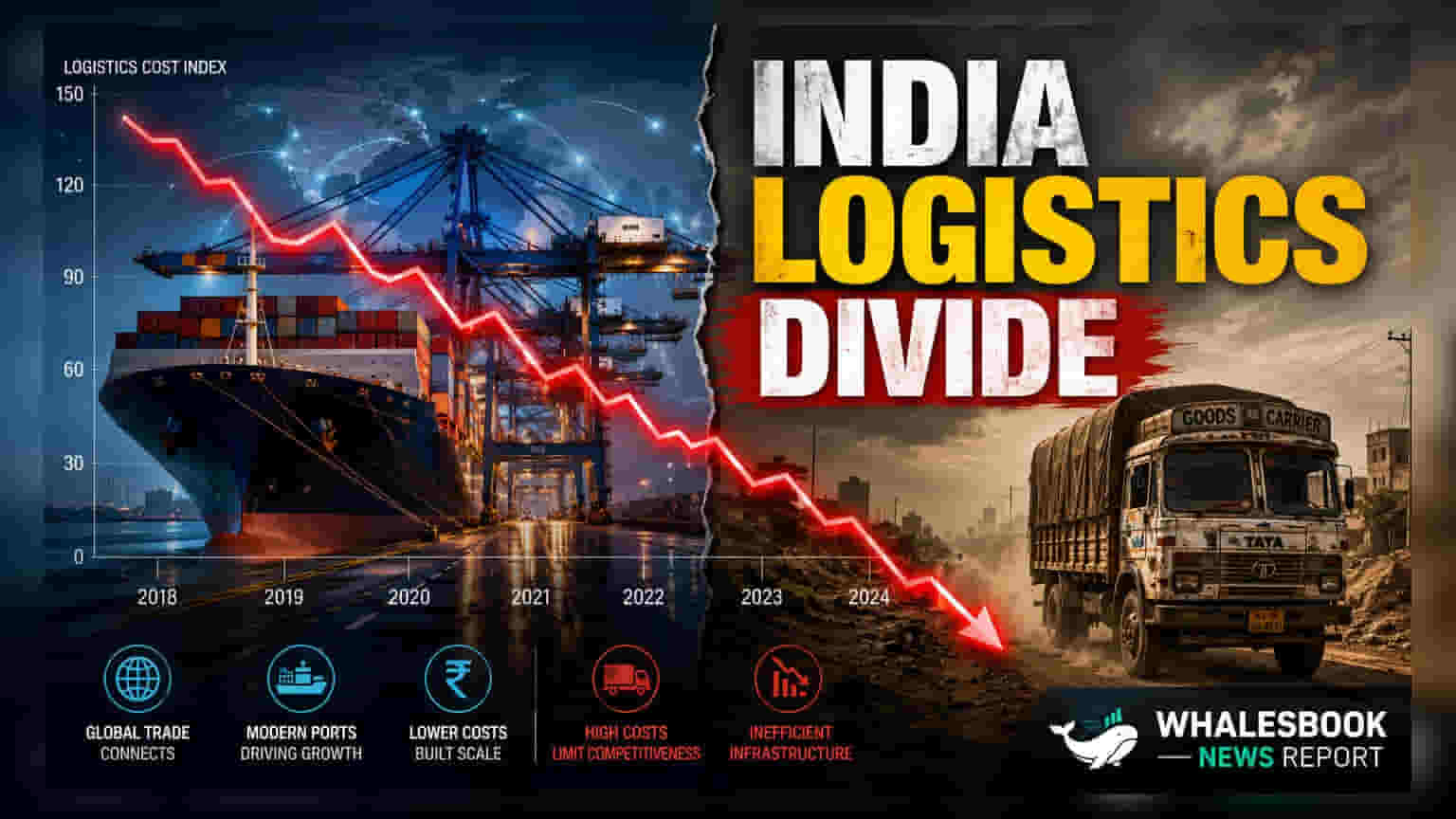

India's logistics expenses have dropped to 8% of GDP, outperforming major economies. However, small chemical companies face costs near 17%, while large firms manage at 7.6%. This disparity highlights that infrastructure benefits are currently favoring larger, better-connected corporations.

India has achieved a significant milestone as national logistics costs have declined to approximately 8.0% of its Gross Domestic Product. This reduction reflects a major improvement from the 13% to 14% range recorded a decade ago. On a global scale, India now appears more cost-efficient than nations like the United States at 8.8%, South Korea at 13.6%, and China at 14.4%. This shift is largely credited to focused government efforts, including the PM GatiShakti National Master Plan, which aims to integrate infrastructure projects, along with the expansion of dedicated freight corridors and improved port connectivity.

While the national average presents a positive outlook, a closer look at the chemical manufacturing sector reveals a divide in operational efficiency. Large corporations with better access to industrial infrastructure have successfully brought their logistics costs down to around 7.6%. In contrast, smaller chemical manufacturers continue to bear a much heavier burden, with logistics costs reaching up to 17% of their total output. This suggests that the advantages of recent infrastructure spending are not reaching all businesses equally.

Investors may note that companies located within major, well-connected industrial hubs are better positioned to benefit from these supply chain improvements. Smaller players, often situated in areas with limited last-mile connectivity, continue to face high overheads, which can compress their profit margins compared to larger, more integrated industry peers. The chemical sector specifically remains hindered by a shortage of specialized warehousing for hazardous materials and fragmented multimodal transport links, which are essential for lowering costs for smaller manufacturers.

Looking ahead, the long-term impact of these logistics improvements will depend on whether smaller industrial clusters can bridge the infrastructure gap. Market observers may monitor whether government policy shifts toward improving last-mile connectivity and developing dedicated regional infrastructure help smaller companies reduce their expenses. For large, diversified chemical players, the current environment may offer a chance to further consolidate their market position by maintaining a structural cost advantage over smaller competitors as national logistics networks continue to mature.