Indian states allocated Rs 1.9 lakh crore for energy subsidies in FY 2024-25, making it the largest share of their total subsidy bill. This high level of spending, combined with rising interest payments on public debt, reduces the fiscal space for infrastructure development, creating a long-term challenge for state economies.

What Happened

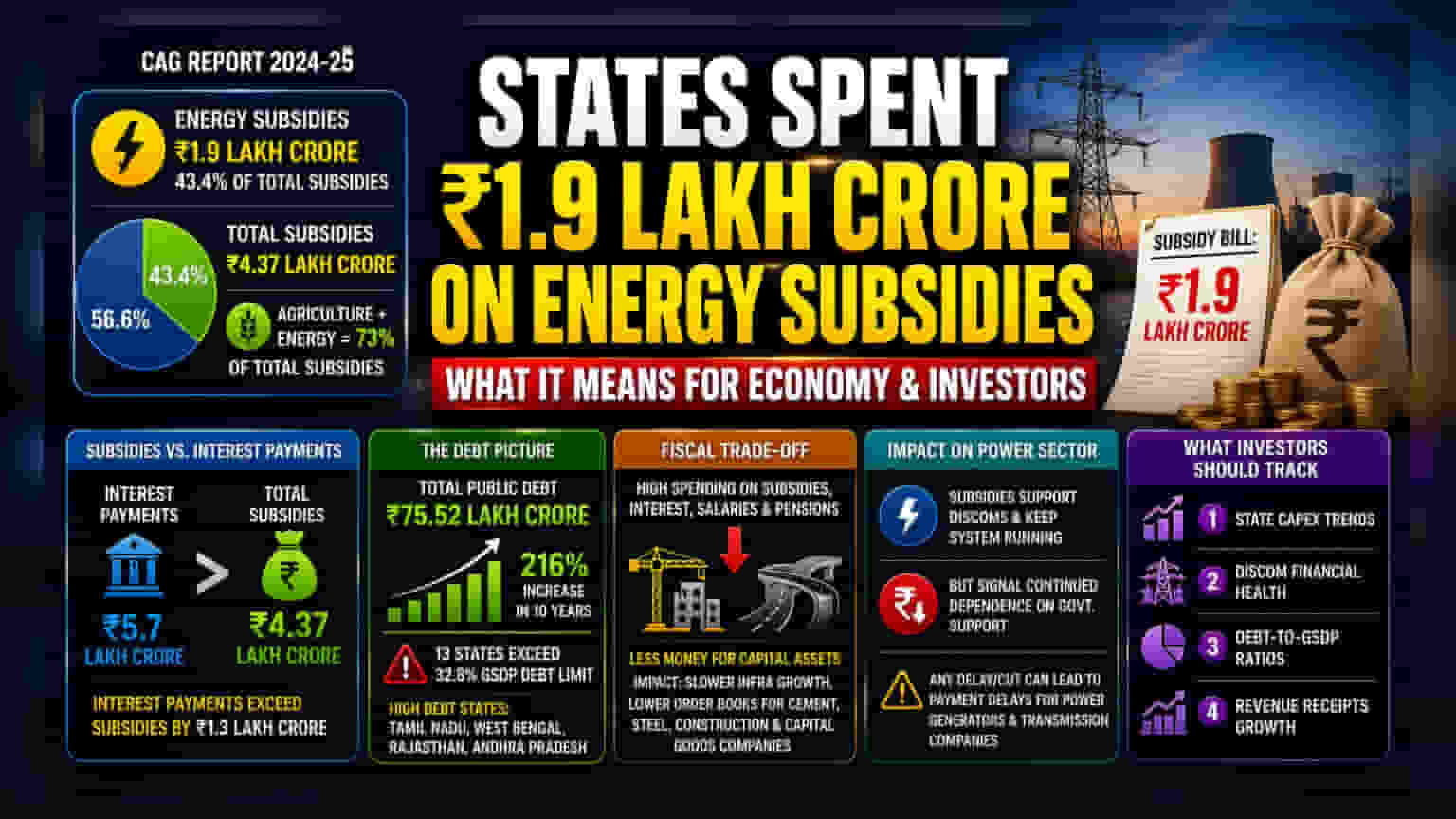

Indian states collectively spent Rs 1.9 lakh crore on energy subsidies during the 2024-25 fiscal year. According to the Comptroller and Auditor General (CAG) of India, this amount formed 43.4% of the total subsidy expenditure of Rs 4.37 lakh crore. These subsidies are largely directed towards supporting power distribution companies (DISCOMs) and providing electricity at lower rates to household and agricultural consumers. The energy sector, combined with agriculture, accounted for nearly 73% of all state subsidies, reflecting the high fiscal priority placed on these areas.

The Trade-Off: Subsidies vs. Infrastructure

For investors and the broader economy, the critical issue is 'fiscal space.' When state governments commit a massive portion of their budgets to subsidies, interest payments, salaries, and pensions, they have less money left to spend on capital assets like roads, bridges, and power infrastructure.

In the 2024-25 fiscal year, interest payments on accumulated debt reached Rs 5.7 lakh crore, which exceeded total subsidy spending by Rs 1.3 lakh crore. When committed expenses such as these dominate the budget, states are forced to rely more on borrowing. This reduction in capital spending can slow down the order book growth for companies in the cement, steel, construction, and capital goods sectors that rely heavily on government project execution.

The Debt Picture

Total public debt for states is projected to rise to Rs 75.52 lakh crore for 2024-25, marking a 216% increase over the past decade. The CAG report highlights that 13 states now have total liabilities exceeding the Finance Commission’s suggested limit of 32.8% of their Gross State Domestic Product (GSDP). High debt levels limit a state’s ability to respond to future economic shocks or invest in growth-oriented projects. States like Tamil Nadu, West Bengal, Rajasthan, and Andhra Pradesh currently hold some of the highest debt loads, which investors often track when assessing the regional investment climate.

Impact on the Power Sector

While the subsidy payments provide a lifeline to DISCOMs, the underlying financial health of these entities remains a key concern. Historically, DISCOMs have struggled with operational inefficiencies, high technical losses, and delayed payments to power generation companies. For investors in the power sector, state subsidies are a double-edged sword: they keep the electricity ecosystem running, but they also signal that the power distribution model continues to rely on government support rather than profitability. If these subsidies were to be reduced or delayed, it could lead to payment delays for private power producers and transmission companies.

What Investors Should Track

Investors may monitor the following indicators to understand how these fiscal trends affect their portfolios:

- State Capital Expenditure (Capex) Trends: Watch for budget announcements to see if states are prioritizing long-term infrastructure over recurring subsidies.

- DISCOM Financial Health: The ability of states to pay subsidies on time is directly linked to the cash flow of power utility companies.

- Debt-to-GSDP Ratios: A rising ratio in specific states may lead to a slowdown in local public sector project awarding.

- Revenue Receipts: Since states borrow when their revenue cannot cover their expenses, consistent revenue growth is the only way to manage the current debt burden without sacrificing development spending.