The Strategic Pivot Away from Crude

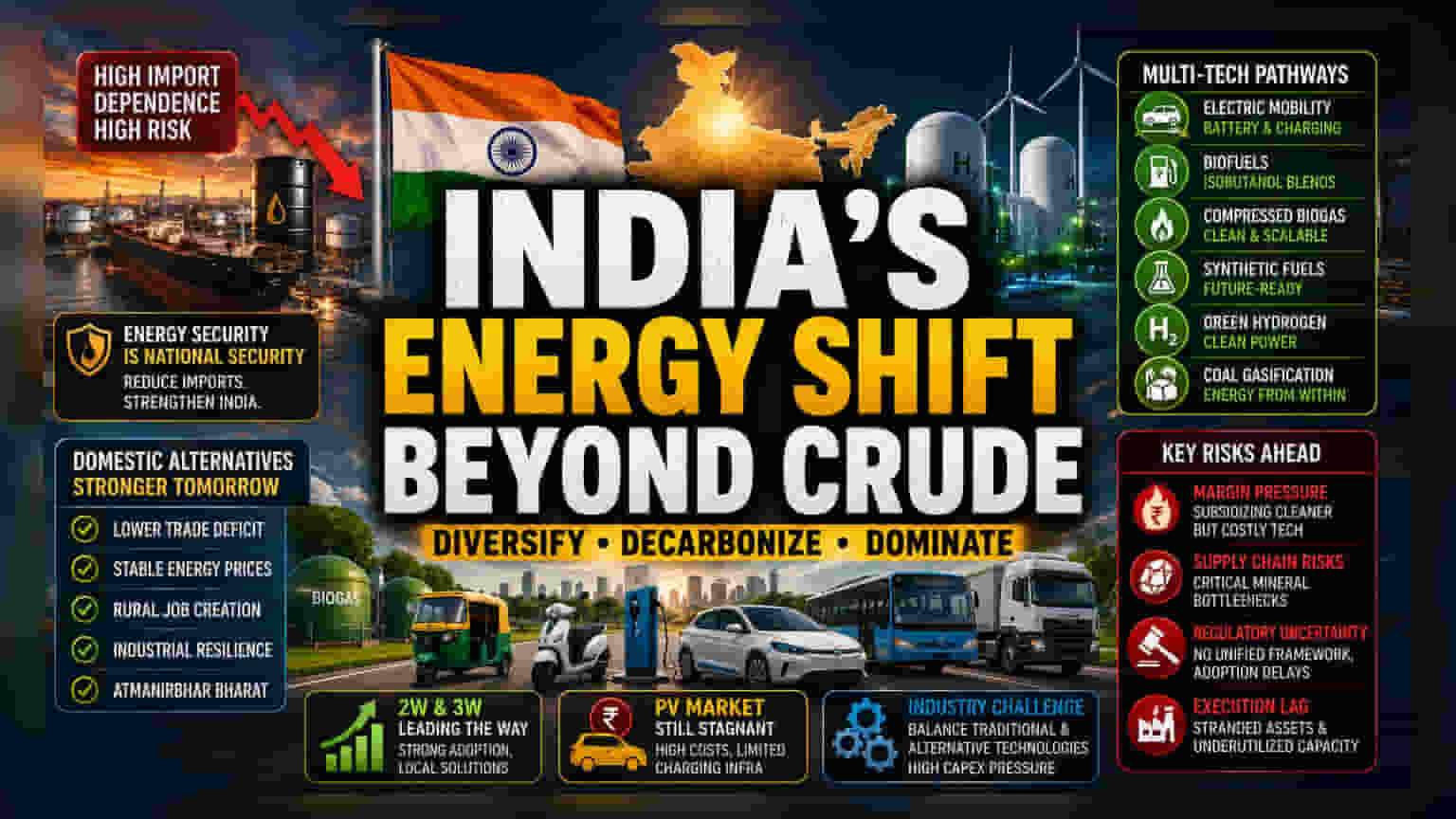

India’s current energy framework faces an existential challenge rooted in its heavy reliance on imported hydrocarbons. Recent supply chain disruptions and volatile pricing in West Asian energy corridors have elevated domestic energy independence from a long-term goal to an immediate macroeconomic priority. The push for localized energy production, as emphasized by government advisors, is not merely an environmental mandate but a defensive maneuver against external shocks that consistently threaten the nation’s current account balance.

Industrial Diversification vs. Market Reality

Unlike previous strategies that favored a singular transition to electric vehicles, current policy now embraces a fragmented, multi-technology approach. By legitimizing pathways like isobutanol blends, compressed biogas, and synthetic fuels alongside electrification, the administration is lowering the barriers to entry for heavy-duty transport and industrial machinery—sectors that remain tethered to traditional fuels. This hedge allows domestic conglomerates to capitalize on existing infrastructure while incrementally integrating green hydrogen and coal gasification. However, this breadth creates capital expenditure pressure, as manufacturers must now balance production lines between traditional internal combustion engines and nascent alternative fuel technologies.

The Structural Impediments to Adoption

While the two- and three-wheeler segments have achieved rapid electrification due to lower battery density requirements and localized charging needs, the passenger vehicle market continues to stagnate. High upfront costs and a lack of unified national charging infrastructure remain significant headwinds. Furthermore, the push for coal gasification, while touted as a secure energy source, faces criticism from analysts who cite the high carbon intensity and complex capital requirements necessary to scale such plants to commercial viability. Investors should monitor whether these mandates lead to margin compression for automotive OEMs, who are currently forced to subsidize the adoption of cleaner but less profitable technologies to meet government-mandated targets.

The Bear Case: Macro Risks and Execution Lag

The move toward localized energy production masks significant fiscal risks. Relying on domestic alternatives often ignores the potential for supply chain bottlenecks in critical minerals required for batteries or the technical complexities of scaling green hydrogen. Furthermore, the lack of a standardized national framework for these diverse fuels creates regulatory uncertainty. If the government fails to synchronize incentives between energy producers and vehicle manufacturers, the resulting industrial friction may manifest as stunted growth in the automotive sector, leaving companies with stranded assets and underutilized production capacity in an increasingly fragmented market.