The Services-Led Mirage

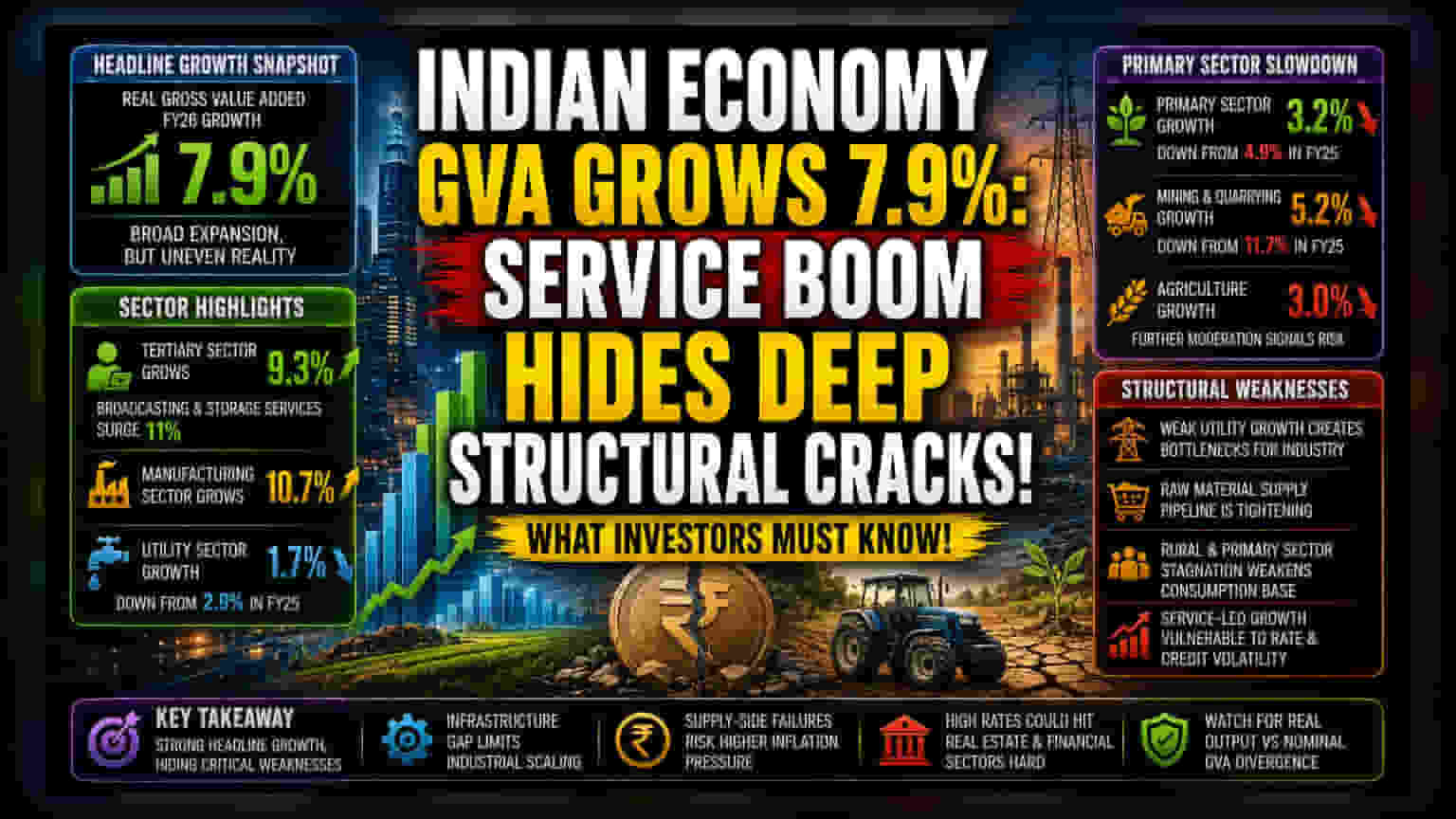

While the 7.9% headline expansion in real Gross Value Added for fiscal year 2026 suggests broad-based prosperity, the underlying data reveals a widening disparity between the tertiary sector and the foundational economy. The tertiary sector's 9.3% expansion, particularly the 11% surge in broadcasting and storage services, has become the primary buoy for national output. However, this reliance on service-oriented growth often masks a lack of depth in capital-intensive sectors. As global financial conditions tighten, a growth model heavily tilted toward professional services, real estate, and finance remains vulnerable to interest rate volatility and shifting discretionary spending patterns.

Industrial Discrepancies and Supply Constraints

Beneath the surface of strong manufacturing gains, the infrastructure reality is far more sobering. The utility segment—specifically electricity, gas, and water supply—stumbled to a mere 1.7% growth rate, down from 2.9% in the prior year. This contraction in essential service inputs acts as a bottleneck for sustained industrial scaling. If the manufacturing sector, which posted a respectable 10.7% growth, cannot access reliable and affordable energy inputs, the long-term margin sustainability for industrial firms remains in jeopardy. This dichotomy suggests that current production gains may be front-loaded, potentially hitting a wall as power infrastructure fails to keep pace with factory output.

The Structural Weakness: Primary Sector Erosion

The most concerning metric in the latest release is the marked slowdown in the primary sector, which decelerated to 3.2% from 4.9% in FY25. With mining and quarrying growth plummeting from a double-digit 11.7% to 5.2%, the raw material pipeline for the broader economy is tightening. Agriculture, the bedrock of domestic consumption demand, further moderated to 3%. This stagnation in the primary sector suggests a dual-risk profile: rising food-based inflation pressure and a diminishing supply of raw materials, both of which threaten to offset the gains seen in the service-centric tertiary index.

The Forensic Bear Case

From a structural standpoint, the Indian economy is exhibiting classic signs of bifurcation. The dependence on high-end services often serves as a lagging indicator of wealth concentration, while the primary sector's decay reflects a weakening rural consumption base. Investors should remain wary of the gap between nominal GVA growth and real economic output. As inflation potentially heats up due to the supply-side failures in the primary sector, the Reserve Bank of India may find its hands tied regarding future monetary policy. A sustained, high-interest-rate environment would disproportionately penalize the real estate and financial services sectors, which are currently fueling the index, creating a precarious dependency loop that could collapse if credit conditions deteriorate further.