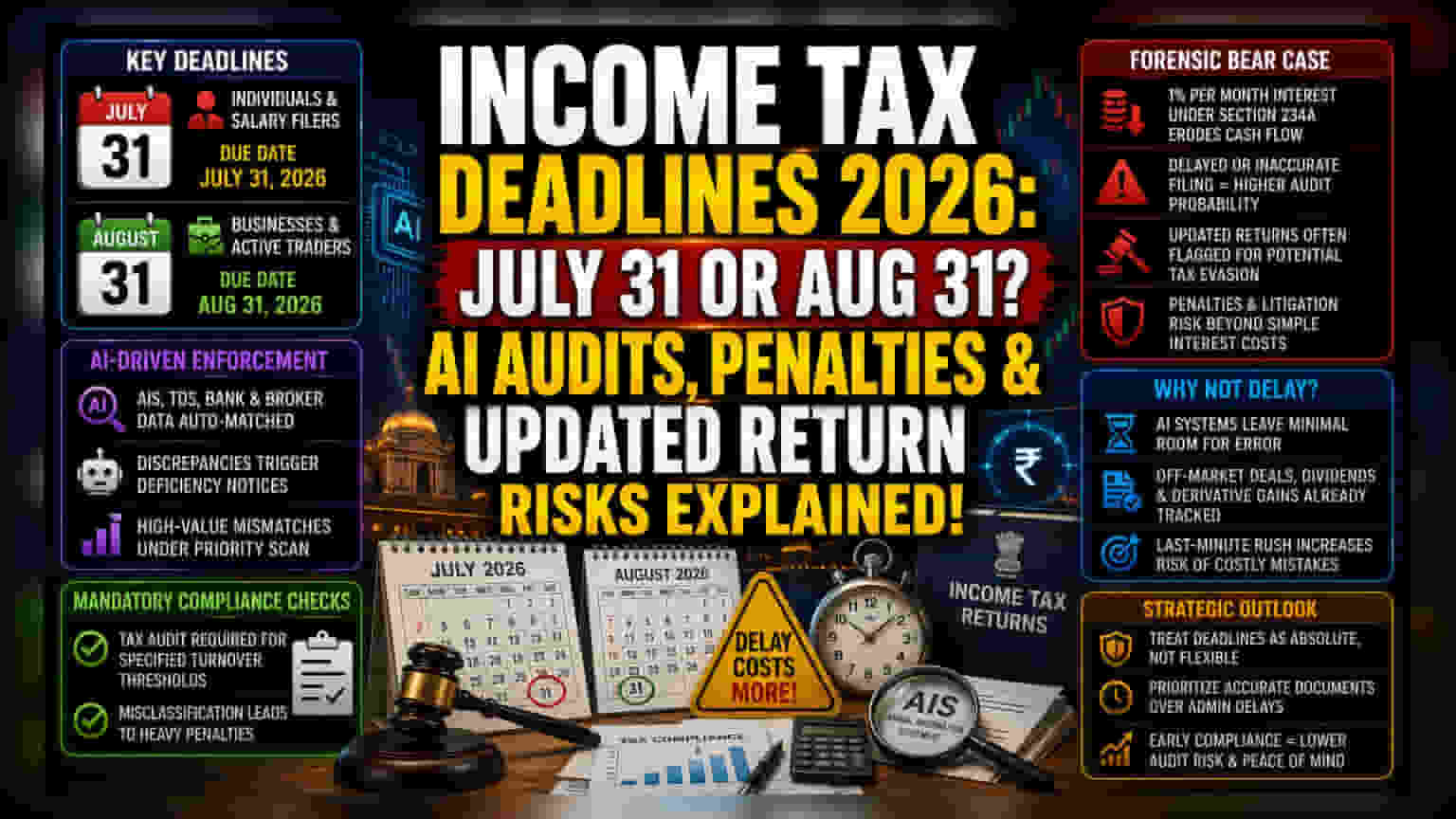

The Compliance Pressure Cooker

The established timeline for the current assessment cycle reflects a deliberate effort by the tax authority to segment the massive influx of filings, yet it places significant operational strain on the administrative infrastructure. While the July 31 cutoff for individuals remains a standard hurdle, the August 31 extension for business cases and active traders acknowledges the heightened volatility and record participation volumes seen in domestic equity derivatives. This bifurcation effectively creates a two-tier oversight system where active market participants, particularly those engaged in high-frequency trading, are granted a temporary grace period that is increasingly scrutinized by data-matching algorithms.

The Data-Driven Enforcement Shift

Unlike previous years, the tax authority is leveraging advanced AI-based analytics to cross-verify Annual Information Statements (AIS) against self-declared income. Traders utilizing the August 31 deadline must navigate a landscape where off-market transactions, dividend receipts, and derivative settlement gains are already pre-populated in taxpayer accounts. Failure to reconcile these figures by the primary deadlines often results in automated deficiency notices. Historically, taxpayers who delay filings under the assumption that they can simply pay interest under Section 234A find themselves targeted for closer review, as the department’s systems now prioritize discrepancies in high-value business turnover over minor salaried reporting errors.

The Forensic Bear Case

From a risk perspective, the reliance on the updated return facility—which persists until March 2031—often masks underlying liquidity issues for businesses. While the statute allows for belated filings, the accumulation of interest under Section 234A at 1% per month quickly erodes working capital. Furthermore, taxpayers relying on the extended August window often overlook the mandatory nature of tax audit reporting for specific turnover thresholds. If a business misclassifies its activity as non-audit to reach the August deadline, the resulting penalties for late audit filing are severe. Additionally, the recent trend of using 'updated' returns to mask initial income under-reporting is increasingly seen by regulators as a signal for potential investigations into tax evasion, effectively tagging the filer for future litigation or audit cycles.

Strategic Outlook for Filers

Professional consensus among tax consultants suggests that the official deadlines should be treated as absolute, particularly for those with complex portfolios. The escalating use of technology for enforcement means that the cost of late compliance extends beyond simple penalty fees into the realm of increased audit probability. As the system moves toward near-instantaneous reconciliation, the margin for error during the August window is narrowing, forcing businesses to prioritize accurate document collation over administrative delays.