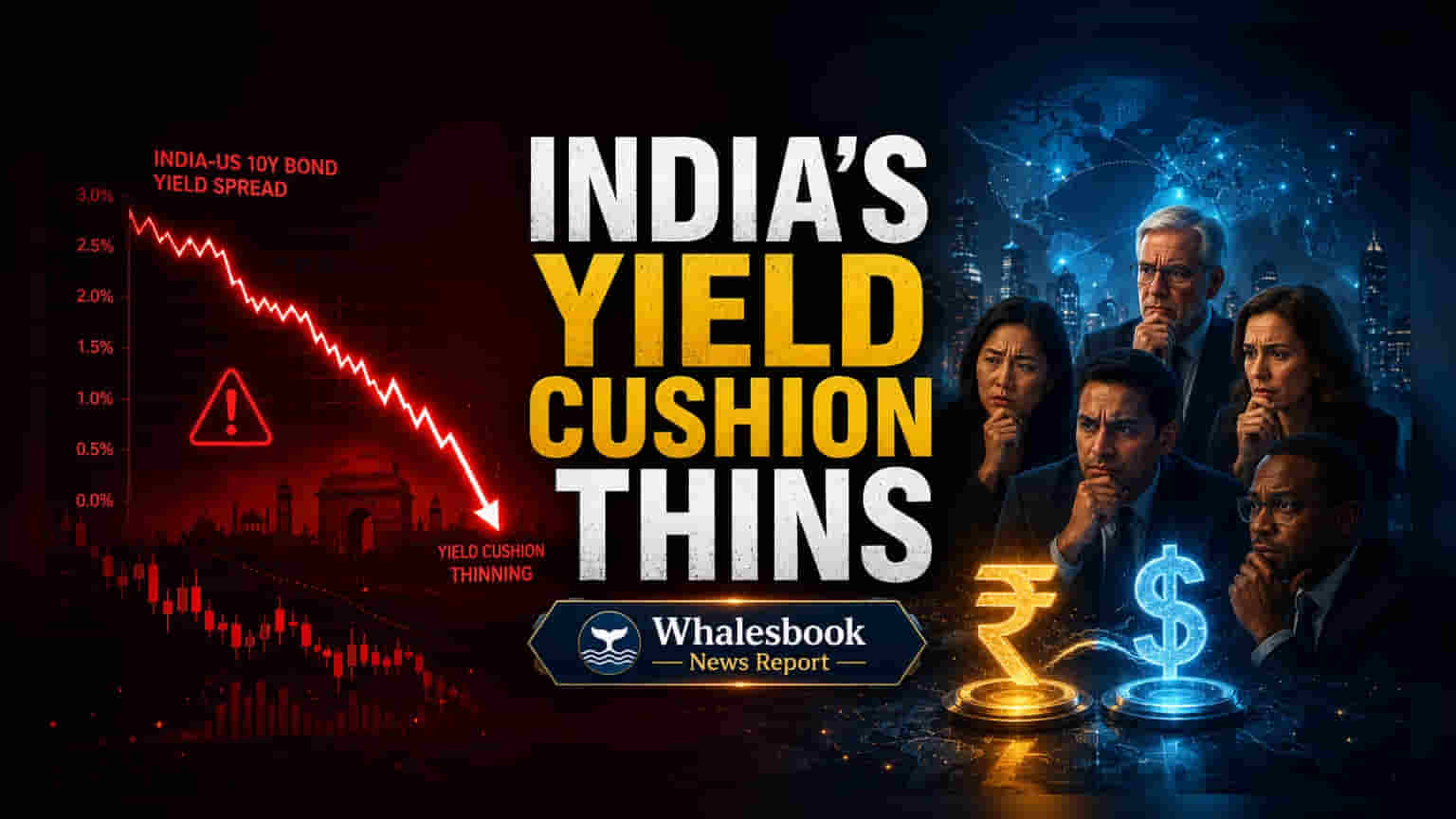

India Bond Yield Spread Shrinks, Challenging Foreign Investors

The shrinking yield difference between Indian and US government bonds presents a critical juncture for international investors. With the historical buffer reduced, the focus is shifting from simply pursuing higher nominal yields to a careful evaluation of currency stability, tax implications, and emerging market volatility.

US Yields Rise, Indian Rates Hold Steady

The yield gap, currently around 250 basis points, has significantly narrowed from its historical average. This compression is mainly due to rising US Treasury yields, driven by persistent inflation and the Federal Reserve's aggressive monetary policy. Indian bond yields, however, have remained stable. This stability is supported by strong domestic demand from financial institutions and the Reserve Bank of India's (RBI) credible inflation control efforts. As of May 20, 2026, India's 10-year government bond yield was about 7.11%, while the US 10-year Treasury yield was 4.674%.

Rethinking Investor Returns

For foreign investors not hedging currency fluctuations, the reduced yield premium poses a significant challenge. Even a small depreciation of the Indian Rupee against the US Dollar could erase the benefit of higher Indian yields, potentially leading to lower returns in dollar terms compared to US Treasury bonds. For those who hedge, currency hedging costs can further reduce the effective yield.

Index Inclusion and Currency Factors

The upcoming inclusion of Indian government bonds in major global indices, starting September 2025, is expected to draw steady passive investment. While this could offset some concerns for active investors, the Indian Rupee's movement remains influenced by various factors, including oil prices, trade balances, equity flows, and geopolitical events. Some analysts predict the Rupee could fall to 95-100 against the US Dollar by the end of 2026, partly due to rising oil import costs. The USD/INR rate was around 96.2760 on May 21, 2026.

RBI's Policy and Market Views

The RBI's main goal is inflation control, not directly managing yield spreads. While a weak rupee could complicate policy, raising rates solely to widen the spread would carry substantial economic costs. Governor Sanjay Malhotra has stated the RBI is watching supply shocks and maintaining a neutral policy stance. Market sentiment is split: some see the reduced yield cushion as a warning, while others believe India's strong domestic demand and growth outlook provide a stable adjustment environment.

Currency Risks for Foreigners

Despite stable domestic demand for Indian bonds, the narrowing yield spread increases currency risk for foreign investors. The Indian Rupee has depreciated about 11.98% in the past year and is expected to trade around 95.77 by the end of the current quarter. This depreciation significantly cuts into the real returns for foreign investors. Additionally, liquidity in the Indian corporate bond market is a concern, with low turnover making it difficult to exit positions without losses. Broader market liquidity issues and external factors like global economic uncertainty could also lead to temporary outflows from Indian debt.

Future Outlook

The future for Indian government bonds is debated. While index inclusion is likely to attract foreign investment, ongoing pressure on the Indian Rupee and rising global yields present challenges. The RBI's focus on balancing inflation control with economic growth, along with global macroeconomic trends, will significantly shape bond market performance and foreign investor sentiment.