by execution delays. Capital expenditure in this sector is highly sensitive to interest rate fluctuations, and any tightening in credit availability for small-scale installers could dampen the momentum required to meet the 2030 milestones.