Beyond the Tariff Cuts

The implementation of the comprehensive trade agreement with Oman represents more than a simple zero-duty arrangement; it is a calculated defensive maneuver for India’s energy infrastructure. By formalizing economic ties with a nation whose geography grants it direct access to the Arabian Sea, India is effectively hedging against the recurring maritime risks associated with the Strait of Hormuz. While the narrative often focuses on the potential for Indian manufactured goods to penetrate West Asian markets, the tangible impact lies in the stabilization of crude oil and liquefied natural gas supply chains. This shift is essential, as the current volatility in global energy pricing demands more predictable logistical corridors.

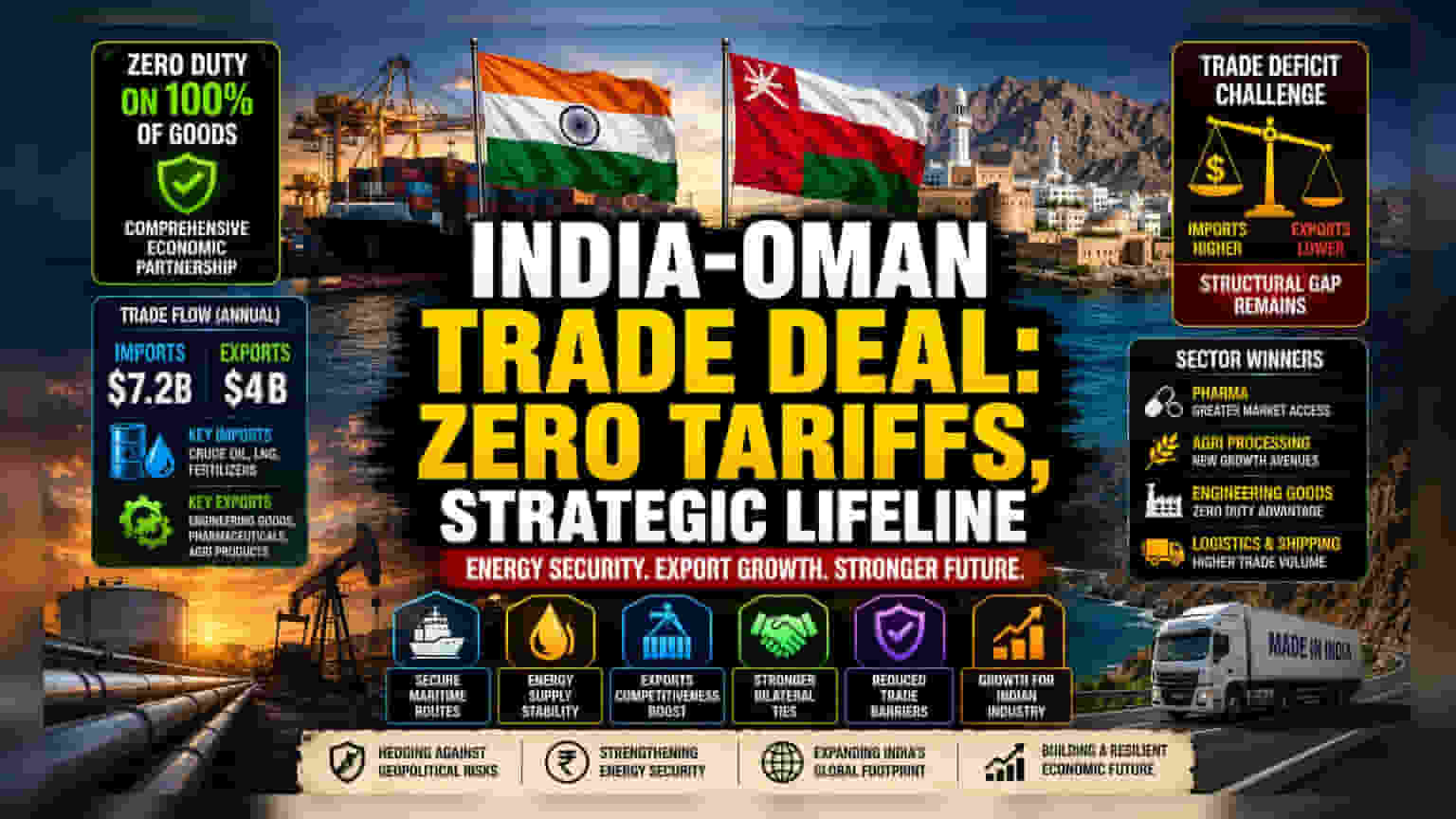

The Competitive Reality of Trade Flows

Analyzing the bilateral balance reveals a persistent structural disparity that this agreement may struggle to address immediately. India’s recent annual imports from Oman, valued at approximately $7.2 billion, remain significantly higher than its $4 billion in exports. The import basket is heavily skewed toward energy-intensive products and fertilizers, commodities that remain susceptible to global price fluctuations regardless of tariff structures. While the zero-duty status on Indian engineering and pharmaceutical exports is a win for manufacturers, these industries face steep competition from both Chinese and European players already entrenched in the Gulf markets. The success of this deal depends less on the removal of trade barriers and more on whether Indian firms can leverage the reduced compliance burdens to improve their price competitiveness against established regional incumbents.

The Sovereign Risk and Structural Weakness

From a cynical financial perspective, this trade pact does not resolve India's fundamental trade deficit issue. Relying on an energy-partner-centric trade strategy creates a trap where the nation’s economic health is tied closely to the fiscal stability of its Gulf counterparts. If Oman faces significant downturns in its own petroleum-dependent economy, the reciprocal benefits of the trade deal could quickly evaporate. Furthermore, regulatory alignment remains a hurdle; historically, cross-border agreements in this region have struggled with non-tariff barriers, including certification delays and sudden shifts in maritime policy. Investors should watch for the specific impact on the balance of payments, as any gains in export market share will need to be substantial to offset the inherent volatility of energy import costs.

Future Outlook and Sector Implications

Expect sector-specific ripples in the coming quarters, particularly for firms specializing in logistics, refining, and specialized manufacturing. Companies currently operating in the pharmaceutical and agricultural processing spaces are likely to receive the most immediate benefit from the streamlined regulatory framework. Market participants should monitor whether the Ministry of Commerce provides updated guidance on specific sectoral quotas, as the current framework remains broad. Long-term, the efficacy of this agreement will be measured by its ability to insulate the Indian rupee from energy-price shocks, rather than the nominal volume of consumer goods exported to the Muscat market.