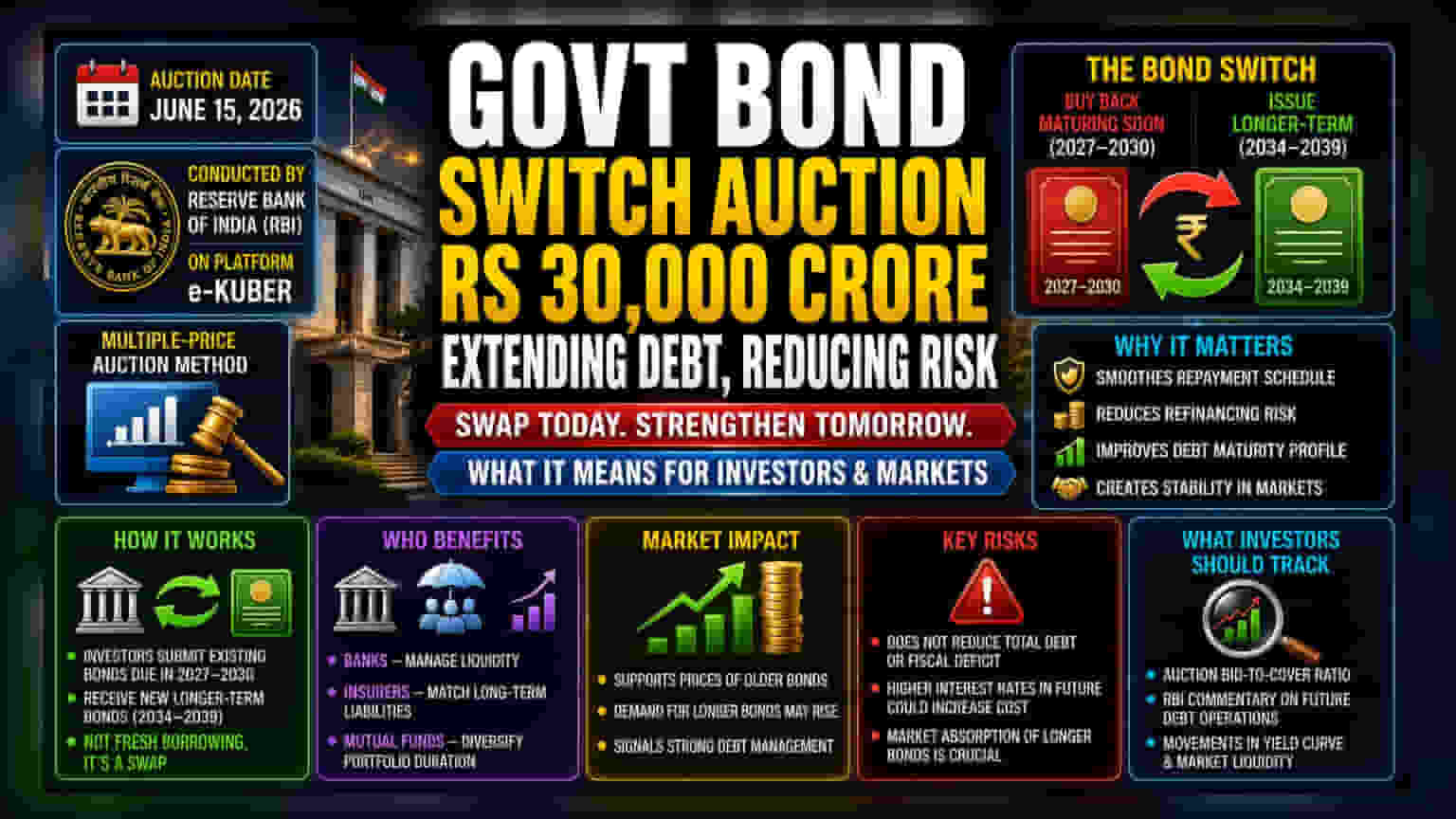

The Indian government will hold a Rs 30,000 crore bond switch auction on June 15 to replace shorter-term debt with longer-term securities. This strategic move helps manage repayment schedules, reducing the risk of having to pay back large amounts of debt at once. It does not reduce total debt but spreads out payment timelines, helping the government maintain better control over its financial obligations.

What Happened

The Indian government has announced plans to conduct a bond switch auction worth Rs 30,000 crore on June 15, 2026. In this process, the government will buy back existing bonds that are set to mature between 2027 and 2030. Simultaneously, it will issue new, longer-term bonds that will mature between 2034 and 2039. The Reserve Bank of India (RBI) will manage this auction on its e-Kuber trading platform using the multiple-price method.

The operation involves specific securities, including debt maturing in the next few years. By repurchasing these older securities and replacing them with new bonds that have a longer timeline, the government is essentially pushing back the date when it needs to repay the principal amount.

Why This Matters For Investors

For investors and the broader bond market, this operation is a tool for "liability management." Governments often face a situation called "maturity bunching," where a large volume of debt is set to be repaid within a short window. If too much debt matures at the same time, the government faces significant pressure to refinance—or borrow fresh money to pay off the old—which can increase borrowing costs if market conditions are unfavorable.

By switching these shorter-term bonds for longer-term ones, the government smooths out its repayment schedule. This reduces refinancing risk. While this does not reduce the total size of the government's debt, it gives the financial system more breathing room by ensuring that the government does not have to scramble for large amounts of cash in the 2027–2030 period.

How The Swap Works

This is not a new borrowing event in terms of raising fresh capital for spending. Instead, it is a swap. Financial institutions, such as banks, insurance companies, and mutual funds that hold these government bonds, participate in the auction. They submit their older bonds to the government and receive the new, longer-dated securities in return.

This helps these institutions adjust their portfolios. For instance, an insurance company that needs to match its long-term payment obligations to policyholders might prefer the longer-dated bonds being issued in this swap, as they provide a steady income stream for a longer period.

Impact on Bond Markets

The bond market often views these operations as neutral to slightly positive for stability. Because the government is reducing the supply of older bonds in the market, it can sometimes support the prices of those bonds. Furthermore, by extending the maturity of its debt, the government signals that it is comfortable managing its financial obligations over the long term, which can help in stabilizing market expectations regarding future borrowing.

Understanding The Risks

While this move helps manage timing, it is important for investors to remember that this does not change the fiscal deficit or the total amount of money the government owes. The government is essentially paying interest on the new bonds for a longer duration. If interest rates in the economy rise significantly in the future, the cost of servicing this long-term debt could become higher than if the government had stayed with the original, shorter-term structure. Additionally, market participants must monitor how much of this new supply the market can absorb without disrupting the overall yield curve, which is the line representing the interest rates of bonds with different maturities.

What Investors Should Track

The primary monitorable for investors is the success of the auction. The market will look at the demand for these new, longer-dated bonds, often referred to as the "bid-to-cover" ratio, which indicates how many investors were willing to participate. Additionally, any commentary from the RBI regarding future debt management operations will be useful for understanding how the government intends to handle its fiscal obligations in the coming quarters.